PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063435

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063435

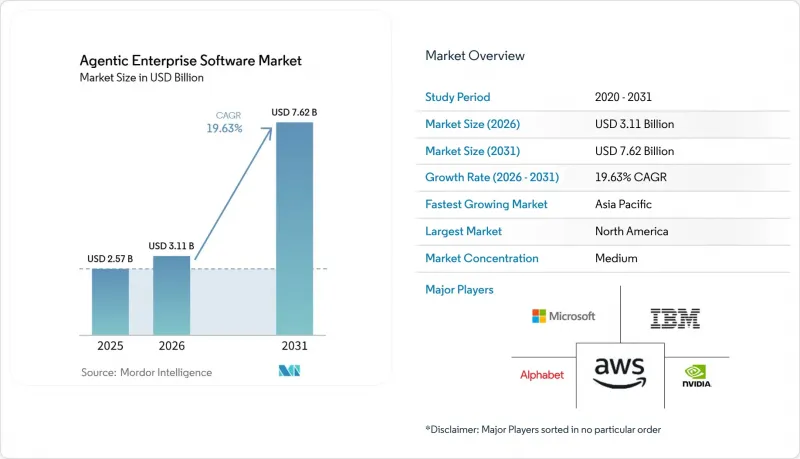

Agentic Enterprise Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the agentic enterprise software market size is expected to grow from USD 2.57 billion in 2025 to USD 3.11 billion in 2026 and is forecast to reach USD 7.62 billion by 2031 at a 19.63% CAGR over 2026-2031.

This report is Segmented by Deployment Mode (Cloud, On-Premise, and Hybrid), Component (Software and Services), Organization Size (Large Enterprises and Small and Medium Enterprises), Industry Vertical (BFSI, Healthcare and Life Sciences, Manufacturing, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Agentic Enterprise Software Market Trends and Insights

Enterprise Demand for Hyper-Automation and Cost Efficiency

Organizations are consolidating scattered point tools into unified agent stacks that compress cycle times and shrink payroll outlays, especially in finance, human resources, and procurement. Agents remain resilient when user interfaces or data schemas shift, which avoids the costly re-scripting that undermined earlier robotic process automation efforts. In high-wage regions, deployments now attain payback in under one year, strengthening board-level sponsorship. Banking compliance teams, for example, deploy agents that monitor transactions in real time, achieving double-digit reductions in false positives while maintaining regulatory audit trails. Rising labor costs and persistent skills gaps further magnify the appeal of digital labor, ensuring that demand for hyper-automation will stay elevated across both mature and emerging economies.

Rapid Advances in Large Language Models and Tool-Orchestration Frameworks

Frameworks such as LangGraph, AutoGen, and CrewAI allow developers to chain specialized agents for data retrieval, code execution, and reasoning into cohesive workflows that approximate human analyst performance. OpenAI's Frontier platform introduced out-of-the-box templates for contract reviews, customer support triage, and supply chain diagnostics, cutting deployment cycles from quarters to weeks. Context windows have leapt from 32,000 tokens in early 2025 to more than 200,000, enabling agents to process entire code bases or multi-year ledgers in a single pass, a capability prized for root-cause investigations in manufacturing. Vertically tuned models backed by safety guardrails are addressing concerns about hallucinations, which is widening adoption in regulated fields that require deterministic rollback and comprehensive audit trails.

High Implementation Costs and Legacy Integration Challenges

Embedding agents into decades-old enterprise resource planning and customer management platforms demands custom connectors, data harmonization, and exhaustive regression testing. Mainframe environments that still power banking and insurance add another layer of complexity because COBOL interfaces lack modern APIs, which increases latency and failure risk. On-premise rollouts also require specialized GPU clusters, which entail capital expenditures ranging from USD 0.5 million to USD 2 million for mid-sized estates. While outcome-based pricing shifts some risk to vendors, it compresses their margins and restricts the pool of capable integrators. These factors prolong project timelines and temper near-term adoption despite compelling total cost-of-ownership calculations.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Infrastructure Expansion and Lower Inference Costs

- Emergence of Multi-Agent Governance Standards Enabling Cross-Vendor Interoperability

- Data Privacy and Regulatory Uncertainty

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid deployments are expanding at a 20.23% annual clip through 2031 as firms route sensitive inference workloads, such as patient records or credit-risk models, to on-premise nodes while leveraging cloud elasticity for batch analytics and public-facing chatbots. Cloud offerings accounted for 61.74% of 2025 revenue due to rapid provisioning and vendor-maintained updates, yet data residency statutes in Germany and Switzerland limit pure-cloud penetration. Microsoft Azure Stack, AWS Outposts, and similar solutions replicate cloud control planes on local hardware, enabling developers to invoke identical APIs regardless of location. The agentic enterprise software market size for hybrid solutions is forecast to accelerate as emerging interoperability protocols reduce configuration overhead and as edge use cases, from robotics to retail kiosks, demand sub-100-millisecond response times.

Regulators are nudging adoption toward hybrid models by requiring that high-risk inference logs remain within sovereign borders, thereby guarding against vendor lock-in by keeping mission-critical data onsite. Enterprises cut egress bills by keeping latency-sensitive tokens local while bursting non-critical jobs to spot instances priced up to 80% below on-demand rates. As multi-cloud governance matures, agents will increasingly orchestrate tasks across AWS, Azure, and Google Cloud within a single workflow, thereby diversifying runtime risk and amplifying resilience.

Software accounted for 58.42% of 2025 spending, yet the agentic enterprise software market share mix is shifting as services register a 20.03% CAGR, mirroring the difficulty of stitching agents into heterogeneous estates. Data engineering, schema mapping, and safety testing can swallow 30% to 50% of first-year budgets, while hourly rates for specialized engineers reach USD 300 in major hubs. Outcome-based managed services that commit to definitive performance benchmarks are attracting mid-market buyers that lack in-house machine-learning talent.

OpenAI's Frontier Alliances with global consultancies formalize this ecosystem by pooling model expertise with change-management playbooks, shrinking pilot timelines in heavily regulated verticals. Training programs from hyperscalers certify thousands of practitioners in prompt engineering and red-teaming, further fueling services growth. The agentic enterprise software market size for managed offerings is set to expand as vendors assume operational risk, though margin pressures may induce consolidation among undercapitalized startups.

Geography Analysis

North America accounted for 39.68% of 2025 revenue, driven by the presence of established technology incumbents and a favorable regulatory environment. The region's market stronghold is attributed to its early adoption of advanced technologies and significant investments in innovation. However, the Asia-Pacific is expected to achieve the highest regional CAGR of 20.63% through 2031. Countries such as China, Japan, India, and South Korea are heavily investing in indigenous model training and local inference clusters to ensure data sovereignty. This focus has led to increased demand for on-premise accelerators and open-source tools, positioning the region as a key growth driver in the market. Meanwhile, Europe faces slower rollouts due to its stringent privacy regulations, but this approach fosters long-term trust, which could serve as a competitive advantage for vendors in the region.

The Middle East and Africa are channeling oil windfall revenues into the development of AI hubs, though current use remains concentrated in sectors such as energy and public services. These investments aim to diversify regional economies and enhance technological capabilities. In Latin America, growth is primarily centered around Brazil and Argentina, where digital banking and retail pilots are successfully demonstrating the value of AI in fraud detection and personalized merchandising. These advancements highlight the region's potential for AI adoption, despite challenges such as economic instability and infrastructure limitations.

Hyperscaler region build-outs in countries like Malaysia, Thailand, and Saudi Arabia are reducing latency for edge-heavy workloads, further enabling the adoption of advanced technologies. These developments are complemented by the World Economic Forum's governance framework, which provides a standardized vocabulary for enterprises to harmonize multi-jurisdiction deployments. This framework is particularly beneficial for organizations operating across diverse regulatory environments, ensuring smoother integration and compliance. Collectively, these regional dynamics underscore the global momentum toward AI adoption, with varying growth trajectories influenced by local policies, investments, and technological readiness.

- Microsoft Corporation

- Salesforce Inc

- ServiceNow Inc

- Amazon Web Services Inc

- Google Cloud (Alphabet Inc)

- IBM Corporation

- OpenAI LLC

- Anthropic PBC

- Cohere Inc

- Adept AI Labs

- NVIDIA Corporation

- UiPath Inc

- Aisera Inc

- DataRobot Inc

- Cognigy GmbH

- SAP SE

- Snowflake Inc

- Oracle Corporation

- Baidu Inc

- Automation Anywhere Inc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Enterprise Demand for Hyper-Automation and Cost Efficiency

- 4.2.2 Rapid Advances in Large Language Models and Tool-Orchestration Frameworks

- 4.2.3 Cloud Infrastructure Expansion and Lower Inference Costs

- 4.2.4 Emergence of Multi-Agent Governance Standards Enabling Cross-Vendor Interoperability

- 4.2.5 Sector-Specific Responsible AI Frameworks Unlocking Regulated Industry Adoption

- 4.2.6 Availability of Outcome-Based Pricing Models Accelerating Mid-Market Uptake

- 4.3 Market Restraints

- 4.3.1 High Implementation Costs and Legacy Integration Challenges

- 4.3.2 Data Privacy and Regulatory Uncertainty

- 4.3.3 Scarcity of Safety-Alignment Engineering Talent

- 4.3.4 Absence of Enterprise-Grade Agent Reliability Benchmarks

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Industry Vertical

- 5.4.1 Banking Financial Services and Insurance BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Manufacturing

- 5.4.4 Retail and E-Commerce

- 5.4.5 Information Technology and Telecom

- 5.4.6 Government and Public Sector

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Salesforce Inc

- 6.4.3 ServiceNow Inc

- 6.4.4 Amazon Web Services Inc

- 6.4.5 Google Cloud (Alphabet Inc)

- 6.4.6 IBM Corporation

- 6.4.7 OpenAI LLC

- 6.4.8 Anthropic PBC

- 6.4.9 Cohere Inc

- 6.4.10 Adept AI Labs

- 6.4.11 NVIDIA Corporation

- 6.4.12 UiPath Inc

- 6.4.13 Aisera Inc

- 6.4.14 DataRobot Inc

- 6.4.15 Cognigy GmbH

- 6.4.16 SAP SE

- 6.4.17 Snowflake Inc

- 6.4.18 Oracle Corporation

- 6.4.19 Baidu Inc

- 6.4.20 Automation Anywhere Inc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment