PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063346

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063346

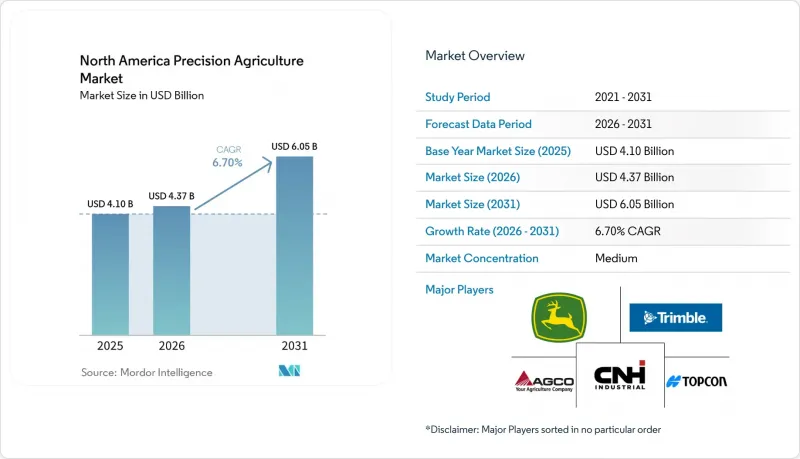

North America Precision Agriculture - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america precision agriculture market is projected to grow from USD 4.10 billion in 2025 and USD 4.37 billion in 2026 to USD 6.05 billion by 2031, registering a CAGR of 6.7% between 2026 and 2031.

This report is Segmented by Component (Hardware, Software, and More), by Technology (Guidance (GPS/GNSS) and More), by Application (Yield Monitoring and More), by Farm Size (Large Farms (More Than 1, 000 Acres), and More), and by Geography (United States, Canada, Mexico, and Rest of North America). The Market Forecasts are Provided in Terms of Value (USD).

North America Precision Agriculture Market Trends and Insights

Optimized Variable-Rate Inputs Lowering Costs

Variable-rate technology enables growers to adjust seed, fertilizer, and pesticide application rates within specific micro-zones, reducing waste by 10%-15% and providing immediate cash-flow benefits . John Deere's ExactApply nozzle system achieved herbicide savings of up to 77% during trials conducted in Nebraska and Kansas in 2025 . Adoption of this technology is advancing most rapidly in areas with high soil variability and existing GPS-guided tractors, particularly in regions such as Iowa, Illinois, and Saskatchewan. Dealers have reported strong sales of retrofit controllers, which can be installed on existing planters at one-third the cost of full replacements.

Subsidies Promoting Smart Equipment Use

Cost-share incentives remain significant in promoting the adoption of precision agriculture technologies across North America. In the United States, the Department of Agriculture enhanced conservation funding programs, including the Environmental Quality Incentives Program, during 2021-2023. This expansion increased financial support for precision farming tools and climate-smart practices. Similarly, in Canada, Agriculture and Agri-Food Canada launched the Agricultural Clean Technology Program in 2021, providing cost-sharing assistance for precision equipment, sensors, and energy-efficient technologies, with funding available through 2026.

High Capital Costs for Advanced Technologies

Equipment costs remain high for a standard package comprising RTK receivers, drone platforms, and variable-rate controllers. This expense poses a significant challenge for small grain farms, which struggle to amortize such investments when net returns are limited. High initial investment requirements continue to be a significant barrier to the adoption of precision agriculture technologies in North America. The substantial upfront costs of advanced equipment, including GPS-guided systems, sensors, and data platforms, discourage adoption, particularly among small and mid-sized farms with limited capital access. Beyond hardware expenses, farmers also face difficulties in assessing the return on investment due to uncertainties regarding long-term economic benefits and the operational complexity of these technologies.

Other drivers and restraints analyzed in the detailed report include:

- Increased Adoption of IoT Sensors, Drones, and Analytics

- Carbon-Credit Gains from Precise Nitrogen Use

- Data Interoperability and Privacy Issues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware captured the largest 68.0% of the North America precision agriculture market share in 2025, owing to the entrenched base of GPS receivers and drone platforms. Even so, the software market size is projected to grow at the fastest 9.8% CAGR from 2026 to 2031. The Climate Corporation gained new FieldView subscribers, with a significant portion opting to pay additional fees for variable-rate scripting and carbon-credit documentation. In 2023, Trimble announced its mixed-fleet precision agriculture strategy through a joint venture with AGCO, emphasizing integration across equipment brands and data systems. By 2024, this initiative expanded into broader multi-brand connectivity and data integration platforms, enabling telemetry interoperability across the Deere & Company, CNH Industrial N.V., and AGCO Corporation .

Service-based offerings are expanding in response to increasing operational complexity, with vendors emphasizing integrated digital platforms and remote support to minimize reliance on on-site interventions. Equipment manufacturers are incorporating telematics, connectivity, and agronomic advisory services into their offerings, aligning revenue models with performance outcomes and fostering long-term customer engagement. Additionally, advanced sensing technologies, such as hyperspectral imaging and soil analysis tools, are being integrated into broader digital ecosystems. Proprietary analytics play a key role in transforming raw data into actionable insights for effective farm management.

Guidance (GPS/GNSS) held the largest 37.5% of the North America precision agriculture market share in 2025, reflecting two decades of retrofits and factory installs. The variable-rate technology market size is projected to grow at the fastest 10.4% CAGR from 2026 to 2031. This growth is driven by the addition of prescription control over seeding, fertilization, and chemical application, which enhances returns on existing autosteer platforms. In May 2025, John Deere's acquisition of Sentera integrated hyperspectral analytics directly into its Operations Center, eliminating a subscription layer and facilitating adoption for connected machines.

Remote sensing and analytics providers are enhancing edge computing and real-time processing capabilities, enabling quicker decision-making and reducing delays in field assessments. Interoperability solutions and retrofit technologies are improving accessibility by allowing older machinery to connect with modern precision systems, facilitating broader adoption among cost-conscious operators. While artificial intelligence-driven analytics are gaining traction for applications like crop monitoring and yield optimization, adoption remains limited to technologically advanced users due to high data requirements and implementation complexities.

List of Companies Covered in this Report:

- Deere & Company

- Trimble Inc.

- CNH Industrial N.V.

- AGCO Corporation

- Topcon Corporation

- Farmers Edge Inc.

- Hexagon AB

- Lindsay Corporation

- Valmont Industries, Inc

- TeeJet Technologies (Spraying Systems Co.)

- Ag Leader Technology, Inc.

- DroneDeploy, Inc.

- Kubota Corporation

- Sentera, Inc.

- The Climate Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Optimized variable-rate inputs lowering costs

- 4.2.2 Subsidies promoting smart equipment use

- 4.2.3 Increased adoption of IoT sensors, drones, and analytics

- 4.2.4 Carbon-credit gains from precise nitrogen use

- 4.2.5 Private 5G networks on large farms

- 4.2.6 Soil-microbiome analytics enabling adaptive fertility

- 4.3 Market Restraints

- 4.3.1 High capital costs for advanced technologies

- 4.3.2 Data interoperability and privacy issues

- 4.3.3 Lack of ag-tech technicians in rural areas

- 4.3.4 Connectivity gaps due to fragmented rural spectrum

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Technology

- 5.2.1 Guidance (GPS (Global Positioning System)/GNSS (Global Navigation Satellite System))

- 5.2.2 Remote Sensing

- 5.2.3 Variable-rate Technology

- 5.2.4 AI-enabled Analytics

- 5.3 By Application

- 5.3.1 Yield Monitoring

- 5.3.2 Field Mapping

- 5.3.3 Crop Scouting

- 5.3.4 Weather Tracking and Forecasting

- 5.3.5 Irrigation Management

- 5.3.6 Inventory and Labor Management

- 5.4 By Farm Size

- 5.4.1 Large Farms (more than 1,000 acres)

- 5.4.2 Medium Farms (250-999 acres)

- 5.4.3 Small Farms (less than 250 acres)

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

- 5.5.4 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 Trimble Inc.

- 6.4.3 CNH Industrial N.V.

- 6.4.4 AGCO Corporation

- 6.4.5 Topcon Corporation

- 6.4.6 Farmers Edge Inc.

- 6.4.7 Hexagon AB

- 6.4.8 Lindsay Corporation

- 6.4.9 Valmont Industries, Inc

- 6.4.10 TeeJet Technologies (Spraying Systems Co.)

- 6.4.11 Ag Leader Technology, Inc.

- 6.4.12 DroneDeploy, Inc.

- 6.4.13 Kubota Corporation

- 6.4.14 Sentera, Inc.

- 6.4.15 The Climate Corporation

7 Market Opportunities and Future Outlook