PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063519

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063519

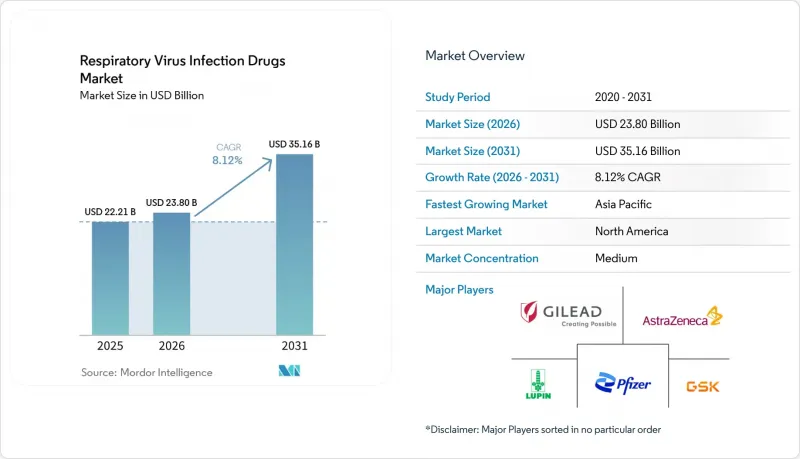

Respiratory Virus Infection Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the respiratory virus infection drugs market size is projected to be USD 22.21 billion in 2025, USD 23.80 billion in 2026, and reach USD 35.16 billion by 2031, growing at a CAGR of 8.12% from 2026 to 2031.

This report is Segmented by Pathogen (SARS-CoV-2, Influenza A/B, RSV, HMPV, and More), Modality (Small-Molecule Antivirals, Monoclonal Antibodies, and More), Route of Administration (Oral, IV, IM/SC, Inhaled), Setting of Care (Outpatient, Hospital, Long-Term Care), and Geography (North America, South America, Europe, APAC, MEA). Market Forecasts are Provided in Terms of Value (USD).

Global Respiratory Virus Infection Drugs Market Trends and Insights

High Elderly and Infant RSV and Influenza Burden Sustains Antiviral Demand

Older adults account for up to 120,000 RSV hospitalizations annually in the United States, while infants under six months face the highest per-capita RSV load . Nirsevimab showed 88.2% effectiveness in Australian infants during the 2024 season and 89.8% in Spain's 2024-2025 season. Baloxavir resistance stayed low at 1.7% overall but rose to 3.6% in H3N2 cases in Japan through 2025. Growing real-world evidence across geriatric and pediatric cohorts is creating dual pillars of steady demand. GSK and Sanofi together booked USD 1.2 billion in 2024 ex-U.S. nirsevimab sales as European health systems backed preventive biologics.

Oral Antivirals Enable Faster Outpatient Access

Time-critical initiation drives interest in pill-based regimens that bypass infusion suites. Despite eligibility, 69% of U.S. patients missed COVID-19 antivirals in 2024, citing prescriber hesitancy and drug interaction fears with ritonavir-boosted products. Ensitrelvir, under FDA review for June 2026, cleared the virus 82% faster than placebo and avoids ritonavir, improving suitability for polypharmacy patients . Forty-two U.S. states allow pharmacists to test and prescribe antivirals the same day, compressing treatment windows. Japan's baloxavir granules broke adherence barriers for children unable to swallow tablets, although 138 mutations were observed in 9.7% of treated pediatric cases. China's March 2026 approvals of oral simnotrelvir-ritonavir and VV-116 added home-use options with higher resistance barriers.

COVID-19 Hospitalization Decline and Lower Public Procurement Depress Volumes

U.S. hospitalizations fell 18% in 2024 versus 2023 and 92% from the January 2022 peak, slashing inpatient demand for remdesivir. Pfizer's Paxlovid sales shrank to USD 1.5 billion in 2024 from USD 12.5 billion in 2022 as public stockpiles depleted and retail pricing rose to USD 1,390 per course. The United Kingdom wrote off GBP 1.7 billion (USD 2.1 billion) in expired Paxlovid during May 2025 . Governments are shifting funds toward RSV and influenza preparedness, leading to a temporary lull in COVID-19 antiviral purchases.

Other drivers and restraints analyzed in the detailed report include:

- Asia-Pacific Healthcare Expansion Boosts Antiviral Utilization

- Long-Acting RSV Monoclonal Antibodies Scale Across Immunization Programs

- Antiviral Resistance and Variant Escape Events

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SARS-CoV-2 products delivered 57.28% of 2025 revenue, but RSV therapies are expanding at 8.87% annually through 2031 as monoclonal antibodies enter pediatric schedules. RSV advances underpin the outlook for the respiratory virus infection drugs market, offering insulation from pandemic volatility. Influenza antivirals remain seasonally stable, with Japan's baloxavir granules widening pediatric reach amid careful resistance monitoring. Combined, non-COVID pathogens contribute over significant share of the current value, and their share is rising steadily.

Real-world data show nirsevimab reaching 88%-90% effectiveness and clesrovimab adding supply depth, reinforcing the respiratory virus infection drugs market share momentum for RSV prophylaxis. COVID-19 demand is flattening at endemic levels, yet ensitrelvir's potential post-exposure label could expand household use cases, diversifying the portfolio and extending lifecycle revenues for protease inhibitors.

Small molecules retained 67.34% revenue dominance in 2025, but the 9.21% CAGR for antibodies signals a shift toward passive prophylaxis solutions. The respiratory virus infection drugs market for monoclonal antibodies is projected to expand fastest in high-risk infant and elderly segments, driven by single-dose convenience and reduced cold-chain waste.

Ritonavir interactions limit nirmatrelvir use in polypharmacy groups, nudging prescribers toward ritonavir-free or biologic options. AstraZeneca and GSK logged combined revenue of USD 2.2 billion from nirsevimab in 2024, demonstrating commercial viability. Combination therapy remains marginal but attracts R&D investment aimed at raising resistance thresholds.

Geography Analysis

North America maintained a 47.29% revenue share in 2025, but growth is plateauing as COVID-19 stockpile use wanes and reimbursement shifts to retail channels. U.S. pharmacist test-to-treat frameworks supply speed advantages, while Canada eyes nationwide expansion after successful provincial pilots. Mexico's adoption is hampered by uneven insurance coverage, although public clinics are adding generic oseltamivir and molnupiravir to formularies.

Europe demonstrates mixed momentum. Germany and the United Kingdom accelerate pharmacist prescribing, yet supply hiccups in France exposed cold-chain weaknesses for RSV biologics. Southern Europe faces slower reimbursement cycles, delaying the introduction of new antivirals. Eastern European markets remain price-sensitive, favoring generics over premium monoclonals.

Asia-Pacific tops the growth chart at an 8.88% CAGR. China's approvals of simnotrelvir and VV-116, plus telemedicine penetration, expand reach into lower-tier cities. Japan's pediatric baloxavir and South Korea's RSV immunization roll-outs support double-digit gains. India's vast manufacturing base gives the region a cost edge, though additional local trials for novel agents prolong time-to-market. Australia's 88.2% nirsevimab effectiveness is catalyzing take-up across Oceania.

- AstraZeneca

- Aurobindo Pharma

- BioCryst Pharmaceuticals

- Cipla

- Roche

- Fujifilm Toyama Chemical

- Genentech (US)

- Gilead Sciences

- GlaxoSmithKline

- Hetero Healthcare

- Invivyd

- Lupin

- Merck

- Pfizer

- Sanofi

- Sawai Pharmaceutical

- Shionogi & Co., Ltd.

- Swedish Orphan Biovitrum

- Teva Pharmaceutical Industries

- Zydus Lifesciences

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Elderly and Infant RSV/Influenza Burden Sustains Antiviral and Mab Demand

- 4.2.2 Oral Antivirals Enable Outpatient Treatment and Faster Access

- 4.2.3 APAC Healthcare Expansion and Surveillance Lift Antiviral Utilization

- 4.2.4 Long-Acting RSV Mab Single-Dose Immunization Scales Across Countries

- 4.2.5 Pharmacist-Prescribed Test-To-Treat Broadens Same-Day Antiviral Initiation

- 4.2.6 China-Led Uptake of Baloxavir and New Antivirals Accelerates Growth

- 4.3 Market Restraints

- 4.3.1 COVID-19 Hospitalization Declines and Waning Public Procurement Depress Volumes

- 4.3.2 Antiviral Resistance and Variant Escape

- 4.3.3 Seasonal Supply and Cold-Chain Limits for RSV mAbs Constrain Coverage

- 4.3.4 Underuse Of Antivirals Among High-Risk Outpatients Reduces Penetration

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Pathogen

- 5.1.1 SARS-CoV-2 (COVID-19)

- 5.1.2 Influenza A/B

- 5.1.3 Respiratory Syncytial Virus (RSV)

- 5.1.4 Human Metapneumovirus (hMPV)

- 5.1.5 Parainfluenza Viruses (PIV 1-4)

- 5.1.6 Adenovirus (respiratory types)

- 5.2 By Modality

- 5.2.1 Small-Molecule Antivirals

- 5.2.2 Monoclonal Antibodies

- 5.2.3 Combination/Adjunctive Regimens

- 5.3 By Route of Administration

- 5.3.1 Oral

- 5.3.2 Intravenous

- 5.3.3 Intramuscular/Subcutaneous

- 5.3.4 Inhaled/Intranasal

- 5.4 By Setting of Care

- 5.4.1 Outpatient/Community

- 5.4.2 Hospital/Acute care

- 5.4.3 Long-term care/Skilled nursing

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of MEA

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 AstraZeneca Plc

- 6.3.2 Aurobindo Pharma USA

- 6.3.3 BioCryst Pharmaceuticals

- 6.3.4 Cipla Limited

- 6.3.5 F. Hoffmann-La Roche

- 6.3.6 Fujifilm Toyama Chemical

- 6.3.7 Genentech (US)

- 6.3.8 Gilead Sciences, Inc

- 6.3.9 GSK plc

- 6.3.10 Hetero Healthcare

- 6.3.11 Invivyd

- 6.3.12 Lupin Pharmaceuticals

- 6.3.13 Merck & Co.

- 6.3.14 Pfizer Inc

- 6.3.15 Sanofi

- 6.3.16 Sawai Pharmaceutical

- 6.3.17 Shionogi & Co., Ltd.

- 6.3.18 Swedish Orphan Biovitrum

- 6.3.19 Teva Pharmaceutical Industries

- 6.3.20 Zydus Lifesciences

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment