PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063508

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063508

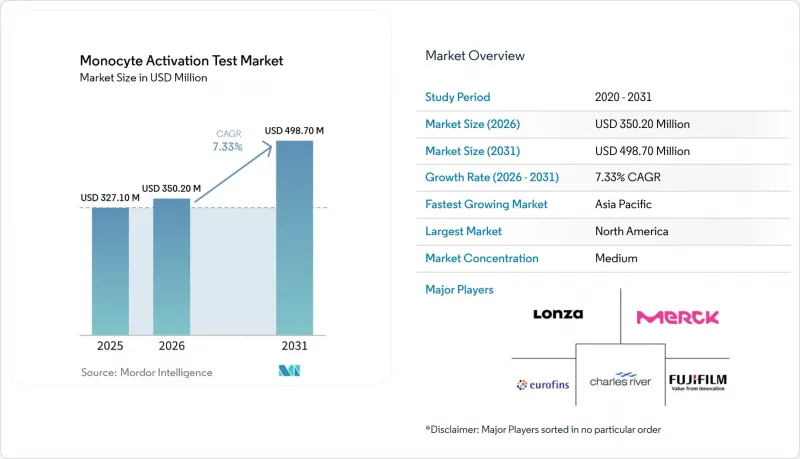

Monocyte Activation Test - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the monocyte activation test market size is expected to grow from USD 327.10 million in 2025 to USD 350.20 million in 2026 and is forecast to reach USD 498.70 million by 2031 at 7.33% CAGR over 2026-2031.

This report is Segmented by Product & Service (Kits and Reagents, and More), Source (PBMC-Based, Cell Line-Based, and More), Readout (ELISA, Flow Cytometry, QPCR/Reporter Gene), Application (Drug Development, Vaccine Development, Medical Devices, Raw Materials), End User (Pharma, Biotech, Device Manufacturers, CROs/CMOs, Academic Institutes), and Geography. Market Forecasts are in Value (USD).

Global Monocyte Activation Test Market Trends and Insights

Regulatory Phase-Out of Rabbit Pyrogen Test in Europe Accelerates MAT Adoption

European Pharmacopoeia suppressed the rabbit pyrogen test from chapter 2.6.8 on 1 January 2026 and deleted it from 57 monographs by July 2025, eliminating the last regulatory fallback that delayed MAT investment. Manufacturers must now conduct non-endotoxin pyrogen risk assessments for every process change, effectively mandating MAT for complex biologics. Middle Eastern and African regulators, mirroring Ph. Eur. standards, are updating national guidelines, expanding the addressable demand. The majority of European parenteral products that were formerly tested on rabbits must convert to MAT by mid-2026, triggering a short-term surge that spills into Latin America and MENA over the medium term.

Expanding Biologics, Cell/Gene-Therapy Pipelines Increase Pyrogen Testing Volumes

Gene-therapy investment reached USD 15.2 billion in 2024, with more than half of new trials outside oncology, bringing lipid nanoparticles, viral capsids, and novel excipients that activate monocytes via TLR-independent pathways . FDA scrutiny of innate immune activation following AAV-related fatalities in 2025 has driven MAT adoption at the preclinical and Phase I stages. mRNA vaccines illustrate the need: their ionizable lipids induce TNF-a and IL-6 that ordinary endotoxin assays miss. Volumes therefore rise beyond batch release into development and validation workflows, particularly in North America and Europe, with Asia-Pacific adding capacity through 2030.

Non-Harmonized Pharmacopeial Acceptance and Product-Specific Validations Slow Global Rollout

USP lacks a dedicated MAT chapter, forcing sponsors to deliver full alternative-method validation under <1225> and product-specific verification, adding 6-12 months and up to USD 0.5 million per product. Japan and Pharmacopoeia Internationalis omit MAT entirely, compelling dual rabbit or endotoxin testing for those markets. Until ICH Q4B expands to MAT, multinational firms weigh the costs of duplication against scientific gains.

Other drivers and restraints analyzed in the detailed report include:

- Ethical / 3Rs Mandates and Corporate Sustainability Policies Favor Animal-Free Testing

- Rapid MAT Formats Reduce Cycle Time and QC Bottlenecks

- Donor/Assay Variability and Inter-Lab Reproducibility Challenges Raise QA Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Kits and reagents led the monocyte activation test market, with a 56.18% share in 2025, and are growing at a 7.65% CAGR. Rapid ELISA and reporter-gene formats underpin demand. Instruments represent a smaller slice because one reader supports multiple assays, yet remain critical for cell-based workflows; vendors such as BMG LABTECH offer multimode readers with 37 °C incubation and 5% CO2 control. Services expand as biotech firms outsource validation; Charles River provides turnkey testing, interference studies, and regulatory consulting, monetizing complexity.

Large biopharma internalizes MAT to cut unit costs, while small sponsors leverage CROs to avoid capital outlay. Service revenues are episodic, tied to product launches and validation cycles, whereas kit sales recur with every batch. Suppliers with integrated portfolios-cells, reagents, reference standards, and protocols-lower adoption barriers and defend margins. Demand for service bundles that include method development and submission support is increasing, creating a two-speed ecosystem within the monocyte activation test market.

PBMC-based methods controlled 43.87% of the monocyte activation test market share in 2025, thanks to pharmacopeial precedent. Cell-line platforms are advancing at a 7.93% CAGR driven by reproducibility advantages. NOMO-1 or THP-1 NF-κB luciferase assays deliver detection limits below 0.013 EU/mL and remove donor-screening costs . Whole-blood formats remain niche for phage therapy and complex matrices because logistics limit scale.

Cell lines appeal to vaccine manufacturers and CDMOs handling high volumes, yet regulators require bridging studies to show parity with PBMC assays. MHRA's 2025 phage-therapy guidance accepted MAT without prescribing cell source, indicating openness to validated alternatives. hiPSC-derived macrophages offer a promising future path for GMP production but await validation. The coexistence of PBMCs and cell lines ensures differentiated options across budgets and risk profiles in the monocyte activation test market.

Geography Analysis

North America commanded 38.39% of revenue in 2025. FDA accepts MAT as an alternative method upon full validation, yet the absence of a compendial chapter raises costs. Lonza's 18,000 sq ft Maryland expansion signals sustained regional demand. Concentrated gene-therapy pipelines and heightened scrutiny after 2025 safety events drive early-stage adoption. Canada and Mexico contribute modestly; Mexico's biosimilar producers implement MAT to meet export standards.

Europe's share benefits from legal certainty: the rabbit test was removed, and non-endotoxin pyrogen risk assessment is mandatory. Germany, the United Kingdom, and France are front-runners thanks to dense biopharma clusters and strong 3Rs culture. EDQM's 2026 symposium provided implementation guidance, smoothing adoption. Southern European uptake lags, but spillover into MENA and Latin America via harmonized standards sustains growth.

Asia-Pacific is the fastest-growing region, with a 7.59% CAGR through 2031. China and India scale cell-therapy and biosimilar plants devoid of rabbit infrastructure, embracing MAT from the outset. Japan's pharmacopoeia gap forces dual testing, muting growth. South Korea leverages its cell-therapy leadership, and Australia's regulators prioritize in vitro methods. Southeast Asia and Taiwan represent emerging adopters as they align with export-market requirements. The Middle East & Africa and South America remain smaller but strategic. GCC health authorities and Brazil's ANVISA align progressively with European standards, opening new markets for kits and validation services.

- Cellular Technology Limited (CTL)

- Charles River

- Eurofins

- FUJIFILM

- Haemochrom Diagnostica GmbH

- Labor LS SE & Co. KG

- Lonza Group Ltd.

- Mabtech

- MAT BioTech B.V.

- MAT Research B.V.

- Merck

- Microcoat Biotechnologie

- Minerva Biolabs GmbH

- Nelson Labs

- PromoCell

- Quality Assistance S.A.

- Sanquin Reagents B.V.

- SGS North America, Inc.

- WuXi App Tec

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Phase-Out Of Rabbit Pyrogen Test (RPT) In Europe Accelerates MAT Adoption

- 4.2.2 Expanding Biologics, Cell/Gene Therapy, And Parenteral Pipelines Increase Pyrogen Testing Volumes

- 4.2.3 Ethical/3Rs Mandates and Corporate Sustainability Policies Favor Animal-Free Testing

- 4.2.4 Rapid MAT Formats (2-8 Hour ELISA/Reporters) Reduce Cycle Time and QC Bottlenecks

- 4.2.5 New EU Ph. Eur. 5.1.13 "Pyrogenicity" And NEP Risk-Assessment Drive MAT Where BET/Rfc Are Insufficient

- 4.2.6 PBMC Supply Scaling and Vendor Partnerships Improve Lot-To-Lot Reproducibility and Global Availability

- 4.3 Market Restraints

- 4.3.1 Non-Harmonized Pharmacopeial Acceptance and Product-Specific Validations Slow Global Rollout

- 4.3.2 Donor/Assay Variability and Inter-Lab Reproducibility Challenges Raise QA/Validation Burden

- 4.3.3 Limited NEP Reference Standards and Control Materials Constrain Robust PSV And Comparability

- 4.3.4 Specialized Equipment/Readouts (ELISA/Reporters) And Trained Staff Needs Elevate Entry Costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product & Service

- 5.1.1 Kits and Reagents

- 5.1.2 Instruments

- 5.1.3 Services (CRO/CTO testing, validation, training)

- 5.2 By Source

- 5.2.1 PBMC-based

- 5.2.2 Cell line-based (e.g., MM6, THP-1, NOMO-1)

- 5.2.3 Whole blood-based

- 5.3 By Detection

- 5.3.1 ELISA-based

- 5.3.2 Flow-cytometry-based

- 5.3.3 qPCR/Reporter gene-based (e.g., NF-κB luciferase, dPCR)

- 5.4 By Application

- 5.4.1 Drug development / batch release

- 5.4.2 Vaccine development and inherently pyrogenic vaccines

- 5.4.3 Medical devices (material-mediated pyrogens)

- 5.4.4 Raw materials / excipients / APIs

- 5.5 By End User

- 5.5.1 Pharmaceutical companies

- 5.5.2 Biotechnology companies

- 5.5.3 Medical device manufacturers

- 5.5.4 CROs/CMOs/CTOs

- 5.5.5 Academic & research institutes

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Cellular Technology Limited (CTL)

- 6.3.2 Charles River Laboratories International, Inc.

- 6.3.3 Eurofins Scientific SE

- 6.3.4 FUJIFILM Holdings Corporation

- 6.3.5 Haemochrom Diagnostica GmbH

- 6.3.6 Labor LS SE & Co. KG

- 6.3.7 Lonza Group Ltd.

- 6.3.8 Mabtech AB

- 6.3.9 MAT BioTech B.V.

- 6.3.10 MAT Research B.V.

- 6.3.11 Merck KGaA

- 6.3.12 Microcoat Biotechnologie GmbH

- 6.3.13 Minerva Biolabs GmbH

- 6.3.14 Nelson Labs

- 6.3.15 PromoCell GmbH

- 6.3.16 Quality Assistance S.A.

- 6.3.17 Sanquin Reagents B.V.

- 6.3.18 SGS North America, Inc.

- 6.3.19 WuXi AppTec

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment