PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063511

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063511

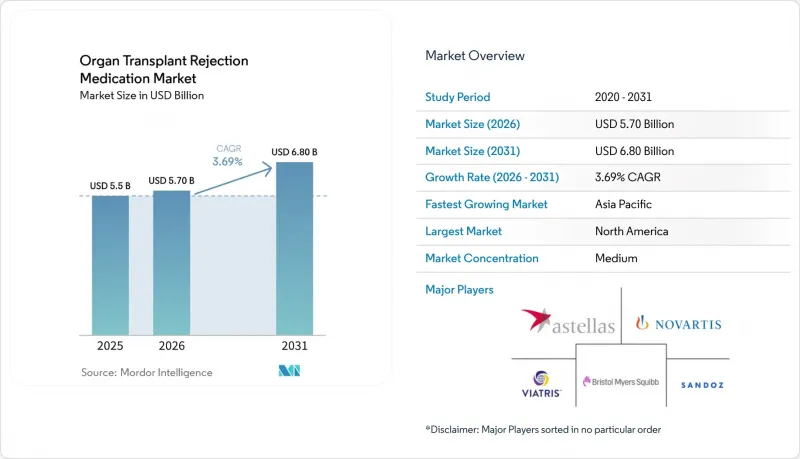

Organ Transplant Rejection Medication - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the organ transplant rejection medication market size was valued at USD 5.5 billion in 2025 and is estimated to grow from USD 5.70 billion in 2026 to reach USD 6.80 billion by 2031, at a CAGR of 3.69% during the forecast period (2026-2031).

This report is Segmented by Drug Class (Calcineurin Inhibitors, Antiproliferatives, and More), Transplant Type (Kidney, Liver, Heart, and More), Molecule Type (Small Molecules, Biologics), Distribution Channel (Transplant Centers, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Organ Transplant Rejection Medication Market Trends and Insights

Rising Transplant Volumes Anchor Chronic Immunosuppression Demand

Kidney transplantation accounted for a significant share of 2025 revenue and continues to outpace the liver and heart segments, as 27,573 kidney procedures were performed in the United States in 2025 and 22,814 in China in 2023. Medicare's coverage reforms eliminated the 36-month payment cliff, cutting non-adherence-driven graft loss by roughly 15% and expanding the treated population. India's National Organ and Tissue Transplant Organization reports 15,000-20,000 annual kidney transplants, underscoring Asia-Pacific's pivotal role in the organ transplant rejection medication market. Japan remains supply-constrained with only about 2,000 kidney transplants per year because its deceased-donor rate is just 1.7 per million people. Volume growth thus delivers the single-largest positive increment to CAGR forecasts through 2031.

Tacrolimus-Based CNI Regimens Remain the Global Workhorse

Calcineurin inhibitors held a significant share in 2025, with tacrolimus accounting for the majority of CNI prescriptions. Although generic penetration surged significantly, the FDA's 2023 downgrade of one tacrolimus generic from AB to BX slowed new substitutions, prompting most U.S. programs to sign single-source agreements to avoid formulation variability. Extended-release tacrolimus, marketed as Envarsus XR, offers higher bioavailability and once-daily dosing, yet payer reluctance toward its price premium limits broad adoption. This mixed pricing-and-volume strategy contributes to the market's growing CAGR.

Price Erosion Compresses Per-Patient Revenue

Generics seized the majority of the mycophenolate segment by 2025, while tacrolimus prices fell significantly since patent expiry, cutting Roche's CellCept sales from USD 2.4 billion in 2010 to roughly USD 350 million in 2026 . Similar patterns afflict sirolimus and everolimus following multiple generic launches. Although single-source contracts curb interchangeability, they also lock in discounted rates, amplifying the negative CAGR contribution.

Other drivers and restraints analyzed in the detailed report include:

- North American Coverage Keeps Adherence High

- Extended-Release Tacrolimus Boosts Adherence, Faces Cost Barriers

- Infection and Malignancy Concerns Drive Minimization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

CNIs accounted for 41.68% of 2025 revenue in the organ transplant rejection medication market, yet widespread generic availability slashed per-unit revenue. Meanwhile, mTOR inhibitors are forecast to rise at 3.98% annually as physicians pair sirolimus or everolimus with reduced-dose tacrolimus to mitigate nephrotoxicity. Triple-therapy protocols involving antiproliferatives such as mycophenolate still account for a notable share of market revenue, highlighting the entrenched nature of clinical practice. Co-stimulation blockade and IL-2 receptor antagonists together hold a modest share, largely driven by belatacept's significant year-over-year gains.

Kidney transplants accounted for 48.19% of 2025 revenue and are projected to grow at a 4.05% CAGR through 2031, outpacing the liver and heart segments. Medicare's coverage extension and sizable living-donor programs in India reinforce this trajectory. Liver transplantation, roughly ntable share of the 2025 value, benefits from rising non-alcoholic steatohepatitis prevalence but faces marginally lower immunosuppression intensity. Heart and lung segments account for a combined modest share but command higher per-patient spending due to stringent rejection prophylaxis.

By maintaining volume leadership, kidney transplantation will keep the organ transplant rejection medication market anchored in regions where deceased-donor systems are robust or living-donor programs expand. Novel tolerance-induction regimens under study may eventually rebalance segment weightings past 2030.

Geography Analysis

North America held 43.19% of 2025 revenue, underpinned by Medicare's policy change that permanently funds immunosuppressants for kidney recipients, a reform that slashed graft failure due to non-adherence by 15%. CVS Specialty, Accredo, and Walgreens Specialty manage the majority of high-cost biologic dispensing, linking reimbursement to monitoring adherence metrics. Specialty-pharmacy growth thus parallels biologic uptake, further entrenching payer oversight.

Europe contributed a significant share of global sales, leveraging coordinated procurement through Eurotransplant and Scandiatransplant. However, high generic penetration for tacrolimus and mycophenolate mofetil unit prices are below North American levels. EMA's 2025 biosimilar guidance for monoclonal antibodies still excludes rATG, allowing incumbent brands to defend price points on induction agents.

Asia-Pacific is the fastest-growing geography, expanding at 3.91% annually through 2031. China conducted 22,814 kidney transplants in 2023, and India performs up to 20,000 each year, yet Japan's low deceased-donor rate constrains its share of the market. Regulatory heterogeneity and aggressive local generic manufacturers temper per-patient revenue, but absolute volume gains will raise the baseline for the organ transplant rejection medication market across the region.

- Accord Healthcare

- Asahi Kasei

- Astellas Pharma

- Aurobindo Pharma

- Bristol-Myers Squibb

- Cipla

- CSL Behring

- Dr. Reddy's Laboratories

- Roche

- Fresenius

- Grifols

- Novartis

- Octapharma

- Pfizer

- Sandoz Group

- Sanofi

- Takeda Pharmaceuticals

- Teva Pharmaceutical Industries

- Viatris

- Zydus Lifesciences

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Transplant Volumes; Kidney Accounts for the Majority of Solid Organ Procedures

- 4.2.2 Tacrolimus-Based CNI Regimens Remain the Maintenance Backbone Across Sots

- 4.2.3 North America Leads Revenue Share; Coverage Expansions Sustain Chronic Therapy Adherence

- 4.2.4 Oral Maintenance Dominance; Hospital/Specialty Channels Anchor Dispensing

- 4.2.5 Extended-Release Tacrolimus Adoption Improves Exposure Stability and Adherence

- 4.2.6 AMR Management Intensifies Use of IVIG And Complement-Targeted Adjuncts

- 4.3 Market Restraints

- 4.3.1 Price Erosion from Widespread Generics Across Tacrolimus/MMF/Sirolimus

- 4.3.2 Infection, Malignancy, and Metabolic Risks Drive Minimization and Regimen Switches

- 4.3.3 Regulatory/Quality Frictions (E.G., TE-Rating Changes) Slow Generic Substitution in Some Markets

- 4.3.4 IV Infusion Logistics And EBV-Serostatus Limits Cap Uptake of Certain Biologics

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Drug Class / Mechanism

- 5.1.1 Calcineurin inhibitors (tacrolimus, cyclosporine)

- 5.1.2 Antiproliferatives (mycophenolate mofetil, mycophenolic acid, azathioprine)

- 5.1.3 mTOR inhibitors (sirolimus, everolimus)

- 5.1.4 Corticosteroids

- 5.1.5 Co-stimulation blockers / IL-2R antagonists (belatacept, basiliximab)

- 5.1.6 Lymphocyte-depleting antibodies (rATG/ATG-F, alemtuzumab where used)

- 5.1.7 IVIG/plasmapheresis adjuncts

- 5.2 By Transplant Type

- 5.2.1 Kidney

- 5.2.2 Liver

- 5.2.3 Heart

- 5.2.4 Lung

- 5.2.5 Pancreas

- 5.2.6 Hematopoietic stem cell (HSCT)

- 5.3 By Molecule Type

- 5.3.1 Small molecules

- 5.3.2 Biologics

- 5.4 By Distribution Channel

- 5.4.1 Transplant centers / hospital pharmacies

- 5.4.2 Specialty pharmacies

- 5.4.3 Retail / online pharmacies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Accord Healthcare

- 6.3.2 Asahi Kasei

- 6.3.3 Astellas Pharma

- 6.3.4 Aurobindo Pharma

- 6.3.5 Bristol Myers Squibb

- 6.3.6 Cipla

- 6.3.7 CSL Behring

- 6.3.8 Dr. Reddy's Laboratories

- 6.3.9 F. Hoffmann-La Roche

- 6.3.10 Fresenius Kabi

- 6.3.11 Grifols

- 6.3.12 Novartis AG

- 6.3.13 Octapharma

- 6.3.14 Pfizer

- 6.3.15 Sandoz

- 6.3.16 Sanofi

- 6.3.17 Takeda

- 6.3.18 Teva Pharmaceutical Industries

- 6.3.19 Viatris

- 6.3.20 Zydus Lifesciences

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment