PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063333

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063333

Wealth Tech Solution - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

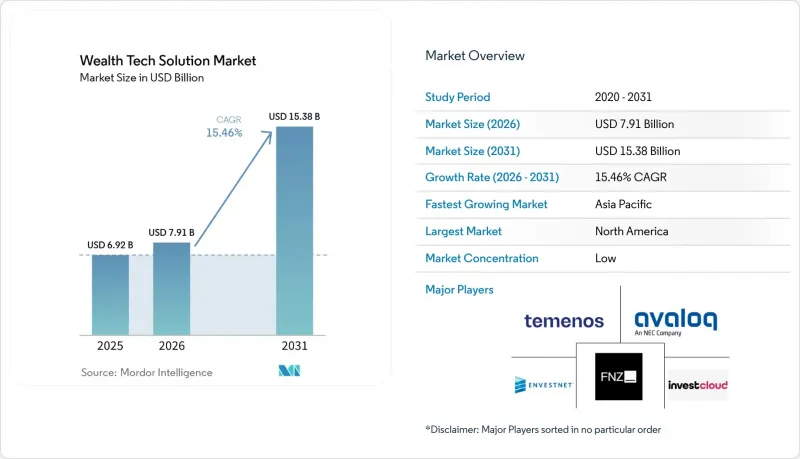

According to Mordor Intelligence, the wealth tech solution market size was valued at USD 6.92 billion in 2025 and estimated to grow from USD 7.91 billion in 2026 to reach USD 15.38 billion by 2031, at a CAGR of 15.46% during the forecast period (2026-2031).

This report is Segmented by Solution Type (Robo-Advisory Platforms, Risk, and More), Deployment Mode (Cloud, On-Premise, and Hybrid), End-User Industry (Banks, and More), Enterprise Size (Large Enterprises and More), Business Model (B2C (Direct-To-Consumer), B2B (Vendor -Financial Institution), and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Wealth Tech Solution Market Trends and Insights

Mainstream Digital-Banking Adoption Accelerates Wealth-Tech Uptake

Rapid migration to mobile banking gives financial institutions a ready-made channel for cross-selling investment products. In 2025, 68% of United States community banks and credit unions signaled plans to embed robo-advisory tools into their apps by 2026, up from 42% in 2024. Younger cohorts reinforce this shift, with 62% of Gen Z and millennials preferring to invest through the same application they use for daily payments. Citi Sky's rollout illustrates the upside, the feature lifted digitally active assets under management by 34% within six months. As banking apps normalize wealth features, standalone robo-advisors face margin pressure unless they cultivate white-label partnerships, and core-banking vendors must decide whether to build or buy wealth capabilities.

Regulatory Push Toward Open-Finance APIs

Open-data mandates are dismantling proprietary data silos, enabling best-of-breed modules to interoperate across custodians. The CFPB's Section 1033 rule obliges depository institutions to provide machine-readable account data, enabling advisors to consolidate positions under a single view. In Europe, the Payment Services Directive 3 extends similar rights to investment accounts, while the Digital Operational Resilience Act tightens oversight of critical third-party providers. Although compliance can exceed USD 5 million for systemically important banks, first movers stand to win mandates from institutions that would rather outsource resilient infrastructure than retrofit legacy codebases.

Data-Privacy and Cloud-Sovereignty Regulations Raise Compliance Cost

Fines under Europe's General Data Protection Regulation reached EUR 1.15 billion (USD 1.33 billion) in 2024, with financial services absorbing 28%. DORA compounds costs by mandating annual penetration tests and exit plans that allow institutions to replace cloud vendors on short notice, totaling USD 5 million for the largest banks. Similar localization mandates in China and India prevent vendors from hosting client data in a single region, prompting a pivot to sovereign clouds that carry a 15%-25% price premium. Vendors must balance resilience with cost discipline to remain competitive.

Other drivers and restraints analyzed in the detailed report include:

- Rising Gen Z and Millennial Demand for Self-Directed and Hybrid Advisory Tools

- AI-Driven Hyper-Personalization Improves Conversion and Retention

- Integration Debt With Legacy Core-Banking Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Portfolio management and reporting software held 38.21% of the wealth-tech solutions market share in 2025, underscoring its role as the operational backbone for registered investment advisors. Yet API infrastructure is advancing at a 16.66% CAGR, signaling a pivot toward composable modules that institutions can embed into payroll systems and neobank apps. The wealth tech solution market size for API-centric offerings is projected to grow as white-label platforms compress launch cycles from 18 months to under 90 days.

Demand for robo-advisory remains robust, evidenced by Betterment's USD 65 billion assets under management, but differentiation is drifting toward client engagement. Vendors such as Fidelity combine algorithmic allocation with certified-planner support, achieving engagement 4 times that of legacy portals. Risk, compliance, and RegTech modules enjoy steady tailwinds from DORA and Section 1033 reporting mandates, while data and AI engines have shifted from nice-to-have add-ons to core buying criteria.

Cloud is projected to account for 61.81% of spending in 2025, highlighting its dominant role in the market. However, hybrid configurations are experiencing significant growth, with an annual growth rate of 16.05%, as organizations strive to balance sovereignty mandates with the flexibility and scalability offered by elastic compute. This trend is driving the expansion of the wealth tech solution market size associated with hybrid deployments. For instance, European banks are increasingly adopting hybrid models to ensure client data remains within sovereign regions while leveraging public clouds for computationally intensive tasks, such as running Monte Carlo simulations.

Wealth-tech solutions market. On-premise solutions continue to hold a strong position, particularly among ultra-high-net-worth family offices and in jurisdictions that prioritize minimizing third-party risks. The implementation of the Digital Operational Resilience Act (DORA), which mandates that data must be portable across providers, adds complexity to migration timelines. However, advancements in secure access service edge (SASE) frameworks are facilitating this transition. By integrating network security and cloud connectivity into a unified policy engine, SASE frameworks are helping organizations streamline their migration processes while maintaining robust security measures.

Geography Analysis

North America generated 39.91% of 2025 revenue, propelled by more than 15,000 registered investment advisors and the earliest adoption of robo-advisory among mass-affluent households. The compulsory rollout of Section 1033 is boosting aggregation demand, while Vanguard Digital Advisor's minimum investment cut to USD 100 broadened access for first-time investors. Canada's market revolves around five dominant banks, making integration partnerships critical, whereas Mexico's regulatory reforms are sparking interest from United States-based platforms seeking fresh growth corridors.

Asia-Pacific is the fastest-growing region, registering a 16.68% CAGR through 2031. Hong Kong clients show high readiness for AI-based portfolio management, and Singapore continues to position itself as a wealth hub for Southeast Asia. Avaloq's April 2026 expansion into Japan and Australia underscores vendor interest in countries where aging populations and historically low yields are pushing savers toward equities. India's mutual-fund assets more than doubled between 2020 and 2024, catalyzing demand for digital distribution that bypasses legacy broker networks.

Europe's outlook hinges on the phased enforcement of PSD3, the Payment Services Regulation, and DORA, all of which converge by 2027. While the Nordics embrace public-cloud deployments, Germany emphasizes private clouds, and the United Kingdom refines suitability rules for robo-advisors, signaling persistent fragmentation. South America's momentum centers on Brazil, where instant payments and open banking rails invite embedded investment in use cases. In the Middle East and Africa, the United Arab Emirates and Saudi Arabia lead pilot programs within regulatory sandboxes, whereas South Africa integrates wealth management modules into established banking apps to expand access among the region's growing middle class.

- InvestCloud LLC

- Avaloq Group AG

- FNZ Group Ltd.

- Envestnet Inc.

- Temenos AG

- Additiv AG

- Fincite GmbH

- SS&C Advent (Black Diamond)

- Orion Advisor Tech LLC

- Addepar Inc.

- Valuefy Solutions Pvt. Ltd.

- InvestSuite NV

- Bambu Global Pte. Ltd.

- Betterment LLC

- Wealthfront Corporation

- SigFig Wealth Management LLC

- Stash Financial Inc.

- Robinhood Markets Inc.

- Broadridge Financial Solutions Inc.

- Charles River Development (State Street Corp.)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream Digital-Banking Adoption Accelerates Wealth-Tech Uptake

- 4.2.2 Regulatory Push Toward Open-Finance APIs (PSD3, DORA, US Open Banking)

- 4.2.3 Rising Gen Z and Millennial Demand for Self-Directed and Hybrid Advisory Tools

- 4.2.4 AI-Driven Hyper-Personalisation Improves Conversion and Retention

- 4.2.5 Embedded Wealth Features Inside Payroll Platforms Unlock SME Channel

- 4.2.6 Quantum-Secure Encryption Mandates Spur Refresh of Wealth-Core Architectures

- 4.3 Market Restraints

- 4.3.1 Data-Privacy and Cloud-Sovereignty Regulations Raise Compliance Cost

- 4.3.2 Integration Debt With Legacy Core-Banking Systems

- 4.3.3 Digital-Identity Fraud Forces Multi-Factor Authentication Friction

- 4.3.4 Wealth-Tech Vendor Consolidation Triggers Client Disruption

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution Type

- 5.1.1 Robo-Advisory Platforms

- 5.1.2 Portfolio Management and Reporting Software

- 5.1.3 Client Engagement and Digital Advisory Tools

- 5.1.4 Risk, Compliance and RegTech Modules

- 5.1.5 Data, Analytics and AI Engines

- 5.1.6 API / Integration and Wealth-as-a-Service Infrastructure

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By End-User Industry

- 5.3.1 Banks

- 5.3.2 Wealth Management Firms

- 5.3.3 Registered Investment Advisors (RIAs)

- 5.3.4 FinTech Platforms and Neobanks

- 5.3.5 Rest of End-User Industries

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-sized Enterprises

- 5.5 By Business Model

- 5.5.1 B2C (Direct-to-Consumer)

- 5.5.2 B2B (Vendor -Financial Institution)

- 5.5.3 B2B2C / White-Label Platforms

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 InvestCloud LLC

- 6.4.2 Avaloq Group AG

- 6.4.3 FNZ Group Ltd.

- 6.4.4 Envestnet Inc.

- 6.4.5 Temenos AG

- 6.4.6 Additiv AG

- 6.4.7 Fincite GmbH

- 6.4.8 SS&C Advent (Black Diamond)

- 6.4.9 Orion Advisor Tech LLC

- 6.4.10 Addepar Inc.

- 6.4.11 Valuefy Solutions Pvt. Ltd.

- 6.4.12 InvestSuite NV

- 6.4.13 Bambu Global Pte. Ltd.

- 6.4.14 Betterment LLC

- 6.4.15 Wealthfront Corporation

- 6.4.16 SigFig Wealth Management LLC

- 6.4.17 Stash Financial Inc.

- 6.4.18 Robinhood Markets Inc.

- 6.4.19 Broadridge Financial Solutions Inc.

- 6.4.20 Charles River Development (State Street Corp.)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment