PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063510

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063510

Tissue Processing Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

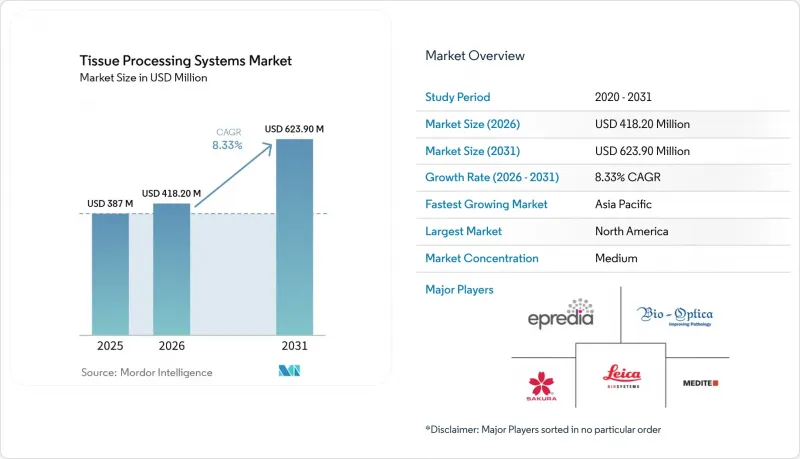

According to Mordor Intelligence, the tissue processing systems market size is expected to increase from USD 387 million in 2025 to USD 418.20 million in 2026 and reach USD 623.90 million by 2031, growing at a CAGR of 8.33% over 2026-2031.

This report is Segmented by Technology (Vacuum/Retort Tissue Processors and More), Product (Fully Automated, Semi-Automated, Manual), Modality (Stand-alone/Floor-standing, Bench-Top), End User (Hospitals, Research & Academic Institutes, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Tissue Processing Systems Market Trends and Insights

Rising Cancer and Chronic Disease Burden Elevates Biopsy Volumes and Histology Workloads

The Global Burden of Disease Study estimated worldwide cancer incidence at 18.5 million cases in 2023 and projects a 65% increase to 30.5 million by 2050, thereby directly increasing cassette throughput in pathology laboratories . Precision oncology protocols now demand three to five blocks per patient for biomarker panels such as PD-L1 or HER2, tripling work per case compared with hematoxylin-and-eosin-only routines. China's clinical-trial ecosystem logged a 22% annual rise in oncology studies in 2024, with each trial generating 50-200 biopsies, prompting Beijing and Shanghai centers to install dual-retort processors that handle 300-400 cassettes per eight-hour shift. Across OECD markets, people older than 65 will account for 25% of the population by 2030, and this cohort already represents 60% of cancer diagnoses, stretching histology capacity. Serial-biopsy monitoring of inflammatory bowel and autoimmune liver disease added 12 million cases in 2025, raising utilization above 85% at many labs.

Push for Lab Automation and LIS/Digital Integration to Lift Throughput and Quality in Core Histology

Modern laboratory information systems orchestrate end-to-end specimen flow. Tissue processors now stream real-time temperature and reagent-consumption data via HL7 FHIR, feeding dashboards that predict maintenance windows and prompt just-in-time reagent restocks. In 2025, Agilent bundled its processors with digital pathology partners, cutting ID errors by 40% at Mayo Clinic's two-million-slide operation. CMS order QSO-25-10 enforces electronic audit trails, obliging any Medicare-billing lab to retire isolated manual processors that lack connectivity. FlexLIS, launched in 2025, reroutes cassettes to under-used instruments and flags anomalies before embedding, slashing overall turnaround 30% at pilot sites.

High Capital and Lifecycle Costs Constrain Adoption

A modern dual-retort processor lists at USD 150,000-250,000, and annual service can add 15% of that figure. Medium-sized community hospitals face a 3- to 5-year payback period, while reimbursement for histopathology has remained flat since 2020. Refurbished units cut upfront costs but increase downtime risk because parts for seven-year-old platforms may take 6 weeks to source, an unacceptable delay for single-processor sites. Reagent lock-in deepens the bill: xylene-free chemistries from leading vendors cost 25% more than bulk xylene and cannot be cross-used on rival machines, removing competitive-bidding leverage. The NHS in Wales excluded processors from a GBP 34.4 million managed-service package in 2025, precisely to avoid volatile reagent escalations.

Other drivers and restraints analyzed in the detailed report include:

- Faster Turnaround Time Mandates Accelerate Rapid or Microwave Processor Adoption

- Shift to Xylene-Free or Formalin-Reduced Workflows to Meet Occupational-Health and Sustainability Targets

- Shortage of Skilled Histotechnologists Limits Complex Protocol Uptake

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vacuum or retort processors delivered 55.80% of 2025 revenue, anchored by proven parity with xylene methods and overnight reliability. The tissue processing systems market size for this segment is advancing at a steady pace as refurb units cascade into smaller hospitals. Microwave systems are tracking an 8.87% CAGR because emergency departments want same-day answers and academic centers build rapid suites to cut frozen-section backlogs. Validation research confirmed 95% biomarker integrity after microwave cycles, easing earlier doubts about epitope loss.

Continuous-flow dual-retort architectures help vacuum systems stay relevant by shaving queue times and automating reagent swaps. Milestone's EVO platform processes 400 cassettes per shift and supports xylene-free chemistries, narrowing the functional gap with microwave alternatives. Sakura's VIP 6 AI adds viscosity monitoring, cutting reprocess rates by significantly. With histotechnologist overtime surpassing USD 50 per hour in many U.S. markets, the capital premium for microwave units can be offset within two years through labor savings.

Fully automated processors captured 53.80% of 2025 sales. The tissue processing systems market share advantage stems from integrated barcode tracking, predictive maintenance, and cloud dashboards that enable a single technologist to supervise multiple runs. CMS order QSO-25-10 accelerates that shift by forcing audit-trail capability for Medicare labs. Semi-automated units retain a foothold among mid-tier hospitals yet face erosion as secondary-market automated systems hit similar price points. Manual devices linger in veterinary and small research labs.

Epredia's E1000 Dx processes 1,500 samples a day and uses RFID-based reagent management that automatically orders supplies when a 2-day supply is available, smoothing cash flow for high-volume reference labs. In Asia-Pacific, hospital chains equipping for medical-tourism accreditation install fully automated lines to satisfy College of American Pathologists benchmarks, helping the region outpace global growth. Robotic loaders, such as Sakura's SmartConnect, reduce manual handling by 80%, which is vital in geographies with 20% vacancy rates.

Geography Analysis

North America accounted for 38.19% of the 2025 value, with the United States accounting for nearly four-fifths. The region's consolidation wave, typified by Labcorp's May 2025 acquisition of Incyte diagnostics assets, is harmonizing protocols and negotiating reagent bulk discounts. CMS CLIA order QSO-25-10 forces full digital traceability, vaulting automation investment ahead of simple capacity gains. Leica partnered with Histofy in 2025 to embed predictive QC into HistoCore PEGASUS Plus, showing the region's appetite for AI-driven analytics. Canada and Mexico lag because of lower per-capita spend and limited adoption outside academic centers. Persistent 15-20% technologist vacancies keep automation on the front burner.

Asia-Pacific is forecast to post an 8.59% CAGR to 2031, outpacing all other regions. China leads due to a 22% annual rise in oncology trials that demand high-throughput dual-retort systems. India's private hospital chains install automated lines to attract international patients and secure College of American Pathologists stamps, yet staffing shortfalls slow protocol validation. Japan's over-65 share will hit 35% by 2030, spurring demand, though reimbursement caps temper capital budgets. Australia and South Korea act as early adopters of xylene-free chemistries because procurement frameworks award 15% weight to environmental criteria.

Europe holds a diversified mid-tier position. The U.K. NHS Anatomical Pathology Automation framework, worth GBP 40 million over eight years, anchors large upgrades across England and Wales. Germany and France follow with university hospital investments, while Eastern Europe sees fresh capacity, as in MedLife's USD 2.1 million automated lab opened in Romania in 2025. The Middle East and Africa cluster around centers of excellence such as Saudi Arabia's King Faisal Specialist Hospital, which unveiled a USD 50 million AI-enabled lab in 2024. South America remains nascent; Brazilian and Argentine labs rarely surpass 5,000 cassettes a year, limiting automation ROI, though donor-funded projects in Ethiopia and the Gulf Cooperation Council bring select modern units to public labs.

- Amos Scientific Pty Ltd

- Bioevopeak

- Bio-Optica Milano S.p.A.

- Dakewe Medical

- Diapath S.p.A.

- Epredia (PHC Holdings)

- General Data Healthcare (RTP Series)

- Histo-Line Laboratories

- Infitek Co., Ltd.

- Jinhua YIDI Medical Appliance

- JOKOH Co., Ltd.

- Kalstein

- Leica Biosystems (Danaher)

- MEDITE Medical GmbH

- Milestone Medical

- PathnSitu Biotechnologies

- Sakura Finetek USA, Inc

- Servicebio (Wuhan Servicebio Technology)

- Shenyang Roundfin Technology (Roundfin)

- SLEE medical GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Cancer and Chronic Disease Burden Elevates Biopsy Volumes and Histology Workloads

- 4.2.2 Push For Lab Automation And LIS/Digital Integration to Lift Throughput and Quality in Core Histology

- 4.2.3 Faster Turnaround Time Mandates (STAT/Same-Day) Accelerate Rapid/Microwave Processor Adoption

- 4.2.4 Shift To Xylene-Free/Formalin-Reduced Workflows to Meet OH&S And Sustainability Targets

- 4.2.5 Dual-Retort/Parallel Processing Architectures Enable Lean, Continuous-Flow High-Mix Labs

- 4.2.6 Consolidation Of Multi-Site Networks and Tenders Standardizes Installed Bases to A Few Platforms

- 4.3 Market Restraints

- 4.3.1 High Capital and Lifecycle Costs (Service, Reagents, Downtime Risk) Constrain Adoption

- 4.3.2 Shortage of Skilled Histotechnologists Limits Complex Protocol Utilization at Scale

- 4.3.3 Regulatory and Chemical-Safety Compliance Adds Validation/Documentation Burden

- 4.3.4 Protocol Validation Hurdles for Rapid/Microwave on Sensitive Tissues/Biomarkers

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Technology

- 5.1.1 Vacuum/Retort Tissue Processors

- 5.1.2 Microwave/Rapid Tissue Processors

- 5.1.3 Other

- 5.2 By Product

- 5.2.1 Fully Automated

- 5.2.2 Semi-automated

- 5.2.3 Manual

- 5.3 By Modality

- 5.3.1 Stand-alone / Floor-standing

- 5.3.2 Bench-top

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Diagnostic Laboratories

- 5.4.3 Research & Academic Institutes

- 5.4.4 Pharma/Biotech & CRO

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Amos Scientific Pty Ltd

- 6.3.2 Bioevopeak

- 6.3.3 Bio-Optica Milano S.p.A.

- 6.3.4 Dakewe Medical

- 6.3.5 Diapath S.p.A.

- 6.3.6 Epredia (PHC Holdings)

- 6.3.7 General Data Healthcare (RTP Series)

- 6.3.8 Histo-Line Laboratories

- 6.3.9 Infitek Co., Ltd.

- 6.3.10 Jinhua YIDI Medical Appliance

- 6.3.11 JOKOH Co., Ltd.

- 6.3.12 Kalstein

- 6.3.13 Leica Biosystems (Danaher)

- 6.3.14 MEDITE Medical GmbH

- 6.3.15 Milestone Medical

- 6.3.16 PathnSitu Biotechnologies

- 6.3.17 Sakura Finetek USA, Inc

- 6.3.18 Servicebio (Wuhan Servicebio Technology)

- 6.3.19 Shenyang Roundfin Technology (Roundfin)

- 6.3.20 SLEE medical GmbH

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment