PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063517

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063517

Dental Lights - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

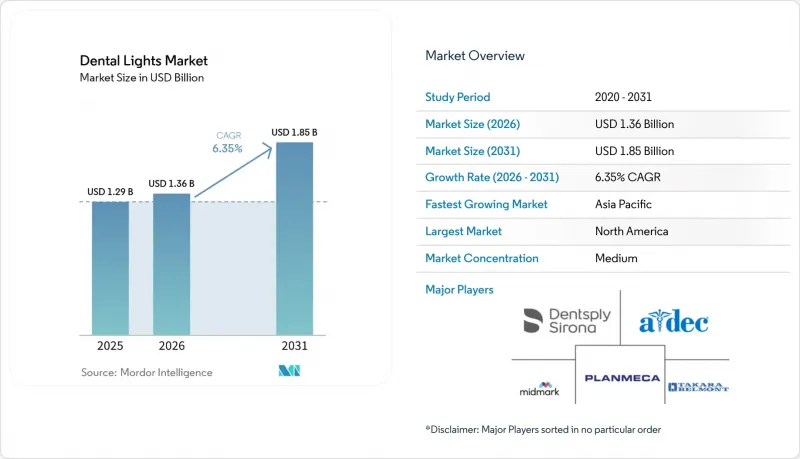

According to Mordor Intelligence, the dental lights market size was valued at USD 1.29 billion in 2025 and is estimated to grow from USD 1.36 billion in 2026 to reach USD 1.85 billion by 2031, at a CAGR of 6.35% during the forecast period (2026-2031).

This report is Segmented by Technology (LED, Halogen, Xenon), Mounting Type (Ceiling-Mounted, Chair-/Unit-mounted, Wall-Mounted, Mobile/Portable), End User (Dental Clinics and DSOs, Hospitals, Academic & Research Institutes, Dental Laboratories), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Dental Lights Market Trends and Insights

LED Transition for Efficiency, Longevity, and Heat Reduction

LED operatory lamps cut energy use by up to 80% and last 15,000-50,000 hours versus halogen's 500-2,000-hour bulbs, eliminating frequent replacements and the associated labor burden. They also generate minimal radiant heat, improving patient comfort and letting sealed housings withstand aggressive disinfectants. Despite those advantages, practitioners who perform complex shade-matching still migrate slowly because only premium multi-wavelength arrays reach CRI 95 or higher, a benchmark halogen meets with ease. The American Dental Association reported that LED multi-wave light-curing units already represented a significant portion of units in clinical use, underscoring momentum behind the solid-state shift.

Infection-Control and Touchless Operatory Workflows

The pandemic cemented touchless activation as a new normal. Motion or proximity sensors now accompany most mid- and high-tier lights, minimizing cross-contamination risk and satisfying stricter hygiene protocols in DSO networks. These features pair naturally with connected ecosystems that log usage hours and automate maintenance reminders. A related occupational-health question has emerged: a 2026 Nature study found that 22.4% of dentists exhibit vision issues linked to prolonged blue-light exposure, roughly double the rate of non-dentists. If regulators translate such findings into tougher blue-hazard limits than ISO 9680:2021's current illuminance threshold, vendors will need adaptive dimming or spectral-filtering upgrades.

Upfront Cost Pressure for Small Practices

Integrated LED packages cost USD 7,000-15,000. Although 80% of practices rely on financing, credit access remains uneven and monthly payments compete directly with staff and consumables budgets. Refurbished halogen units therefore stay attractive, particularly in clinics serving lower-income populations or rural catchments.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of DSOs and Multi-Operatory Buildouts

- Regulatory/Ecodesign Shifts Accelerating LED Retrofits

- Compliance Burden Under ISO 9680:2021 and MDR

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

LED products commanded 61.90% Dental lights market share in 2025, yet halogen posts an 8.10% CAGR. Halogen remains indispensable for specialist clinics where CRI 95-plus color fidelity is non-negotiable. Premium LEDs with multi-wavelength chips are closing the gap, but their price premium sustains a dual-technology landscape. The Dental lights market size for LED platforms will keep expanding, but a loyal halogen customer base guarantees parallel demand through at least 2031.

Second-generation LEDs win favor with DSOs due to 80% lower energy consumption and 15,000-50,000-hour lifespans. Manufacturers reinforce that advantage by bundling lights with imaging and power modules, locking customers into proprietary ecosystems. Meanwhile, xenon stays peripheral, confined to surgical suites that prioritize instant-on brightness over maintenance convenience.

Geography Analysis

North America generated 42.10% of global revenue in 2025, fueled by DSO expansion and a high density of cosmetic procedures that demand advanced lighting. Nevertheless, replacement cycles lengthen as early adopters reach saturation, tempering regional growth below the global CAGR.

Asia-Pacific is the fastest-growing zone at 8.13% per year. China mandates that the majority of dental chairs be locally made by 2026, driving domestic lamp manufacturing and import partnerships. India's 2026 National Dental Commission seeks to close severe care gaps-fewer than one in four primary health centers employ a dentist-thereby lifting demand for portable units and entry-level LED kits. Japan's aging society and Australia's budding DSO sector add premium demand layers, while Southeast Asia adopts a mixed value-premium profile.

Europe exhibits moderate growth underpinned by strict compliance. Northern and Western countries upgrade to tunable LED systems, whereas Southern Europe leans on entry-level LEDs and refurbished halogen models to control costs. The Middle East invests in dental-tourism hubs equipped with high-CRI ceiling lights, and Africa sees sporadic but rising outreach and university purchases. South America's demand concentrates in Brazil and Argentina, where currency swings complicate import affordability yet urban cosmetic practices mirror global LED preferences.

- A-dec Inc.

- BPR Swiss

- DARAY Ltd

- DCI Edge

- DentalEZ

- Dentsply Sirona

- Dr. Mach GmbH & Co. KG

- D-TEC AB

- EKLER

- FARO S.p.A.

- Flight Dental Systems

- Midmark

- Planmeca

- Takara Belmont

- TPC Advanced Technology, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 LED Transition for Efficiency, Longevity, And Heat Reduction

- 4.2.2 Infection-Control and Touchless Operatory Workflows

- 4.2.3 Expansion Of DSOs and Multi-Operatory Buildouts

- 4.2.4 Rising Cosmetic and Restorative Procedure Volumes

- 4.2.5 Regulatory/Ecodesign Shifts Accelerating LED Retrofits

- 4.2.6 Digital Imaging Integration and Tunable CCT/CRI Features

- 4.3 Market Restraints

- 4.3.1 Upfront Cost Pressure for Small Practices

- 4.3.2 Compliance Burden Under ISO 9680:2021 And MDR

- 4.3.3 LED/Optics Component Supply Variability

- 4.3.4 Retrofit Constraints in Low-Ceiling/Legacy Operatory Rooms

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Technology (Light Source)

- 5.1.1 LED

- 5.1.2 Halogen

- 5.1.3 Xenon (niche)

- 5.2 By Mounting Type

- 5.2.1 Ceiling-mounted

- 5.2.2 Chair-/Unit-mounted

- 5.2.3 Wall-mounted

- 5.2.4 Mobile/Portable

- 5.3 By End User

- 5.3.1 Dental Clinics and DSOs

- 5.3.2 Hospitals

- 5.3.3 Academic & Research Institutes

- 5.3.4 Dental Laboratories

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 A-dec Inc.

- 6.3.2 BPR Swiss

- 6.3.3 DARAY Ltd

- 6.3.4 DCI Edge

- 6.3.5 DentalEZ

- 6.3.6 Dentsply Sirona Inc.

- 6.3.7 Dr. Mach GmbH & Co. KG

- 6.3.8 D-TEC AB

- 6.3.9 EKLER

- 6.3.10 FARO S.p.A.

- 6.3.11 Flight Dental Systems

- 6.3.12 Midmark Corporation

- 6.3.13 Planmeca Oy

- 6.3.14 Takara Belmont Corporation

- 6.3.15 TPC Advanced Technology, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment