PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063457

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063457

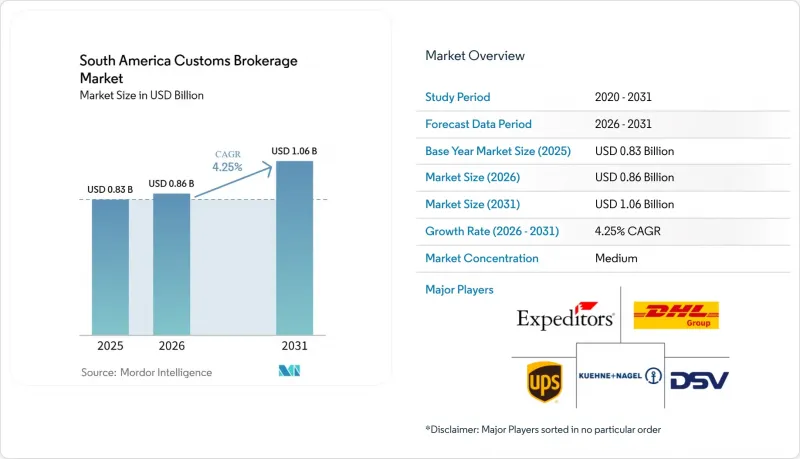

South America Customs Brokerage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the south america customs brokerage market size was valued at USD 826.83 million in 2025 and estimated to grow from USD 862.6 million in 2026 to reach USD 1062.25 million by 2031, at a CAGR of 4.25% during the forecast period (2026-2031).

Growing e-commerce parcel flows, regional single-window programs, and near-shoring by automotive and electronics manufacturers keep volumes resilient even as tariff schedules change each quarter. This report is Segmented by Mode of Transport (Ocean, Air, and More), by Broker Type (Pure Customs Broker, Freight Forwarder), by Importer Size (Large Enterprises, Mid-Market, and More), by Digital Adoption (Traditional, API-Based), by End-User (Retail and E-Commerce, Automotive and More), and by Country (Brazil, Colombia, and More ). The Market Forecasts are Provided in Terms of Value (USD).

South America Customs Brokerage Market Trends and Insights

Cross-Border E-Commerce Boom

Low-value parcels already form more than one-quarter of customs declarations in Brazil, Argentina, and Chile, pushing brokers to process higher transaction counts for lower fees. Brazil's Remessa Conforme program enrolls 67% of inbound parcels and collects duties upfront, shifting brokerage work upstream to platforms like Mercado Libre. Colombia's USD 5,000 simplified-declaration ceiling achieves a similar effect and accelerates SME imports. Argentina's SUCA portal handled 3.2 million parcels in its first year, encouraging brokers to automate rather than re-key data. Accelerated clearance cycles enlarge the addressable South America customs brokerage market as more merchants begin exporting directly.

Mercosur & Pacific Alliance Trade Facilitation

The AEO-reciprocity pact signed in 2025 covers 570 Colombian companies and removes duplicate compliance audits across five economies. Brazil and Argentina activated the AFC PLUS system in 2026, imposing 12-hour targets for green-channel cargo and creating predictable dwell times. Chile integrated certificate-of-origin exchanges with Mexico, Peru, and Colombia, while Peru's VUCE mandates full inter-agency linkage by December 2026. Harmonized processes enlarge the South America customs brokerage market because exporters expand intra-regional trade when clearance risk falls.

Complex & Frequently Changing Tariff Schema

Argentina adjusted Common External Tariff exceptions 14 times in two years, forcing brokers to monitor gazettes daily. Brazil's dual-VAT rollout runs to 2033, so declarations must calculate legacy and new levies in parallel. Colombia will replace criminal sanctions with administrative fines in 2026, increasing audit volume. Frequent rule changes add cost and slow the South America customs brokerage market growth by deterring smaller entrants.

Other drivers and restraints analyzed in the detailed report include:

- Digital Customs-Clearance Platforms (Single Window, Blockchain)

- Near-Shoring of Supply Chains into South America

- High Logistics Costs & Port Congestion

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air express and general cargo will post a 5.46% CAGR through 2031, even though ocean freight controlled 47.33% of the South America customs brokerage market share in 2025. Small parcels propel the modal shift under the USD 50 Remessa Conforme ceiling and by vaccine consignments that demand 2-to-8 °C chains of custody. IATA's ONE Record adoption hit 22% in 2025, allowing brokers to auto-populate declarations from airline data feeds.

Ocean and sea lanes remain vital for grains, chemicals, and automotive knockdown kits, yet importers increasingly negotiate all-in contracts that bundle freight, insurance, and clearance. Truck and rail flows on trans-Andean corridors use TIR carnets that suspend duties until arrival, a service niche for brokers fluent in land-border inspection rules. As digital-first filing systems mature, the South America customs brokerage market size tied to air express should keep widening.

Freight forwarders and 3PL-integrated operators captured 60.67% of the South America customs brokerage market share because enterprise shippers value a single liability point. On-dock brokerage suites in Santos and Buenos Aires shorten door-to-door cycles and encourage "vendor-managed clearance" contracts. However, pure customs brokers are forecast to grow at 4.88% CAGR by offering audit defense, drawback recovery, and classification advice under Mercosur automotive rules.

Traditional relationship capital with inspectors still matters for yellow-channel cargo, but API-driven entrants now match that advantage by hiring ex-officials and overlaying real-time tariff databases. The South America customs brokerage market, therefore, splits between scale-based service bundles and high-skill advisory retainers.

List of Companies Covered in this Report:

- DHL Global Forwarding

- DSV

- Kuehne + Nagel

- CEVA Logistics (CMA CGM)

- Maersk Customs Services

- UPS Supply Chain Solutions

- Expeditors International

- FedEx Logistics

- Hellmann Worldwide Logistics

- GEODIS

- Rhenus Logistics

- Noatum Logistics

- Yusen Logistics

- TIBA Group

- Grupo RAS

- Allink Transportes

- Aduana Brokerage Services (ABS Group)

- Agunsa

- Ultramar

- FS Agencia de Aduanas

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cross-Border E-Commerce Boom

- 4.2.2 Mercosur & Pacific Alliance Trade Facilitation

- 4.2.3 Digital Customs-Clearance Platforms (Single Window, Blockchain)

- 4.2.4 Near-Shoring of Supply Chains into South America

- 4.2.5 Emergence of Amazonian Free-Trade Zones

- 4.2.6 Carbon-Footprint Disclosure in Customs Paperwork

- 4.3 Market Restraints

- 4.3.1 Complex & Frequently Changing Tariff Schema

- 4.3.2 High Logistics Costs & Port Congestion

- 4.3.3 Patchy Digital-Signature Laws Across Countries

- 4.3.4 Ageing Certified-Broker Talent Pool

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Geo-Political Events

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Mode of Transport (Value)

- 5.1.1 Ocean / Sea

- 5.1.2 Air (Express and General Cargo)

- 5.1.3 Cross-Border Land (Truck and Rail)

- 5.2 By Broker Type

- 5.2.1 Pure Customs Broker

- 5.2.2 Freight Forwarder / 3PL-Integrated Brokers

- 5.3 By Importer Size

- 5.3.1 Large Enterprisess

- 5.3.2 Mid-Market

- 5.3.3 SMEs / Micro-shippers

- 5.4 By Digital Adoption

- 5.4.1 Traditional Brokerages

- 5.4.2 Digital-first / API-based Brokerages

- 5.5 By End-Use Industry

- 5.5.1 Retail and E-commerce

- 5.5.2 Automotive and EV

- 5.5.3 Electronics and Semiconductors

- 5.5.4 Pharmaceuticals and Life Sciences

- 5.5.5 Aerospace and Defense

- 5.5.6 Chemicals and Industrial Goods

- 5.5.7 Others

- 5.6 By Country

- 5.6.1 Brazil

- 5.6.2 Argentina

- 5.6.3 Chile

- 5.6.4 Colombia

- 5.6.5 Peru

- 5.6.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 DHL Global Forwarding

- 6.4.2 DSV

- 6.4.3 Kuehne + Nagel

- 6.4.4 CEVA Logistics (CMA CGM)

- 6.4.5 Maersk Customs Services

- 6.4.6 UPS Supply Chain Solutions

- 6.4.7 Expeditors International

- 6.4.8 FedEx Logistics

- 6.4.9 Hellmann Worldwide Logistics

- 6.4.10 GEODIS

- 6.4.11 Rhenus Logistics

- 6.4.12 Noatum Logistics

- 6.4.13 Yusen Logistics

- 6.4.14 TIBA Group

- 6.4.15 Grupo RAS

- 6.4.16 Allink Transportes

- 6.4.17 Aduana Brokerage Services (ABS Group)

- 6.4.18 Agunsa

- 6.4.19 Ultramar

- 6.4.20 FS Agencia de Aduanas

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment