PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063365

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063365

Automotive Start-Stop System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

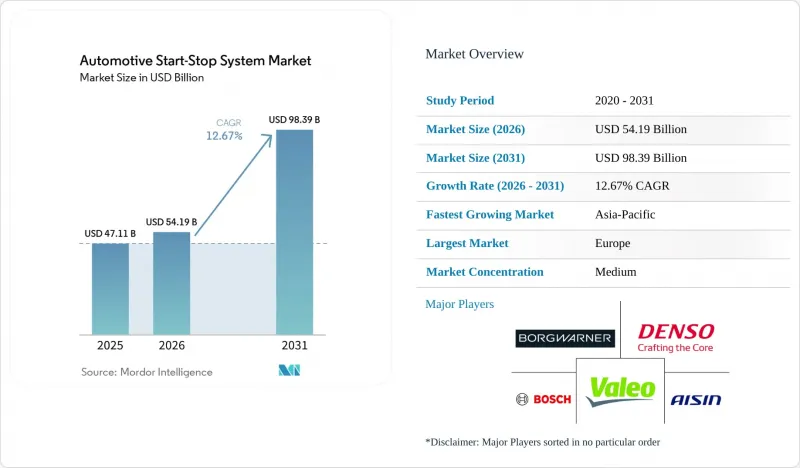

According to Mordor Intelligence, the automotive start-Stop system market size is projected to expand from USD 47.11 billion in 2025 and USD 54.19 billion in 2026 to USD 98.39 billion by 2031, registering a CAGR of 12.67% between 2026 to 2031.

This report is Segmented by Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, and More), Technology (Belt-Driven Alternator Starter, Integrated Starter Generator, and Direct Starter), Component (Battery, Starter Motor, Alternator, and More), Fuel Type (Gasoline, Alternative Fuels, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Automotive Start-Stop System Market Trends and Insights

Heightened Corporate Average Fuel Economy and CO2 Regulations

Regulatory stringency remains the single most potent lever for expansion in the automotive start-stop system market. The United States finalized corporate average fuel-economy targets that climb toward 50.4 miles per gallon by model year 2031, and penalties for non-compliance are set high enough to shift OEM product-planning budgets toward cost-effective idle-reduction content. Europe's revised passenger-van CO2 performance standards require a 55% drop in fleet emissions by 2030 to 2034, cementing micro-hybrid demand as a compliance backstop when battery-electric deliveries miss plan. Similar tightening is visible in India and Brazil, binding the technology to certification success in the next five-year product cycle. Collectively, these overlapping mandates provide an enduring compliance floor that supports long-run adoption.

OEM Integration of 48-Volt Mild-Hybrid Architectures

Automakers are migrating from 12-volt belt-starter packages to 48-volt integrated starter-generator (ISG) topologies that unlock regenerative braking and torque assist. MAHLE's 48-volt belt-starter-generator delivers up to 15 kW of recuperation, saving 12-15% fuel in urban cycles.Silicon-carbide power devices from STMicroelectronics and onsemi are cutting conversion losses by 30%, letting OEMs shrink under-hood packaging. These gains, matched with falling lithium-ion prices, make 48-volt the dominant bridge toward deeper electrification without incurring full BEV cost or charging-infrastructure risk.

Accelerated Adoption of Battery-Electric Vehicles Cannibalizing Fitment

Rising BEV penetration directly shrinks the addressable pool for start-stop hardware. China's new-energy vehicles accounted for 44.97% of all new automobile registrations in 2025, with BEVs forming about 70% of that mix. Harvard Business School research shows that the start-stop business case weakens as BEV total cost of ownership approaches parity with internal-combustion vehicles in markets with high fuel prices and dense charging grids. Premium segments convert first, chopping volume for 12-volt systems. While emerging economies and commercial fleets temper the impact, BEV growth remains the single largest structural headwind.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Micro-Hybrid Passenger Cars in Emerging Economies

- Continuous Decline in Lithium-Ion Battery USD Per kWh Enhancing Durability

- Driver Discomfort from NVH During Heavy Stop-Start Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The automotive start-stop system market for passenger cars dominated in 2025, with a 62.14% share, as most global light-vehicle platforms standardized on idle-reduction to meet fleet targets. Urban motorists in India and Southeast Asia spend long stretches in stop-and-go traffic, making fuel savings from start-stop immediately tangible. Fleet operators in Europe and North America also add the technology to light vans to curb discretionary idling. Though heavy trucks lag in torque and accessory loads, niche applications such as refuse trucks are slowly adopting them.

Two-wheelers represent the fastest-growing segment, forecast to grow at a 14.61% CAGR through 2031, and are reshaping the automotive start-stop system market. Honda's Idling Stop System restarts a scooter in 0.5 seconds, delivering double-digit fuel savings that resonate with price-sensitive commuters. TVS Motor has replicated the approach with its intelliGO starter, pushing penetration beyond premium bikes into mass-market city runabouts. Rising helmet-law enforcement and growing micro-mobility appetites further enlarge the pool of urban riders that value efficiency and low tail-pipe emissions. As two-wheeler output expands in India, Indonesia, and Vietnam, their share of overall system shipments will rise steadily.

Belt-driven alternator starters enjoyed a robust 38.42% share of the automotive start-stop system market in 2025, driven by their favorable USD 200-300 bill-of-materials cost. It will continue to anchor entry-level micro-hybrids, particularly where 12-volt electrical architecture remains in place. Yet integrated starter-generator units are poised for double-digit growth as OEMs roll out 48-volt platforms across premium and, eventually, volume models. The switch unlocks energy recuperation, electric torque fill, and smoother restarts.

The integrated starter generator is set to post an 16.13% CAGR, capturing share in Europe and China first, then in North America. Valeo's high-volume 48-volt program offers 15 kW recuperation, enough to power auxiliary compressors and let a small three-cylinder engine feel like a larger four-cylinder. Semiconductor advances, especially 750 V silicon-carbide MOSFETs from Infineon, are slashing thermal losses and enabling smaller converters, enabling packaging in compact sedans. Direct-starter solutions, though cheaper, lack these functional wins and are increasingly relegated to late-life platforms or markets with lenient standards.

Geography Analysis

In 2025, Europe secured 35.17% of the global automotive start-stop system market, solidifying its position as the leading regional market. This dominance stems from stringent EU CO2 emission regulations, aggressive fleet efficiency mandates, and the widespread adoption of 48-volt mild-hybrid architectures in passenger vehicles. Even with the swift rise of battery-electric vehicles, start-stop systems remain prevalent on internal combustion and hybrid platforms, serving as a cost-effective compliance solution. Moreover, a robust Tier-1 supplier ecosystem in Germany, France, and other automotive hubs bolsters system integration capabilities and fuels strong aftermarket demand.

North America is a pivotal market for automotive start-stop systems, buoyed by tightening fuel-economy standards and their growing presence in light trucks, SUVs, and commercial fleets. Although historically lower fuel prices in the U.S. have tempered adoption rates compared to Europe, mounting regulatory pressures are now hastening their integration across OEM platforms. Additionally, the region's gradual pivot towards mild-hybrid powertrains is amplifying demand, especially in next-gen pickup and SUV models.

The Asia-Pacific region, marked by rapid urbanization and rising fuel costs, is witnessing a surge in demand for automotive start-stop systems. Countries like China, India, Japan, and those in Southeast Asia are tightening emissions regulations, further driving this trend. The region's large-scale production of compact and entry-level vehicles has led to widespread use of start-stop systems as a cost-effective solution for improving fuel efficiency. Furthermore, the increasing localization of battery and starter motor manufacturing is enhancing affordability, pushing deeper penetration into mass-market vehicle segments.

Furthermore, South America, the Middle East, and Africa form a smaller yet emerging market for automotive start-stop systems. Countries like Brazil, Saudi Arabia, and South Africa are emphasizing fuel efficiency, tightening regulations, and modernizing fleets. However, adoption remains constrained by economic volatility, harsh operating environments, and limited electrification infrastructure, which collectively slow large-scale penetration despite steady incremental demand.

- Aisin Corporation

- BorgWarner Inc.

- Continental AG

- DENSO Corporation

- Valeo SA

- Robert Bosch GmbH

- Hitachi Astemo Ltd.

- HELLA GmbH & Co. KGaA

- Johnson Controls International plc

- Mitsubishi Electric Corporation

- SEG Automotive Germany GmbH

- Marelli Holdings Co., Ltd.

- Schaeffler AG

- Panasonic Holdings Corporation (Automotive Systems)

- Calsonic Kansei Corporation

- Clarios, LLC

- Exide Technologies, LLC

- Furukawa Electric Co., Ltd.

- Prestolite Electric Incorporated

- Mando Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Heightened Corporate Average Fuel Economy (CAFE) and CO2 Regulations

- 4.2.2 Rising Demand for Micro-Hybrid Passenger Cars in Emerging Economies

- 4.2.3 OEM Integration of 48-V Mild-Hybrid Architectures

- 4.2.4 Continuous Decline in Lithium-Ion Battery USD/kWh Enhancing Durability

- 4.2.5 Adoption of Edge-AI Idle Prediction Algorithms to Minimize Restart Lag

- 4.2.6 Insurance Telematics Incentives Favoring Idle-Reduction Technologies

- 4.3 Market Restraints

- 4.3.1 Accelerated Adoption of Battery-Electric Vehicles Cannibalizing Fitment

- 4.3.2 Driver Discomfort From NVH During Heavy Stop-Start Cycles

- 4.3.3 Transition to Solid-State 12-V Batteries Necessitating Redesigns

- 4.3.4 Supply-Chain Fragility for Power MOSFETs and Relays

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Light Commercial Vehicles

- 5.1.3 Heavy Commercial Vehicles

- 5.1.4 Two-Wheelers

- 5.2 By Technology

- 5.2.1 Belt-Driven Alternator Starter (BDAS)

- 5.2.2 Integrated Starter Generator (ISG)

- 5.2.3 Direct Starter

- 5.3 By Component

- 5.3.1 Battery

- 5.3.2 Starter Motor

- 5.3.3 Alternator

- 5.3.4 Control Unit and Sensors

- 5.3.5 Other Components

- 5.4 By Fuel Type

- 5.4.1 Gasoline

- 5.4.2 Diesel

- 5.4.3 Hybrid (Incl. 48-V)

- 5.4.4 Alternative Fuel Types

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Aisin Corporation

- 6.4.2 BorgWarner Inc.

- 6.4.3 Continental AG

- 6.4.4 DENSO Corporation

- 6.4.5 Valeo SA

- 6.4.6 Robert Bosch GmbH

- 6.4.7 Hitachi Astemo Ltd.

- 6.4.8 HELLA GmbH & Co. KGaA

- 6.4.9 Johnson Controls International plc

- 6.4.10 Mitsubishi Electric Corporation

- 6.4.11 SEG Automotive Germany GmbH

- 6.4.12 Marelli Holdings Co., Ltd.

- 6.4.13 Schaeffler AG

- 6.4.14 Panasonic Holdings Corporation (Automotive Systems)

- 6.4.15 Calsonic Kansei Corporation

- 6.4.16 Clarios, LLC

- 6.4.17 Exide Technologies, LLC

- 6.4.18 Furukawa Electric Co., Ltd.

- 6.4.19 Prestolite Electric Incorporated

- 6.4.20 Mando Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment