PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063420

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063420

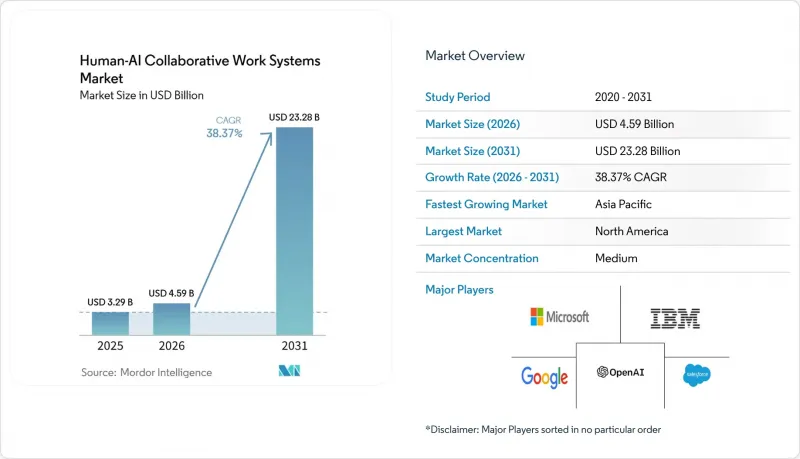

Human-AI Collaborative Work Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the human-AI collaborative work systems market size is projected to be USD 3.29 billion in 2025, USD 4.59 billion in 2026, and reach USD 23.28 billion by 2031, growing at a CAGR of 38.37% from 2026 to 2031.

This report is Segmented by Deployment Mode (On-Premise, Cloud, and Hybrid), Component (Software, and Services), End-User Industry (IT and Telecom, Healthcare and Life Sciences, Manufacturing, BFSI, Retail and E-Commerce, Education, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Human-AI Collaborative Work Systems Market Trends and Insights

Escalating Enterprise Adoption of Generative AI Assistants

Organizations are embedding assistants directly into decision workflows rather than treating them as separate productivity add-ons. Microsoft disclosed that more than 65,000 enterprises consumed Azure OpenAI Service by late 2025, almost quadrupling its early-2024 count, while Copilot for Microsoft 365 surpassed 15 million paid seats, yet still touched less than 4% of the Office installed base, showing substantial headroom. Salesforce customers using Agentforce reported 30-50% reductions in case-resolution time after its late-2025 launch. IBM's internal roll-out of watsonx across 270,000 employees targets USD 4.5 billion in cumulative productivity gains by 2027, reinforcing the ROI narrative. These examples underscore how early adopters validate economic impact before extending deployment across all knowledge workers.

Advances in Multimodal Large Language Models Enhancing Collaboration

Multimodal models that understand text, images, audio, and video are opening new collaboration frontiers in design, clinical diagnostics, and industrial maintenance. Google's Gemini hit 750 million monthly active users in December 2025, with many regulated-industry customers opting for on-premises deployments to comply with data-residency rules. Adobe embedded Firefly into Creative Cloud, enabling marketers to generate personalized visual assets without hiring extra designers. In healthcare, the FDA approved more than 950 AI-enabled medical devices through 2024, many of which are powered by vision-language models that streamline radiology reads. The move toward edge inference addresses low-latency requirements in retail checkout and autonomous robotics scenarios.

Lack of Standardized Human-AI Interaction Protocols

No common protocol governs how agents receive instructions, ask clarifying questions, or escalate to humans. ISO/IEC 42001 outlines management systems but leaves technical hand-off details undefined. IEEE's P7001 transparency standard remains voluntary and will not be finalized until 2027. Enterprises report that close to 40% of integration time is spent harmonizing authentication schemes, feedback loops, and audit logs across vendors. This fragmentation slows multi-agent adoption and increases switching costs, particularly inside regulated finance and healthcare environments that must document every decision path.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Hybrid-Work Orchestration Platforms

- Integration of RPA Bots With Conversational Agents

- Data-Privacy Concerns Limiting Cross-Team Data Sharing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid models are forecast to lead growth, advancing at a 38.97% CAGR from 2026-2031, as heavily regulated sectors process sensitive data on-premise while offloading non-critical inference to the cloud. Financial institutions using Azure Stack or Google Distributed Cloud keep customer PII within local jurisdiction while still using the latest transformer models for risk scoring. In manufacturing plants, edge nodes execute low-latency quality inspections while centralized servers refine models, demonstrating how a hybrid architecture solves both data sovereignty and millisecond response constraints.

Cloud deployments nonetheless sustained the largest 47.22% share of the human-AI collaborative work systems market in 2025 because pure SaaS minimizes upfront capital outlays and accelerates proof of value. On-premises remains relevant for defense and public-sector agencies that require air-gapped security. Vendors now bundle a single control plane spanning environments, easing observability and cost governance. The architectural flexibility widens the market for human-AI collaborative work systems, as late-majority adopters demand compliance without sacrificing performance.

While software captured 63.49% revenue in 2025, services will expand more quickly at a 40.37% CAGR as enterprises seek integration, custom workflow design, and periodic model re-tuning. Continuous audit obligations outlined in the EU AI Act and sectoral U.S. rules oblige organizations to refresh fairness and bias reports for each model iteration, a task often outsourced to systems integrators. By early 2026, Accenture had trained more than 40,000 consultants in generative AI to meet surging demand.

The human-AI collaborative work systems market for managed services is growing fastest among small and medium enterprises that lack in-house data scientists. Turnkey subscription bundles from monday.com or ClickUp wrap platform access with support, lowering entry barriers. Some vendors tie professional services to outcome-based pricing, aligning incentives around productivity lifts rather than hourly billing, a trend expected to reshape contracting norms across the human-AI collaborative work systems industry.

Geography Analysis

North America retained 34.57% revenue in 2025, anchored by hyperscaler capex and early experimentation across software, telecom, and professional services. Microsoft invested USD 37.5 billion in AI-optimized data centers that now underpin Azure OpenAI Service, while Salesforce saw 70% of Agentforce pilots originate from U.S. customers, reflecting a culture of rapid technology trials. Nonetheless, litigation under HIPAA and GLBA prolongs deployment timelines in healthcare and banking as risk officers scrutinize data flow.

Asia-Pacific is projected to be the most dynamic region, registering a 39.57% CAGR. China's CNY 1 trillion (USD 138.9 billion approximately) national AI program funds domestic model development by Baidu, Alibaba, and Tencent, emphasizing Mandarin fluency and local domain adaptation. India's thriving IT services sector embeds AI to raise billable efficiency, supported by government subsidies and a vast English-speaking talent pool. Japan and South Korea focus on manufacturing and semiconductor design to offset aging demographics and global supply-chain shifts. However, stringent data-sovereignty laws force multinational companies to maintain parallel instances, inflating operating costs.

Europe balances innovation with strict compliance. The EU AI Act's transparency mandates lengthen procurement cycles yet create opportunities for governance specialists. Germany leads industrial adoption, particularly in automotive predictive maintenance, whereas the United Kingdom leverages its AI Safety Institute for pre-deployment testing that reassures corporate boards. Cloud region build-outs in Brazil, the United Arab Emirates, and South Africa are gradually pulling Latin America and the Middle East, and Africa into the human-AI collaborative work systems market, though spending remains concentrated in multinational subsidiaries.

- Microsoft Corporation

- Google LLC

- IBM Corporation

- OpenAI, L.L.C.

- Salesforce, Inc.

- Adobe Inc.

- Atlassian Corporation

- ServiceNow, Inc.

- UiPath, Inc.

- Automation Anywhere, Inc.

- Zoho Corporation Pvt. Ltd.

- monday.com Ltd.

- Slack Technologies, L.L.C.

- Notion Labs, Inc.

- GitHub, Inc.

- Figma, Inc.

- Zoom Video Communications, Inc.

- ClickUp Technologies Inc.

- Airtable, Inc.

- Workday, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Enterprise Adoption of Generative AI Assistants

- 4.2.2 Advances in Multimodal Large Language Models Enhancing Collaboration

- 4.2.3 Rising Demand for Hybrid-Work Orchestration Platforms

- 4.2.4 Integration of RPA Bots with Conversational Agents

- 4.2.5 Availability of Low-Code and No-Code AI Development Tools

- 4.2.6 Growing Compliance Mandates for AI Auditability and Transparency

- 4.3 Market Restraints

- 4.3.1 Lack of Standardized Human-AI Interaction Protocols

- 4.3.2 Data-Privacy Concerns Limiting Cross-Team Data Sharing

- 4.3.3 High Upfront Integration and Training Costs

- 4.3.4 Workforce Resistance Due to Job-Displacement Anxiety

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.3 By End-User Industry

- 5.3.1 IT and Telecom

- 5.3.2 Healthcare and Life Sciences

- 5.3.3 Manufacturing

- 5.3.4 BFSI

- 5.3.5 Retail and E-commerce

- 5.3.6 Education

- 5.3.7 Government and Public Sector

- 5.3.8 Other End-user Industries

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Google LLC

- 6.4.3 IBM Corporation

- 6.4.4 OpenAI, L.L.C.

- 6.4.5 Salesforce, Inc.

- 6.4.6 Adobe Inc.

- 6.4.7 Atlassian Corporation

- 6.4.8 ServiceNow, Inc.

- 6.4.9 UiPath, Inc.

- 6.4.10 Automation Anywhere, Inc.

- 6.4.11 Zoho Corporation Pvt. Ltd.

- 6.4.12 monday.com Ltd.

- 6.4.13 Slack Technologies, L.L.C.

- 6.4.14 Notion Labs, Inc.

- 6.4.15 GitHub, Inc.

- 6.4.16 Figma, Inc.

- 6.4.17 Zoom Video Communications, Inc.

- 6.4.18 ClickUp Technologies Inc.

- 6.4.19 Airtable, Inc.

- 6.4.20 Workday, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment