PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063509

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063509

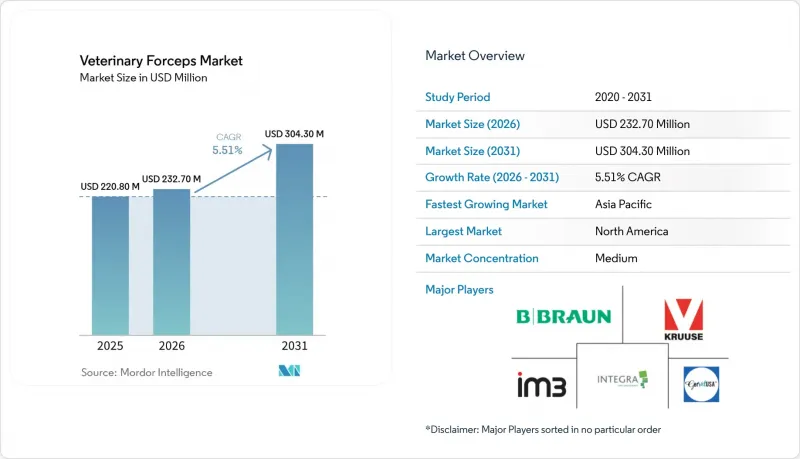

Veterinary Forceps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the veterinary forceps market size is expected to grow from USD 220.80 million in 2025 to USD 232.70 million in 2026 and is forecast to reach USD 304.30 million by 2031 at 5.51% CAGR over 2026-2031.

This report is Segmented by Product Type (Hemostatic/Clamps, Tissue, and More), Application (Dental, Soft Tissue, Orthopedic, Ophthalmic/Neurosurgery, and More), Animal Type (Companion, Equine, Livestock, and More), End User (Clinics, Hospitals/Referral Centers, Research Institutes), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are in Value (USD).

Global Veterinary Forceps Market Trends and Insights

Companion Animal Ownership and Pet-Health Spending Lift Surgical Procedure Volumes

U.S. pet spending climbed to USD 158 billion in 2025, and is projected to reach USD 165 billion in 2026. Rapid insurance uptake lowers cost barriers, prompting owners to approve surgeries that formerly were deferred. Although overall visit counts dipped 3.1% due to staffing shortages, the procedures performed tend to be complex and instrument-intensive, boosting demand for high-margin specialty forceps. Emergency visits rose to 22% of owners in 2025, concentrating surgical volumes at referral hospitals that maintain deeper inventories and tighter replacement cycles. Suppliers that certify traceability and provide quick-turn servicing strengthen their position with these hospitals.

High-Volume Spay/Neuter Programs and Post-Pandemic Surgical Backlog Sustain Instrument Demand

High-volume clinics, typified by PAWS Chicago's target of 20,000 spay-neuter surgeries in 2025, are addressing a backlog of 261,763 missed procedures accumulated during 2020-2023 lockdowns. Rising throughput favors pre-sterilized or single-use hemostats that bypass autoclave bottlenecks. Yet persistent workforce gaps cap expansion speed, forcing tray standardization and bulk purchasing to curb turnaround delays. Vendors offering kitted solutions and competitive per-procedure economics gain preferred-vendor status.

High Instrument and Sterilization Costs Constrain Clinic CAPEX

Fixed facility start-ups require USD 433,000-2 million, with roughly USD 70,000 earmarked for surgical and dental gear, leaving little headroom for premium forceps. Working-capital constraints and higher 2025 interest rates prompted many independents to stretch replacement cycles through repair services. Equipment financing demands credit scores above 640 and exposes clinics to rate resets, prompting deferral of non-essential upgrades. Suppliers offering repair kits, sharpening programs, and trade-in rebates can ease budgetary friction.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Veterinary Dental Care Elevates Demand for Extraction and Tissue Forceps

- Growth of Minimally Invasive and Specialty Procedures Expands Forceps Use-Cases

- Shortage of Skilled Veterinary Surgeons Limits Surgical Throughput

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hemostatic and clamp forceps captured 26.10% veterinary forceps market share in 2025, anchored by universal use across soft-tissue, orthopedic, and emergency trays. Dental extraction forceps are on track for a 6.09% CAGR to 2031, expanding 58 basis points faster than the overall veterinary forceps market. Growth stems from general-practice adoption of dental suites and rising owner awareness of periodontal disease. Tissue, dressing, and orthopedic forceps fill mature niches where sales hinge on replacement rather than first-time installs. Ophthalmic and endoscopic biopsies remain small but price-dense due to precision machining and microtip finishing. GerVetUSA's titanium dental kits and B. Braun's BipoJet bipolar clamps exemplify performance-driven innovations commanding price premiums .

Continued investments in operator ergonomics, such as winged elevators and articulating handles, improve grip security and reduce surgeon fatigue, reinforcing repeat purchasing. The demand for veterinary surgical forceps is expected to surge. Manufacturers pairing extraction forceps with luxating elevators and periosteal lifters deepen lock-in among clinics upgrading entire dental sets at once.

Soft-tissue procedures held 34.87% of revenue in 2025, led by spay-neuter, mass removal, and abdominal surgery, yet orthopedic cases are slated for a 5.98% CAGR through 2031, outrunning the veterinary forceps market by 47 basis points. Locking-plate systems that outperform pin-and-wire constructs require specialized reduction grips and bone-holding clamps, pushing per-case instrument outlays higher. As insurers reimburse fracture repair more readily, clinics increase stock of rongeurs, bone plates, and reduction forceps, driving a larger share of the veterinary forceps market size into orthopedic SKUs. Endoscopic neurosurgery and ophthalmic specialties extend portfolio depth at referral hospitals, although volumes remain comparatively modest.

Technological spillover from human orthopedics, such as 3D-printed patient-specific guides, further differentiates forceps offerings. High upfront capital impedes adoption by general practices, but teaching hospitals and corporate referral centers are piloting these systems, reinforcing demand for compatible graspers and reduction clamps. Suppliers that bundle power tools with matching forceps under service contracts gain cross-selling synergy.

Geography Analysis

North America retained a 43.81% share in 2025, driven by USD 157 billion in U.S. pet spending and a dense network of Mars Petcare facilities. Pet insurance penetration of 6.4 million policies lowers decision friction for elective surgery, though clinic staffing shortages capped 2025 visit growth. Tariffs of up to 54% on Chinese forceps elevated landed costs, prompting suppliers to near-shore production or blend recycled titanium to maintain margins.

Asia-Pacific is forecast to advance at a 5.97% CAGR through 2031, driven by China's urban pet boom and India's National Animal Disease Control Programme, which underwrites large-scale surgical interventions in livestock. Regulatory clarification by India's CDSCO in July 2025 eased device imports, inviting foreign brands to tap the veterinary forceps market. Japan and South Korea add premium tailwinds via tech-enabled clinics and willingness to adopt minimally invasive procedures.

Europe presents a fragmented regulatory patchwork; only six member states directly regulate veterinary devices, complicating rollout. Dual-use instruments must comply with MDR 2017/745, thereby inflating compliance costs. Upcoming EU GMP rules effective July 2026 tighten aseptic manufacturing requirements, indirectly raising the bar for forceps sterilization validation. South America and MEA remain smaller but rising; Brazil benefits from increasing companion-animal ownership, while GCC states boost livestock health budgets, together nudging incremental demand for mid-tier forceps lines.

- Avante Health Solutions

- B. Braun

- Covetrus

- Dentalaire

- Dispomed

- Eickemeyer Veterinary Equipment

- Fine Science Tools (FST)

- GerVetUSA

- gSource

- Harvard Apparatus

- iM3

- Integra LifeSciences

- Jorgensen Laboratories

- Karl Storz

- Kent Scientific

- KRUUSE

- Movora

- Orthomed

- Roboz Surgical

- Sklar Surgical Instruments

- World Precision Instruments (WPI)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Companion Animal Ownership and Pet-Health Spending Lift Surgical Procedure Volumes

- 4.2.2 High-Volume Spay/Neuter Programs and Post-Pandemic Surgical Backlog Sustain Instrument Demand

- 4.2.3 Expansion Of Veterinary Dental Care Elevates Demand for Extraction and Tissue Forceps

- 4.2.4 Growth Of Minimally Invasive and Specialty Procedures Expands Forceps Use-Cases

- 4.2.5 Procurement Standardization by Corporate Consolidators Accelerates SKU Adoption/Replacement

- 4.2.6 Infection-Control Focus Raises Demand for Sterile Single-Use and Reprocessing-Traceable Forceps

- 4.3 Market Restraints

- 4.3.1 High Instrument/Sterilization Costs and Constrained Clinic Capex

- 4.3.2 Shortage Of Skilled Veterinary Surgeons Limits Surgical Throughput

- 4.3.3 Input/Tariff Volatility for Surgical-Grade Steel/Titanium Pressures, Prices, And Margins

- 4.3.4 Research 3Rs And Activism Reduce Lab-Animal Surgical Volumes for Micro-Forceps

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Hemostatic/Clamps

- 5.1.2 Tissue

- 5.1.3 Dressing/Sponge

- 5.1.4 Dental Extraction

- 5.1.5 Orthopedic

- 5.1.6 Ophthalmic

- 5.1.7 Endoscopic & Biopsy

- 5.2 By Application

- 5.2.1 Dental Surgery

- 5.2.2 Soft Tissue Surgery

- 5.2.3 Orthopedic Surgery

- 5.2.4 Ophthalmic/Neurosurgery

- 5.2.5 Other Applications

- 5.3 By Animal Type

- 5.3.1 Companion Animals

- 5.3.2 Equine

- 5.3.3 Livestock

- 5.3.4 Other Animal Types

- 5.4 By End User

- 5.4.1 Veterinary Clinics

- 5.4.2 Veterinary Hospitals/Referral & Teaching Centers

- 5.4.3 Research Institutes & Academic Labs

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Avante Animal Health

- 6.3.2 B. Braun

- 6.3.3 Covetrus

- 6.3.4 Dentalaire

- 6.3.5 Dispomed

- 6.3.6 Eickemeyer

- 6.3.7 Fine Science Tools (FST)

- 6.3.8 GerVetUSA

- 6.3.9 gSource

- 6.3.10 Harvard Apparatus

- 6.3.11 iM3

- 6.3.12 Integra LifeSciences

- 6.3.13 Jorgensen Laboratories

- 6.3.14 KARL STORZ

- 6.3.15 Kent Scientific

- 6.3.16 KRUUSE

- 6.3.17 Movora

- 6.3.18 Orthomed

- 6.3.19 Roboz Surgical

- 6.3.20 Sklar Surgical Instruments

- 6.3.21 World Precision Instruments (WPI)

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment