PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063455

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063455

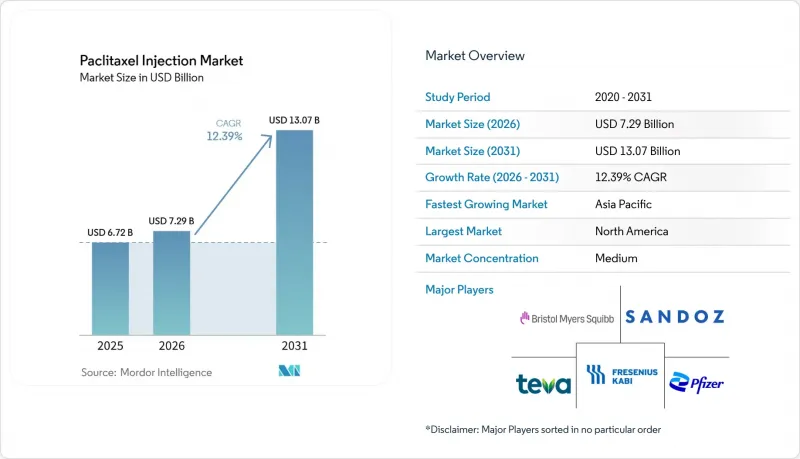

Paclitaxel Injection - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the paclitaxel injection market size is expected to grow from USD 6.72 billion in 2025 to USD 7.29 billion in 2026 and is forecast to reach USD 13.07 billion by 2031 at 12.39% CAGR over 2026-2031.

This report is Segmented by Formulation (Solvent-Based Paclitaxel Injection, Albumin-Bound Paclitaxel Injection, and More), Indication (Breast Cancer, Non-Small Cell Lung Cancer, and More), End User (Hospitals, Dedicated Cancer Centers & Oncology Clinics, and More), Distribution Channel (Hospital Pharmacies, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Paclitaxel Injection Market Trends and Insights

Rising Global Incidence of Breast, Lung, And Ovarian Cancers

Global cancer incidence continues to increase, with breast cancer cases projected to reach 3.2 million annually by 2050, up from 2.3 million in 2022, which sustains the use of taxane-based regimens where biomarker-directed options are not suitable or reimbursed. In the United States, 2026 care pathways remain anchored by chemotherapy in several settings, supported by an estimated 316,950 new breast cancer cases and 226,650 lung cancer cases reported for 2025, which underscores enduring demand for paclitaxel-based combinations when immune or targeted therapies are unavailable or suboptimal. Ovarian cancer's global burden, with substantial mortality, reflects access gaps to companion diagnostics and maintenance therapies that keep paclitaxel relevant in first-line and recurrent protocols across many health systems. As population aging concentrates incidence in middle- and high-income markets and screening broadens in emerging economies, chemotherapy backbones remain critical adjuncts to evolving targeted and immuno-oncology regimens, which stabilize the paclitaxel injection market in core tumor types. These epidemiology trends reinforce formulary continuity for paclitaxel, where clinical guidelines still include taxanes for standard-of-care regimens or for patients who do not meet biomarker thresholds for newer agents

Inclusion Of Paclitaxel On WHO Essential Medicines Lists And National Formularies

Paclitaxel's inclusion on national essential medicines lists anchors institutional purchasing in low- and middle-income countries, with Zambia's 2025 Essential Medicines List classifying paclitaxel 6 mg/mL IV solution as vital for tertiary hospitals. Despite this inclusion, availability remains uneven, with access to cytotoxics such as paclitaxel significantly lower in low- and lower-middle-income settings compared with high-income countries, which highlights persistent infrastructure and financing gaps. Essential-medicine designation supports multi-year tenders and pooled procurement, which contributes to steadier demand volumes and prioritizes stock protection where sterile-injectable shortages are a system risk. In practice, national formularies that emphasize broad-indication chemotherapies ensure backstop options when targeted pathways fail, or biomarker testing is incomplete, which sustains the paclitaxel injection market through varied lines of therapy. Over time, formulary placement, paired with local manufacturing and multi-supplier contracts, helps align cost containment with treatment continuity for hospital-based oncology, which supports more predictable purchasing across budget cycles.

Toxicity Profile (Myelosuppression, Neuropathy) And Solvent-Related Hypersensitivity

Neutropenia remains a central dose-limiting toxicity for paclitaxel, with grade 3-4 events documented in patients receiving nab-paclitaxel regimens and necessitating regular monitoring and treatment holds when neutrophil counts fall below defined thresholds. Peripheral neuropathy accumulates with exposure and can lead to dose reductions or discontinuations, which affects regimen adherence and patient quality of life in long courses of therapy. Solvent-based paclitaxel carries a known hypersensitivity risk linked to Cremophor EL, which requires steroid and antihistamine premedication and reinforces the need for supervised infusions in settings equipped for immediate reaction management. FAERS pharmacovigilance indicates that hematologic events are the leading safety signal for nab-paclitaxel, which highlights the importance of complete blood counts and supportive care across cycles. These risk factors shape clinician choice between solvent-based and solvent-free options and sustain the clinical rationale for regimen adjustments and dose intensity management in practice.

Other drivers and restraints analyzed in the detailed report include:

- Institutional Administration Model Concentrates Demand In Hospital Oncology Settings

- Adoption Of Solvent-Free And Nano-Enabled Formulations Expands Eligible Patient Populations

- Regimen Displacement Risk From Targeted And Immuno-Oncology Therapies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solvent-based paclitaxel held 56.2% of 2025 revenues, reflecting legacy protocols, broad availability, and established infusion practices that rely on prophylactic steroids and antihistamines to mitigate Cremophor EL-related reactions. The paclitaxel injection market size for liposomal and polymeric-micelle formulations is projected to expand at 15.31% CAGR between 2026 and 2031, as solvent-free delivery and improved intracellular uptake broaden patient eligibility and reduce chair time relative to three-hour solvent-based infusions. Nab-paclitaxel's omission of solvent premedication and its 30-minute infusion profile align with high-throughput outpatient operations, which support faster turnover in cancer centers with constrained infusion chairs. Generic competition across the U.S. and EU has eroded the originator's position and redirected purchasing toward multi-supplier panels, with EU approvals such as Naveruclif and Apexelsin reinforcing access in markets that run centralized tenders. As the paclitaxel injection market absorbs greater generic depth, clinical selection within solvent-free options will depend on local outcomes data, site of care protocols, and payer policies for substitution, rather than on branded differentiation.

The paclitaxel injection industry is likely to see further formulation innovation in micellar and liposomal carriers, contingent on Phase III evidence and regulator alignment on bioequivalence or superiority endpoints. Across 2026-2031, unit growth in solvent-free categories will reflect payer openness to generic substitution, guideline integration for specific tumor types, and the operational goals of infusion centers to increase chair throughput without sacrificing safety. These factors together reinforce the multi-year shift toward solvent-free platforms within the paclitaxel injection market.

Breast cancer contributed 36.5% of 2025 revenues, reflecting the persistent role of taxanes across neoadjuvant, adjuvant, and metastatic care when sequencing after anthracycline or when targeted options are exhausted. The paclitaxel injection market size for pancreatic applications is poised to grow at a 15.44% CAGR through 2031, anchored by the gemcitabine plus nab-paclitaxel doublet that improved median overall survival to 8.5 months versus 6.7 months in the MPACT study, which established the regimen as a standard for metastatic disease. In NSCLC, displacement by checkpoint inhibitors has reduced first-line taxane doublet use in eligible patients, although paclitaxel maintains relevance for those who do not meet immunotherapy criteria or require later-line chemotherapy. Ovarian cancer continues to support steady taxane volume, with paclitaxel plus platinum combinations used broadly in first-line settings and in defined recurrent contexts, especially where biomarker-directed maintenance is not feasible or reimbursed. Cervical cancer and AIDS-related Kaposi's sarcoma represent smaller shares, but essential-medicine status in national formularies preserves procurement and clinical availability in resource-limited settings.

Across tumor types, guideline recommendations and payer policies will shape taxane use over time, with expansion likely in gastrointestinal and gynecologic settings where combination regimens with immunotherapy have gained approvals. Regulatory developments in Asia have recognized combinations that incorporate paclitaxel with checkpoint inhibitors in gynecologic malignancies, which signals continuing integration of taxanes within multi-agent protocols. The paclitaxel injection market therefore stays diversified across indications, with growth most visible in pancreatic cancer and in combination regimens that preserve or extend chemotherapy utility. Over the forecast period, real-world data and tolerability in routine practice will be central to sustaining regimen adherence and optimizing outcomes within each indication.

Geography Analysis

North America accounted for 43.2% of 2025 revenues, supported by established treatment pathways, oncologist familiarity with taxane regimens, and reimbursement coverage across solvent-based and albumin-bound formulations. The paclitaxel injection market in the United States has shifted toward multi-supplier purchasing after 2024-2025 generic launches, which accelerated price competition and eroded the originator's sales as hospital GPOs reinforced substitution to approved generics. Company disclosures show continued revenue pressure on the originator brand in late 2025, which illustrates how tender competition and formulary substitution drive rapid share shifts in hospital oncology. Canada and Mexico contribute smaller shares, with budget differences shaping the mix between solvent-based and solvent-free products across public and private providers. The paclitaxel injection market remains stable in North America as chemotherapy continues to complement biomarker-driven therapies and supports care sequences after targeted therapy resistance.

Europe represented an estimated 25.30% of 2025 revenues, led by Germany, France, Italy, Spain, and the United Kingdom. EMA marketing authorizations for generic nab-paclitaxel products such as Naveruclif and Apexelsin broadened options for hospitals that procure through centralized tenders and prefer multi-supplier awards for inventory resilience. Product-specific bioequivalence guidance is harmonizing evidence expectations across EU markets, which improves payer confidence in substitutable options and supports cross-border distribution under unified labeling standards. National-level updates to generic product characteristics and safety information continue through Type II variations, which keep labels aligned with originator references and pharmacovigilance requirements. Over 2026-2031, the paclitaxel injection market in Europe should maintain steady unit volumes on demographic drivers, with revenue growth moderated by generic saturation and price convergence under tender frameworks.

Asia-Pacific is the fastest-growing region for the paclitaxel injection market with a forecast CAGR of 14.12%, reflecting rising cancer incidence, expanding oncology infrastructure, and domestic manufacturing scale in China and India. In China, local approvals for albumin-bound paclitaxel have strengthened domestic supply, which supports broader access under public procurement rules and eases dependence on imports. Regulatory approvals for regimens that include paclitaxel in gynecologic malignancies, such as durvalumab-based combinations, broaden the addressable patient base for taxanes in hospital and certified outpatient settings. India's role as a scaled manufacturer and exporter of oncology injectables reinforces regional and global supply, aided by global approvals that validate product quality and support hospital tenders. Japan, Australia, and South Korea generate higher per-capita revenues due to reimbursement environments that cover solvent-free options, with Japan integrating taxanes into combinations that sustain chemotherapy utilization in defined populations as immunotherapy expands. In the Middle East and Africa and in South America, lower shares reflect oncology infrastructure constraints and public funding limits, though government tenders and essential-medicine programs sustain baseline procurement when budgets permit. Over the forecast period, the paclitaxel injection market in emerging regions should gradually expand as universal health coverage programs evolve and as multi-supplier sourcing reduces stockout exposure.

- Accord Healthcare

- Alembic Pharmaceuticals

- American Regent

- Apotex

- Aurobindo Pharma Limited.

- Bristol-Myers Squibb

- Cipla

- Dr. Reddy's Laboratories

- Fresenius

- GLAND PHARMA

- Hikma Pharmaceuticals

- Inceptua Group

- Intas Pharmaceutical

- Lupin

- medac GmbH

- Pfizer

- SAGENT

- Sandoz Group AG

- Stada Arzneimittel

- Sun Pharmaceuticals Industries

- Teva Pharmaceutical Industries

- Zydus Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Incidence Of Breast, Lung, And Ovarian Cancers

- 4.2.2 Inclusion Of Paclitaxel On Who Essential Medicines Lists And National Formularies

- 4.2.3 Institutional Administration Model Concentrates Demand In Hospital Oncology Settings

- 4.2.4 Adoption Of Solvent Free And Nano-Enabled Formulations Expands Eligible Patient Populations

- 4.2.5 EMA Bioequivalence Pathway For Nab Paclitaxel Enables Faster Eu Generic Entry

- 4.2.6 Broader Availability From Recent Nab Paclitaxel Generic Launches (US/EU)

- 4.3 Market Restraints

- 4.3.1 Toxicity Profile (Myelosuppression, Neuropathy) And Solvent Related Hypersensitivity

- 4.3.2 Regimen Displacement Risk From Targeted And Immuno-Oncology Therapies

- 4.3.3 Sterile Injectable Supply Shocks And Manufacturing/Quality Disruptions

- 4.3.4 Price Compression From Tendering And China VBP On Protein Bound Paclitaxel

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Formulation

- 5.1.1 Solvent Based Paclitaxel Injection

- 5.1.2 Albumin Bound Paclitaxel Injection

- 5.1.3 Liposomal / Polymeric Micelle Paclitaxel Injection

- 5.1.4 Others (Polymeric Micelle Paclitaxel Injection, Emulsion Based Paclitaxel Injection)

- 5.2 By Indication

- 5.2.1 Breast Cancer

- 5.2.2 Non-Small Cell Lung Cancer (NSCLC)

- 5.2.3 Ovarian Cancer

- 5.2.4 Pancreatic Adenocarcinoma

- 5.2.5 AIDS Related Kaposis Sarcoma

- 5.2.6 Others (Cervical Cancer, Endometrial Cancer)

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Dedicated Cancer Centers & Oncology Clinics

- 5.3.3 Ambulatory/Day Care Infusion Centers

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Specialty Pharmacies

- 5.4.3 Retail & Online Pharmacies

- 5.4.4 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Accord Healthcare

- 6.3.2 Alembic Pharmaceuticals Limited

- 6.3.3 American Regent, Inc.

- 6.3.4 Apotex Inc.

- 6.3.5 Aurobindo Pharma Limited.

- 6.3.6 Bristol-Myers Squibb Company

- 6.3.7 Cipla

- 6.3.8 Dr. Reddys Laboratories Ltd.

- 6.3.9 Fresenius Kabi AG

- 6.3.10 Gland Pharma Limited

- 6.3.11 Hikma Pharmaceuticals PLC

- 6.3.12 Inceptua Group

- 6.3.13 Intas Pharmaceuticals Ltd.

- 6.3.14 Lupin

- 6.3.15 medac GmbH

- 6.3.16 Pfizer Inc.

- 6.3.17 SAGENT

- 6.3.18 Sandoz Group AG

- 6.3.19 STADA Arzneimittel AG

- 6.3.20 Sun Pharmaceutical Industries Ltd.

- 6.3.21 Teva Pharmaceutical Industries Ltd.

- 6.3.22 Zydus Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment