PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063499

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063499

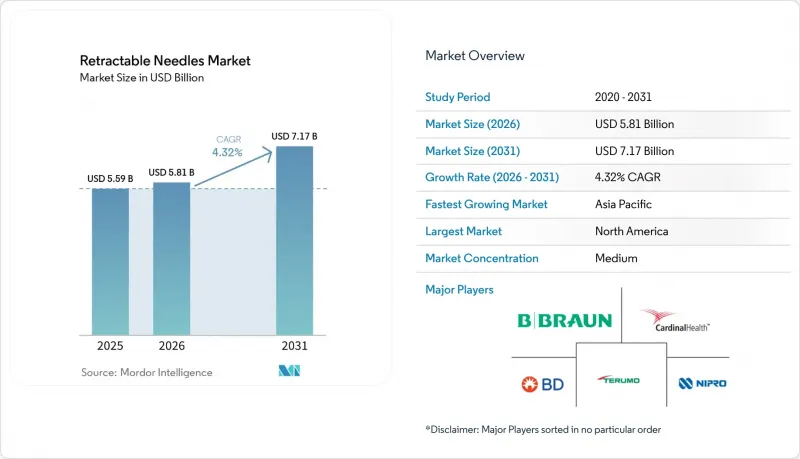

Retractable Needles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the retractable needles market size is expected to increase from USD 5.59 billion in 2025 to USD 5.81 billion in 2026 and reach USD 7.17 billion by 2031, growing at a CAGR of 4.32% over 2026-2031.

This report is Segmented by Product Type (Automatic Retractable Needles, Manual Retractable Needles), Application (Subcutaneous Injections, and More), End User (Hospitals, Clinics and Physician Offices, Ambulatory Surgical Centers, Home Care and Community Health), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Retractable Needles Market Trends and Insights

Rising Injection Volumes From Chronic Diseases And Mass Immunization Programs

Global diabetes prevalence is projected to reach 783 million adults by 2045, and U.S. GLP-1 utilization alone is expected to add roughly 1 billion subcutaneous doses per year by 2030 . Eli Lilly's Zepbound became the top weight-management prescription in 2025, and its Employer Connect channel launched in March 2026 at USD 449 per pen, spurring uptake across 67 million Medicare Part D beneficiaries. Recent FDA approvals of biosimilars Yusimry and Wezlana extend safety-device demand to autoimmune therapies. WHO's 2030 immunization agenda mandates auto-disable syringes for mass campaigns, further embedding retractable technology in emerging markets. Syringe Services Programs, now active in 44 states, distribute sterile sharps that increasingly incorporate passive safety tips in harm-reduction settings.

Regulatory Mandates And Sharps-Injury Prevention Policies Accelerating Safety Device Adoption

OSHA raised fines for serious violations to USD 16,550 and for willful violations to USD 165,514 in January 2025, elevating sharps-injury prevention from a compliance checkbox to a financial priority. Roughly 385,000 U.S. needlestick injuries still occur annually, and the majority of them remain unreported, exposing hospitals to litigation risk . The EU MDR requires safety mechanisms in labeling and packaging, forcing manufacturers to undergo 13- to 18-month CE mark reviews that now bottleneck legacy product renewals. WHO prequalification ties GAVI funding to auto-disable syringes that conform to ISO 23908:2024, effectively hard-wiring retractable needles into low-income immunization tenders. State-level statutes, such as California's AB 2975, further tighten occupational-safety scrutiny and reinforce the commercial case for passive devices.

Higher Unit Costs Versus Conventional Devices And Budget Constraints

Safety needles typically carry 20-30% unit premiums versus plain steel, straining procurement in Asia-Pacific and Latin America, where reimbursement growth lags. Reshoring adds immediate cost pressure: ICU Medical paid USD 33.6 million in tariffs during 2025, a sum likely passed through to hospitals. GPO contracts soften premium shock through bulk discounts, but long commitments risk obsolescence if next-gen devices emerge mid-cycle. Low-income immunization programs sometimes default to lowest-bid tenders that lack passive safeguards, undermining the intent of safety policies. Payer formularies echo this austerity: CVS dropped tirzepatide in July 2025, signaling broader resistance to high-priced injectable regimens.

Other drivers and restraints analyzed in the detailed report include:

- Shift To Prefilled Drug-Device Combinations with Embedded Safety

- Innovation In Passive/Auto-Retractable Mechanisms And Low-Dead-Space Designs

- Workflow And Training Gaps With Manual Safety Mechanisms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automatic retractable needles accounted for 53.39% of 2025 revenue, and is expected to grow with 5.23% CAGR through 2031. Hospital GPOs gravitate toward passive models that document lower failure rates and fewer OSHA reportables. Patents held by Retractable Technologies restrict fast-follower designs, compelling challengers to license IP or innovate around it. Manual needles linger in emerging markets where upfront costs dictate choice, but rising GAVI and WHO tenders embed auto-disable criteria that steadily shrink manual needles' share of the retractable needles market.

Supplier consolidation is tightening. MTD Group's August 2024 purchase of Ypsomed's pen-needle business vaulted it to the world's number-two volume slot at 2.5 billion units annually, heightening bargaining power in GPO negotiations. Environmental concerns add a fresh angle: reloadable autoinjectors promise landfill cuts but lack finalized regulatory frameworks, delaying any immediate threat to single-use retractables. Overall, automatic devices will remain the volume and value engine inside the retractable needles market.

Geography Analysis

North America accounted for 45.49% of 2025 global sales as OSHA penalties escalated and GLP-1 approvals drove injection counts. BD's Nebraska expansion, due to go online mid-2026, illustrates the retreat from domestic capacity even as tariffs elevated manufacturing costs. Medicare coverage for anti-obesity drugs and employer uptake will add an estimated 1 billion annual doses by 2030, safeguarding regional growth prospects despite the reimbursement squeeze.

Asia-Pacific will pace the retractable needles market at a 5.12% CAGR to 2031. China and India invest heavily in vaccination drives and medical tourism infrastructure, boosting both institutional and home-care purchases. Chronic disease prevalence skews heavily toward the region, and Embecta's 2026 GLP-1 biosimilar launches are set to capture pent-up demand. Domestic firms such as Nipro, Terumo, and Hindustan Syringes maintain price advantages, although uneven regulatory enforcement permits counterfeit penetration that erodes premium adoption.

Europe straddles opportunity and compliance risk. The EU MDR's protracted certification process threatens temporary shortages when legacy SKUs retire before approvals. Yet, MTD Group's pan-European capacity and Unither's Euroject line anchor a robust supply base. Auto-disable mandates in GAVI-supported Eastern European programs deliver incremental tailwinds. Elsewhere, South America and the Middle East & Africa lag in absolute terms but show policy-driven openings as the WHO procurement specifications require ISO-23908 compliance.

- B. Braun

- Beckton Dickinson

- Biotronix Healthcare Inc.

- Cardinal Health

- DMC Medical Limited

- Henke-Sass, Wolf

- Hindustan Syringes & Medical Devices

- ICU Medical

- MYCO Medical

- Nanchang Kindly

- Nipro

- Numedico Technologies Pty Ltd

- Retractable Technologies

- Roncadelle Operations s.r.l.

- Sol-Millennium Medical Group

- Terumo

- UltiMed, Inc.

- Weigao Group

- Zephyrus Innovations Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Injection Volumes from Chronic Diseases and Mass Immunization Programs

- 4.2.2 Regulatory Mandates and Sharps-Injury Prevention Policies Accelerating Safety Device Adoption

- 4.2.3 Shift To Prefilled Drug-Device Combinations with Embedded Safety

- 4.2.4 Innovation In Passive/Auto-Retractable Mechanisms and Low-Dead-Space Designs

- 4.2.5 Hospital Procurement Via GPOs Favoring Integrated Safety and Bundled Contracts

- 4.2.6 Supply-Chain Localization and Tariff-Driven Reshoring Boosting Safety-Grade Capacity

- 4.3 Market Restraints

- 4.3.1 Higher Unit Costs Vs Conventional Devices and Budget Constraints

- 4.3.2 Workflow/Training Gaps and Activation Failures In Manual Safety Mechanisms

- 4.3.3 Competition From Needle-Free and Alternative Delivery Modalities

- 4.3.4 Regulatory Crackdowns/Recalls Causing Intermittent Supply Disruptions

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value USD)

- 5.1 By Product Type

- 5.1.1 Automatic Retractable Needles

- 5.1.2 Manual Retractable Needles

- 5.2 By Application

- 5.2.1 Subcutaneous Injections

- 5.2.2 Intramuscular Injections

- 5.2.3 Intravenous Injections

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Clinics and Physician Offices

- 5.3.3 Ambulatory Surgical Centers

- 5.3.4 Home Care and Community Health

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of MEA

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 B. Braun Melsungen AG

- 6.3.2 Becton, Dickinson and Company

- 6.3.3 Biotronix Healthcare Inc.

- 6.3.4 Cardinal Health

- 6.3.5 DMC Medical Limited

- 6.3.6 Henke-Sass, Wolf

- 6.3.7 Hindustan Syringes & Medical Devices

- 6.3.8 ICU Medical

- 6.3.9 MYCO Medical

- 6.3.10 Nanchang Kindly

- 6.3.11 Nipro Corporation

- 6.3.12 Numedico Technologies Pty Ltd

- 6.3.13 Retractable Technologies, Inc.

- 6.3.14 Roncadelle Operations s.r.l.

- 6.3.15 Sol-Millennium Medical Group

- 6.3.16 Terumo Corporation

- 6.3.17 UltiMed, Inc.

- 6.3.18 Weigao Group

- 6.3.19 Zephyrus Innovations Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment