PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063453

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063453

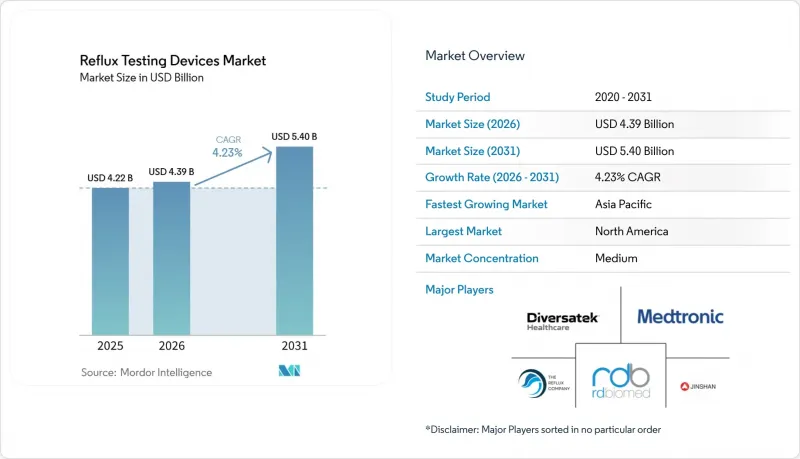

Reflux Testing Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the reflux testing devices market size is projected to expand from USD 4.22 billion in 2025 and USD 4.39 billion in 2026 to USD 5.40 billion by 2031, registering a CAGR of 4.23% between 2026 to 2031.

This report is Segmented by Product (pH Monitoring Systems, PH-Impedance Monitoring Systems, Wireless PH Capsule Systems, and More), End-User (Hospitals, Ambulatory Surgical Centers, Specialty GI Clinics, and More), Indication (GERD, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Reflux Testing Devices Market Trends and Insights

Updated Reflux Testing Guidelines Standardize Ambulatory Monitoring Decisions

The Lyon Consensus 2.0 framework defines acid exposure time above 6% as conclusive for GERD and below 4% as exclusionary, eliminating subjective gray zones and prompting hospitals to replace recorders that lack automated calculations of mean nocturnal baseline impedance and post-reflux swallow-induced peristaltic wave. Diversatek integrated these metrics into its Zvu 3.4.0 release in June 2025, enabling simultaneous manometry and pH analysis within a single interface . FDA 510(k) clearances now require proof of Lyon metric accuracy, encouraging vendors to embed objective scoring engines and accelerating software-driven refresh cycles. Longer wireless protocols are also mandated for patients with negative 24-hour catheter results, uncovering additional positives and expanding procedural volumes.

Wireless Capsule-Based Monitoring Enables Longer Studies and Better Tolerance

Wireless systems extend observation to 96 hours, reveal circadian acid patterns, and record symptom events during real-world activities that nasal probes disrupt. Patient willingness to repeat wireless testing reaches 90% versus 50% for catheters, a compliance edge that boosts longitudinal monitoring of refractory cases. Medtronic's 2025 recall briefly constrained supply, but it also triggered hospital evaluations of Jinshan's alpHaFLEX device, which offers 50 Hz sampling and native Lyon metrics, and of Diversatek's ZepHr capsule, both of which secured new multiyear contracts during the recall gap .

Patient Aversion to Nasal Catheters Dampens Test Uptake

Despite the advantages of real-time impedance data, nasal probes deter repeat testing. Research shows that only half of subjects would repeat a catheter study, versus 90% for wireless capsules. Manufacturers have introduced softer polyurethane probes, but tolerance gaps persist, especially in the Asia-Pacific region, where cultural expectations favor non-invasive approaches. Reduced uptake delays diagnosis in atypical reflux cases, perpetuating empirical PPI therapy without objective evidence.

Other drivers and restraints analyzed in the detailed report include:

- Rising GERD and Extraesophageal Symptom Burden Expands Testing Referrals

- Hospital Dominance and Installed-Base Upgrades Sustain Replacement Demand

- Coverage Variability and Prior Authorization Hurdles for Prolonged Tests

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wireless pH Capsule Systems held 23.14% market share in 2025 and will expand at a 5.23% CAGR through 2031, the fastest growth among product segments, driven by 96-hour monitoring windows that capture symptom-reflux correlations missed by 24-hour catheter studies and patient-tolerance advantages that reduce study abandonment. Medtronic's June 2025 Class I recall of Bravo CF capsule delivery devices-linked to 33 serious injuries from adhesive manufacturing defects-temporarily disrupted supply but accelerated evaluations of Jinshan's alpHaFLEX wireless system, which samples at 50 Hz and integrates Lyon Consensus metrics, including post-reflux swallow-induced peristaltic wave detection, offering hospitals a differentiated alternative during the recall period.

pH-Impedance Monitoring Systems, the second-largest segment, benefit from Lyon Consensus 2.0's emphasis on mean nocturnal baseline impedance and bolus clearance metrics, which require impedance channels that catheter-based pH-only systems lack, compelling hospitals to upgrade legacy recorders to multi-modal platforms. Catheter-based pH Monitoring Systems face structural headwinds from patient aversion-only 50% of subjects are willing to repeat, versus 90% for wireless-but retain niche utility for pre-operative assessments, where real-time impedance waveforms guide surgical planning.

Geography Analysis

North America held 46.54% of global revenue in 2025. Growth will moderate as the mature installed base meets reimbursement friction for prolonged wireless studies, yet hospital GI suite modernization projects keep modest capital flowing. Ambulatory surgical centers are expanding reflux testing volumes due to risk-sharing payment models. Canada and Mexico remain underpenetrated because specialist density is lower and provincial formularies emphasize endoscopy.

Asia-Pacific is projected to log a 6.34% CAGR, the fastest worldwide. China's 43.3 million annual endoscopies create a large procedural funnel, but ambulatory pH monitoring remains concentrated in tier-1 hospitals until regional facilities add trained staff. Domestic vendors like Jinshan leverage lower price points and local service to penetrate rapidly. India's private hospital chains are early adopters of wireless capsules, although out-of-pocket payment norms temper growth outside metro areas. Developed markets such as Japan, South Korea, and Australia mirror North American replacement patterns but favor non-invasive tools due to cultural preferences.

Europe presents a fragmented payer environment. CE-marked devices face varying remuneration, as illustrated by RefluxStop implant prices ranging from EUR 15,100 to 48,000. Public systems stress the need for cost-effectiveness evidence, pushing manufacturers to supply robust health economic data. Germany and the United Kingdom lead adoption, while Southern European markets progress more slowly due to budget constraints.

- Alacer Biomedica

- Biomedix

- Cook Group

- Creo Medical Group

- Diversatek Healthcare

- EB Neuro

- EndoGastric Solutions

- Johnson & Johnson

- Laborie Medical Technologies

- Mederi Therapeutics Inc

- Medtronic

- Olympus

- RD Biomed

- Shenzhen Jinshan Science & Technology Co., Ltd.

- Standard Instruments GmbH

- Synectics Medical Ltd (SynMed UK)

- The Reflux Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Updated Reflux Testing Guidelines Standardize Ambulatory Monitoring Decisions

- 4.2.2 Wireless Capsule-Based Monitoring Enables Longer Studies and Better Tolerance

- 4.2.3 Rising GERD And Extraesophageal Symptom Burden Expands Testing Referrals

- 4.2.4 Hospital Dominance and Installed-Base Upgrades Sustain Replacement Demand

- 4.2.5 Lyon Consensus 2.0 Metrics Embedded in Software Drive Objective Adoption

- 4.2.6 IDN And VA Procurement Standardization Consolidates Device Choices

- 4.3 Market Restraints

- 4.3.1 Patient Aversion to Nasal Catheters Dampens Test Uptake

- 4.3.2 Coverage Variability and Prior Authorization Hurdles For LPR/Prolonged Tests

- 4.3.3 Specialist Capacity and Training Gaps Slow Throughput

- 4.3.4 Limited US Clearance for Some Non-US Systems Constrains Competition

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 pH Monitoring Systems (Catheter-based)

- 5.1.2 pH-Impedance Monitoring Systems (MII-pH)

- 5.1.3 Wireless pH Capsule Systems

- 5.1.4 Oropharyngeal pH Monitoring Systems

- 5.1.5 Accessories & Consumables

- 5.2 By End-User

- 5.2.1 Hospitals

- 5.2.2 Ambulatory Surgical Centers (ASCs)

- 5.2.3 Specialty GI Clinics

- 5.2.4 Diagnostic Centers & Labs

- 5.3 By Indication

- 5.3.1 Gastroesophageal Reflux Disease (GERD)

- 5.3.2 Pre-/Post-operative Evaluation (Anti-reflux, Bariatric)

- 5.3.3 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Alacer Biomedica

- 6.3.2 Biomedix

- 6.3.3 Cook Medical Inc

- 6.3.4 Creo Medical Group PLC

- 6.3.5 Diversatek Healthcare

- 6.3.6 EB Neuro S.p.A.

- 6.3.7 EndoGastric Solutions

- 6.3.8 Johnson & Johnson

- 6.3.9 Laborie Medical Technologies

- 6.3.10 Mederi Therapeutics Inc

- 6.3.11 Medtronic plc

- 6.3.12 Olympus Corporation

- 6.3.13 RD Biomed

- 6.3.14 Shenzhen Jinshan Science & Technology Co., Ltd.

- 6.3.15 Standard Instruments GmbH

- 6.3.16 Synectics Medical Ltd (SynMed UK)

- 6.3.17 The Reflux Company

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment