PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063521

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063521

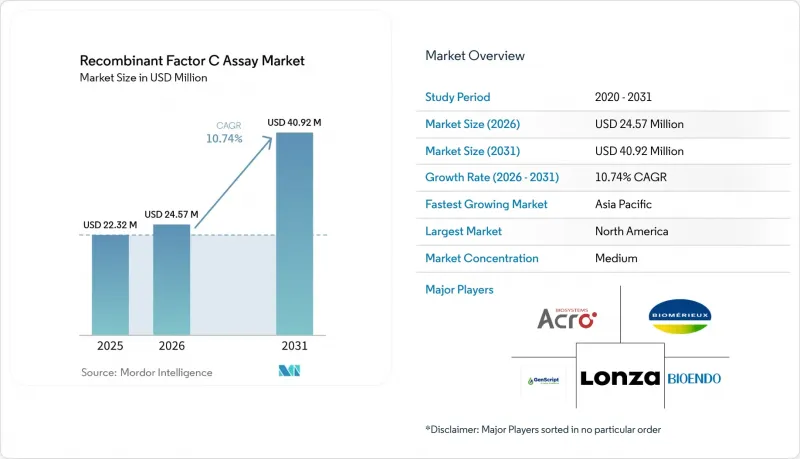

Recombinant Factor C Assay - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the recombinant factor c assay market size is projected to be USD 22.32 million in 2025, USD 24.57 million in 2026, and reach USD 40.92 million by 2031, growing at a CAGR of 10.74% from 2026 to 2031.

This report is Segmented by Product Type (Kits & Reagents, and More), Application (In-Process Water & Raw Materials, and More), End User (Pharma & Biotech Manufacturers, and More), Assay Configuration (Standard Microplate RFC, and More), Throughput Tier, and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Recombinant Factor C Assay Market Trends and Insights

Pharmacopeial Acceptance Accelerates Mainstream Adoption

Formal recognition of non-animal endotoxin methods in USP Chapter 86, effective May 1, 2025, removes the key barrier of inspection uncertainty for manufacturers in the United States. Alignment on water testing has become a catalyst because it represents a high-volume, lower-risk starting point for rFC deployment under routine GMP. Japan, South Korea, and China still operate with language that ranges from under consideration to advisory status, which leaves global suppliers running dual-method comparability in those markets. The net effect is a tiered adoption curve that moves faster in North America and Europe and more cautiously across parts of Asia until further harmonization takes effect.

ESG and Conservation Pressures to Replace LAL with Animal-Free rFC

Horseshoe crab harvest data has sharpened the sustainability debate, with the biomedical harvest in 2022 and bait harvest in 2024 highlighting biodiversity risks that are now tracked by investors and industry coalitions. Corporate ESG programs increasingly view rFC adoption as a measurable action to mitigate ecosystem impact while maintaining quality standards for patient safety, which aligns with the 3Rs principle used by European regulators. The reduction in dependence on wildlife-derived reagents also helps de-risk supply chains that are sensitive to seasonal and regulatory shocks in fishery management. Sector initiatives and purchaser expectations are adding momentum to in-house policy updates that specify animal-free methods where compendial paths are open. As users expand rFC to time-critical releases, they benefit from fewer beta-glucan related false positives, which reduces waste and rework and improves sustainability metrics in practice.

Validation and Comparability Workload with Heterogeneous Regional Acceptance

Manufacturers targeting multiple regulatory jurisdictions face a heavier validation plan because compendial language remains misaligned outside the United States and Europe. China frames rFC in guidance as a principle rather than a binding requirement, and Japan is still evaluating comparative evidence, which sustains dual-method comparability studies for regional dossiers. These programs require multi-lot recovery evaluations and trending analyses, which extend timelines for routine release and for submissions that cross multiple markets. Some product classes also present matrix effects that tighten dilution windows for rFC, which raises the method-suitability workload for complex vaccines and vectors. Until broader harmonization is achieved, large sponsors will continue to run LAL and rFC in parallel for certain markets, which sustains higher operating costs for global portfolios.

Other drivers and restraints analyzed in the detailed report include:

- QC Lab Automation and Digital Traceability Reduce OPEX and Speed Validation

- Beta-Glucan Independence Reduces Invalid and OOS Retesting Burden

- Gel-Clot Dominance and Cost Constraints in Parts of Asia, Africa, South America

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Kits and reagents held the largest share at 68.12% of 2025 revenue, anchored by recurring use that scales with test volume across large biopharma QC operations. Vendors in the recombinant Factor C assay market emphasize format innovations such as pre-optimized substrates and immobilized controls that reduce operator variability in plate-based assays. Instruments and readers showed healthy replacement demand as QC groups retired aging turbidimeters and standardized on multimode fluorescence systems from established suppliers in North America and Europe. Automation and compliance software is projected to deliver the fastest growth at a 12.56% CAGR through 2031 as 21 CFR Part 11 enforcement drives electronic signatures, audit trails, and LIMS integrations across regulated sites. Contract testing services remain a practical route for smaller firms that need method suitability or overflow capacity without full in-house investment, which keeps service demand relevant to the recombinant Factor C assay market.

The recombinant Factor C assay industry continues to migrate toward software-enabled workflows that make complex testing repeatable and audit-ready at scale. Pre-validated software packages translate into shorter validation cycles for change controls and submissions, which reduces friction during inspections. Reader innovations like enhanced dynamic range enable mixed high and low signals on a single plate without manual gain steps, which protects accuracy on first pass for diverse matrices. Across buyers, service models and training support adoption among mid-size QC labs that prefer staged transitions rather than full automation in one step, which diversifies the recombinant Factor C assay market with hybrid operating models.

In-process water and raw-materials testing captured 35.61% of activity in 2025 and remains the most frequent use case because purified water and buffers account for a large share of daily BET volume in regulated plants. Many adopters begin with water testing because compendial pathways are clear and matrix effects are limited, which creates a safe entry point to validate rFC under routine conditions. Finished product release stays more complex since matrix interferences and dilution limits can alter method suitability, which raises the stakes for first-pass success. Device testing remains a steady segment due to ISO and FDA expectations for extract testing and risk management, where animal-free methods align with broader regulatory goals for the recombinant Factor C assay market.

Advanced therapies quality control is projected to expand at a 12.09% CAGR as sponsors scale autologous and allogeneic platforms with very short release windows that cannot absorb retests. EMA's updated guidance for investigational ATMPs strengthens expectations around contamination controls in clinical production, which aligns well with fast, animal-free BET pipelines. Where beta-glucan exposure is likely due to filters, excipients, or process trains, rFC's independence from Factor G reduces false positives and shortens hold times. In this context, the recombinant Factor C assay market provides a practical route to improve release reliability for cell and gene therapy workflows that cannot tolerate delays.

Geography Analysis

North America held 42.17% of the recombinant Factor C assay market share in 2025 due to early alignment with USP Chapter 86 and concentrated biopharma manufacturing across key hubs. The region benefits from a robust ecosystem of QC automation providers and software vendors that support 21 CFR Part 11 compliance, which increases the readiness to adopt rFC in validated workflows. Public conservation data on horseshoe crabs resonates across stakeholders, which supports corporate policies that favor non-animal reagents for sustainability and supply chain resilience. North American CDMOs list recombinant methods in their service portfolios, which helps smaller sponsors transition without full on-site investments.

EMA's updated expectations for ATMPs in clinical production reinforce the value of rapid, animal-free endotoxin testing across cell and gene therapy programs. Across the region, capital planning cycles and replacement schedules shape the pace of transition as older turbidimetric readers give way to multimode fluorescence in GMP facilities.

Asia-Pacific is projected to grow faster than the global average as India and China scale biologics and biosimilar manufacturing capacity and as regional suppliers localize reagent production. Regulatory language remains more conservative in several countries, which sustains dual-method comparability where rFC is advisory rather than compendial, as reflected in current China guidance. Japan continues to examine comparative evidence for recombinant methods, and emerging regulatory updates in South Korea signal more alignment with U.S. expectations in the near term. As harmonization advances, the recombinant Factor C assay market will gain from faster validations and lower reliance on wildlife-derived reagents across regional manufacturing centers.

- ACROBiosystems Co., Ltd.

- Bioendo rFC Endotoxin Test Kit

- bioMerieux

- BMG LABTECH GmbH

- Cormica Ltd.

- Eurofins BioPharma Product Testing

- Genscript

- Hzymes Biotechnology

- Indoor Biotechnologies, Inc.

- INTEGRA Biosciences

- Lonza Group

- Microcoat Biotechnologie

- Xiamen Bioendo Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Pharmacopeial acceptance accelerates mainstream adoption (EU Ph. Eur. rFC compendial; USP <86> official)

- 4.2.2 ESG and conservation pressures to replace LAL with animal-free rFC

- 4.2.3 First FDA drug release using rFC builds confidence in regulated use

- 4.2.4 QC lab automation (microplate fluorescence, digital traceability) reduces OPEX and speeds validation

- 4.2.5 Enterprise supply-chain risk diversification and multi-sourcing favor rFC

- 4.2.6 Beta-glucan independence (no Factor G) reduces invalid/OOS runs and retesting burden

- 4.3 Market Restraints

- 4.3.1 Validation and comparability workload; heterogeneous regional acceptance

- 4.3.2 Gel-clot dominance and cost constraints in parts of Asia, Africa, South America slow replacement

- 4.3.3 Higher rFC kit costs and fluorescence reader capex for small labs

- 4.3.4 Inter-supplier variability and product-matrix effects slow standardization

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Kits & Reagents (rFC assay kits)

- 5.1.2 Pre-coated plates/strips

- 5.1.3 Instruments & Readers

- 5.1.4 Automation & Compliance Software

- 5.1.5 Contract Testing Services

- 5.2 By Application

- 5.2.1 In-process water & raw materials

- 5.2.2 Final drug product release

- 5.2.3 Advanced therapies (cell/gene therapy) QC

- 5.2.4 Medical device BET

- 5.2.5 Others

- 5.3 By End User

- 5.3.1 Pharma & Biotech manufacturers

- 5.3.2 CDMOs/CMOs

- 5.3.3 Medical device manufacturers

- 5.3.4 Others

- 5.4 By Assay Configuration

- 5.4.1 Standard microplate rFC

- 5.4.2 Pre-coated GO plates/strips

- 5.4.3 Automation-integrated rFC workflows

- 5.5 By Throughput Tier

- 5.5.1 High-volume QC labs

- 5.5.2 Mid-volume labs

- 5.5.3 Low-volume/point workflows

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 ACROBiosystems Co., Ltd.

- 6.3.2 Bioendo rFC Endotoxin Test Kit

- 6.3.3 bioMerieux SA

- 6.3.4 BMG LABTECH GmbH

- 6.3.5 Cormica Ltd.

- 6.3.6 Eurofins BioPharma Product Testing

- 6.3.7 GenScript Biotech Corporation

- 6.3.8 Hzymes Biotechnology

- 6.3.9 Indoor Biotechnologies, Inc.

- 6.3.10 INTEGRA Biosciences

- 6.3.11 Lonza Group AG

- 6.3.12 Microcoat Biotechnologie GmbH

- 6.3.13 Xiamen Bioendo Technology Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment