PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063469

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063469

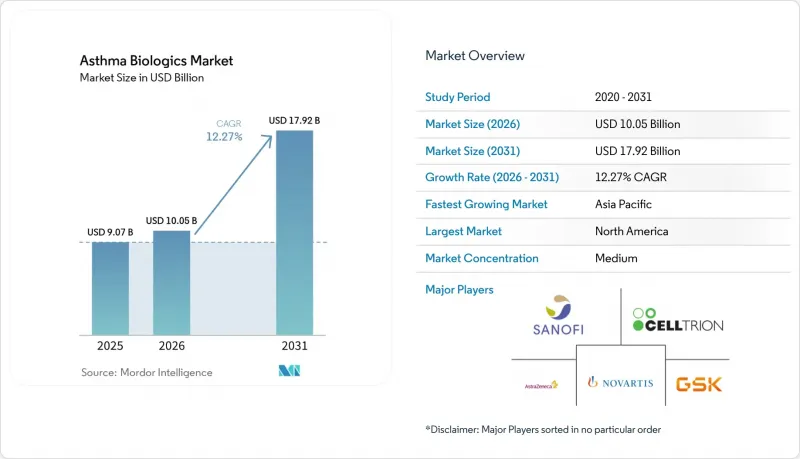

Asthma Biologics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asthma biologics market size was valued at USD 9.07 billion in 2025 and is estimated to grow from USD 10.05 billion in 2026 to reach USD 17.92 billion by 2031, at a CAGR of 12.27% during the forecast period (2026-2031).

This report is Segmented by Mechanism of Action (Anti-IL-4Ra, Anti-TSLP, Anti-IL-5, Anti-IL-5Ra, Anti-IgE), Phenotype (Eosinophilic, Allergic/IgE-mediated, OCS-Dependent, Non-Eosinophilic), Route of Administration (Subcutaneous, Intravenous), End-User (Hospitals, Specialty Clinics, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Asthma Biologics Market Trends and Insights

GINA-Endorsed Add-On Biologics for Severe Uncontrolled Asthma

GINA's 2024-2025 revisions positioned biologics as the standard Step 5 option, giving pulmonologists a guideline-backed rationale to start biologics sooner and decrease prolonged oral corticosteroid exposure. Registry data show 50-70% exacerbation drops within six months of mepolizumab or dupilumab initiation . FDA approval of benralizumab for eosinophilic granulomatosis with polyangiitis in 2024 reinforced class benefits across multiple Type 2 diseases. Payers interpret these outcomes as cost offsets because emergency visits decline when exacerbations fall. However, GINA's biomarker emphasis favors markets with reliable eosinophil and FeNO testing, slowing penetration in regions with limited laboratory capacity.

Broad-Eligibility Agents Expanding Treatable Population Beyond Biomarker-High Patients

Tezepelumab's thymic stromal lymphopoietin blockade demonstrated 56% overall and 41% biomarker-low exacerbation reduction in the NAVIGATOR trial, creating the first biologic option for 25-30% of severe asthma patients who lack elevated eosinophils or IgE . The October 2025 FDA label for chronic rhinosinusitis with nasal polyps further broadens use among ENT specialists. Absence of a predictive biomarker complicates payer value models, prompting six-month reassessment rules, yet early uptake data suggest clinicians are willing to trial the drug in non-eosinophilic cases when alternatives are limited. Growth in Asia-Pacific is poised to accelerate once phenotyping infrastructure becomes more accessible and regional payers adopt value-based coverage.

High Prices and Payer Step Edits Restrict Access and Delay Initiation

Annual biologic costs span USD 30,000-40,000, prompting US insurers to demand documented trials of inhaled steroids and often oral corticosteroids before approval. A 2024 claims review showed 22-28% initial denial rates, extending treatment start by an average of 45 days. Each extra month on steroids lifts fracture risk by 12% and diabetes incidence by 8%. Medicaid applies even tighter rules, while emerging markets rely on out-of-pocket spending except where price-discounted reimbursement.

Other drivers and restraints analyzed in the detailed report include:

- Pediatric Label Expansions and Self/At-Home Administration Improving Uptake

- Real-World Evidence Strengthening Payer Confidence

- Safety and Monitoring Constraints Limit Site-of-Care Flexibility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Anti-IL-4Ra agents retained the largest asthma biologics market share at 44.80% in 2025, yet Anti-TSLP agents are positioned to expand at a 14.49% CAGR through 2031, the fastest among all classes. Dupilumab's broad efficacy across asthma, atopic dermatitis, and CRSwNP underpinned USD 11.6 billion in global sales in 2024, with asthma accounting for roughly 35% of revenue, consolidating the drug's position as a platform therapy. By contrast, tezepelumab's upstream TSLP blockade treats the 25-30% of severe patients who present with low eosinophils, normal FeNO, and minimal IgE, a cohort historically limited to systemic corticosteroids. In NAVIGATOR, tezepelumab cut exacerbations 41% in biomarker-low patients, a feat still unmatched by rival mechanisms. AstraZeneca's October 2025 CRSwNP label expansion now allows ENT specialists to initiate the drug, widening its prescriber base and expanding the asthma biologics market addressable by a single molecule.

Eosinophilic asthma maintained 38.65% of 2025 revenue and remains pivotal to payer coverage algorithms that favor documented eosinophilia. Eosinophilic asthma is also expected to advance at 13.65% CAGR through 2031. This phenotype offers multiple therapeutic options-IL-5, IL-5Ra, and IL-4Ra inhibition-resulting in competitive contracting that keeps prices in check for payers while preserving physician choice.

Biomarker-low severe asthma, historically underserved, shows rapid patient conversion following the approval of tezepelumab, adding thousands of new candidates to the asthma biologics market. Absence of a clear predictive test requires trial-and-error strategies, and insurers frequently mandate six-month reassessment endpoints. Nevertheless, pulmonologists welcome the option because systemic steroids and bronchial thermoplasty offer modest benefit for this group.

Geography Analysis

North America retained 45.12% of the 2025 value, buoyed by payer coverage that reimburses biologics for biomarker-qualified patients despite high list prices. The region benefits from mature pulmonology networks, robust biomarker testing, and quick FDA approvals, making it the reference launch market for new agents like depemokimab. Canada widened access when provinces added mepolizumab and benralizumab to public formularies in 2025, narrowing gaps with US availability.

Europe contributed a significant share of global revenue. Germany's flexible reimbursement fosters early adoption, while the UK's NICE imposes tighter cost-effectiveness filters that slow uptake until negotiated discounts align with QALY thresholds. Southern European countries show variable hospital budgets but follow EMA guidance once national price negotiations conclude. Biosimilar entry is expected to temper spending growth without curtailing access, as seen with omalizumab.

Asia-Pacific posts the fastest growth at 9.48% CAGR, driven by China's price-discounted duplication list entry and Japan's premium innovation pricing for tezepelumab and depemokimab. South Korea and Australia exhibit mid-single-digit growth on the back of expanding private insurance coverage. India remains nascent but could pivot upward when local biosimilars arrive post-2027, lowering costs and enabling broader reach.

- Aimmune Therapeutics

- Alvotech Pharma

- Amgen

- Amneal Pharmaceuticals

- AstraZeneca

- Boehringer Ingelheim

- Celltrion

- Chiesi Farmaceutici S.p.A

- Circassia Pharmaceuticals

- DBV Technologies

- Roche

- GlaxoSmithKline

- Innovent Biologics

- Novartis

- Regeneron Pharmaceuticals

- Sanofi

- Teva Pharmaceutical Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 GINA-Endorsed Add-On Biologics for Severe Uncontrolled Asthma; Strong Exacerbation And OCS-Sparing Outcomes Since 2024

- 4.2.2 Broad-Eligibility Agents (TSLP Pathway) Expanding Treatable Population Beyond Biomarker-High Patients

- 4.2.3 Pediatric Label Expansions and Self/At-Home Administration (Pens, Autoinjectors) Improving Uptake

- 4.2.4 Real-World Evidence Showing Reduced Exacerbations and OCS Use Strengthens Payer and Clinician Confidence

- 4.2.5 Ultra-Long-Acting IL-5 Biologics (Twice-Yearly Dosing) Reduce Treatment Burden and Improve Adherence

- 4.2.6 Co-Morbidity Overlap (CRSwNP, AD, EGPA/HES) Broadens Specialist Adoption and Care Pathways

- 4.3 Market Restraints

- 4.3.1 High Prices and Payer Step Edits/Prior Authorization Restrict Access and Delay Initiation

- 4.3.2 Safety And Monitoring Constraints (E.G., Anaphylaxis Risk/Observation) Limit Site-Of-Care Flexibility

- 4.3.3 Limited Biomarker/Feno Infrastructure in Resource-Constrained Settings Impedes Phenotyping

- 4.3.4 IV Infusion Burden (Reslizumab) Vs SC Options Curbs Adoption in Outpatient/Home Settings

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Mechanism of Action (MoA)

- 5.1.1 Anti-IL-4Ra

- 5.1.2 Anti-TSLP

- 5.1.3 Anti-IL-5

- 5.1.4 Anti-IL-5Ra

- 5.1.5 Anti-IgE

- 5.2 By Phenotype / Biomarker Segment

- 5.2.1 Eosinophilic asthma

- 5.2.2 Allergic asthma

- 5.2.3 OCS-dependent severe asthma

- 5.2.4 Non-eosinophilic asthma

- 5.3 By Route of Administration

- 5.3.1 Subcutaneous

- 5.3.2 Intravenous

- 5.4 By End-user

- 5.4.1 Hospitals

- 5.4.2 Specialty Clinics

- 5.4.3 Home/At-home Settings

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of APAC

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of MEA

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Aimmune Therapeutics

- 6.3.2 Alvotech Pharma

- 6.3.3 Amgen

- 6.3.4 Amneal Pharmaceuticals

- 6.3.5 AstraZeneca PLC

- 6.3.6 Boehringer Ingelheim

- 6.3.7 Celltrion Inc.

- 6.3.8 Chiesi Farmaceutici S.p.A

- 6.3.9 Circassia Pharmaceuticals

- 6.3.10 DBV Technologies

- 6.3.11 F. Hoffmann-La Roche AG

- 6.3.12 GlaxoSmithKline

- 6.3.13 Innovent Biologics

- 6.3.14 Novartis AG

- 6.3.15 Regeneron Pharmaceuticals

- 6.3.16 Sanofi

- 6.3.17 Teva Pharmaceutical Industries

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment