PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063530

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063530

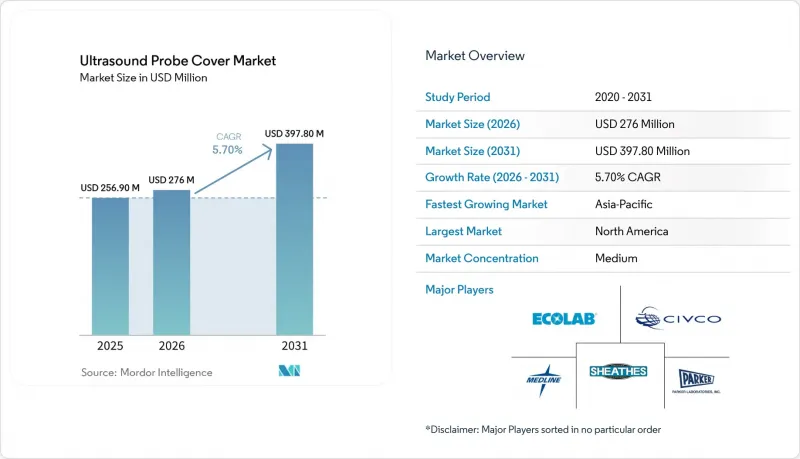

Ultrasound Probe Cover - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the ultrasound probe cover market size is projected to be USD 256.90 million in 2025, USD 276 million in 2026, and reach USD 397.80 million by 2031, growing at a CAGR of 5.70% from 2026 to 2031.

This report is Segmented by Cover Type (Disposable, Reusable), Material (Latex-Free, Latex), Sterility (Sterile, Non-Sterile), Probe Application (Endocavitary, and More), End-User (Hospitals, ASC, Diagnostic Imaging Centers, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Ultrasound Probe Cover Market Trends and Insights

Rising Ultrasound Procedure Volumes

Clinical imaging workloads are increasing as aging populations face chronic disease screenings and obstetric monitoring requirements. Countries such as Japan, South Korea, and several in Western Europe are experiencing double-digit growth in outpatient ultrasound visits. Similarly, China's township clinics have reported a rise in ultrasound procedures following increased equipment allocations under the "Healthy China 2030" initiative. Each additional scan necessitates the use of at least one new cover or a high-level disinfection cycle. Hospitals without automated processors often rely on single-use barriers to maintain operational efficiency. The relationship is straightforward: more scans result in a higher number of probes in circulation daily. Administrators have effectively translated radiology booking data into forward orders for covers through materials-management software. Consequently, the growth in diagnostic procedures directly drives the ultrasound probe cover market, offering suppliers clear demand signals and predictable volume growth.

Stricter Infection-Control Regulations

Infection-control regulations classify transvaginal and transrectal transducers as semi-critical devices that require either high-level disinfection or the use of sterile, single-use covers between patients. Accreditation bodies now audit probe-cover inventory logs and penalize hospitals unable to link every endocavitary scan to a documented barrier or reprocessing record. Similar regulatory vigilance is enforced in Europe, and leading hospital chains in the Asia-Pacific region are adopting these standards to secure certifications critical for medical tourism. The risk of reputational damage and potential malpractice litigation has prompted administrators to prioritize sterile covers over reusable sheaths, even when the latter remains legally permissible. This regulatory environment continues to expand the ultrasound probe cover market as facilities adopt risk-averse practices and shift toward disposable solutions.

Single-Use Plastic Sustainability Concerns

The EU's Single-Use Plastics Directive enforces extended producer responsibility programs, holding manufacturers accountable for downstream waste management. Similarly, California's recycling regulations impose stringent targets, while advocacy groups evaluate hospitals' plastic usage through annual assessments. In response, industry leaders are piloting polylactic acid films that biodegrade in industrial composting environments while maintaining sterility standards. However, high costs, limited resin availability, and inadequate end-of-life infrastructure restrict broader adoption. Until bio-based polymers achieve comparable performance in barrier integrity and cost-effectiveness, environmental regulations are likely to impact the growth trajectory of the ultrasound probe cover market.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Disposable Covers

- Growth of Point-of-Care Ultrasound

- Cost Pressure in Low-Resource Settings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, disposable solutions contributed 61.34% of revenue and are projected to grow at a 5.95% CAGR, outperforming reusable sheaths across all monitored regions. This dominance is primarily driven by the labor-intensive requirements of sterile processing, as each reusable sleeve necessitates rinsing, leak testing, disinfection, drying, and documentation. Staffing shortages exacerbate these challenges, making disposables a reliable solution to mitigate human error and avoid compliance issues. Manufacturers have enhanced single-use items by incorporating antimicrobial coatings and RFID chips, further differentiating them from reusable alternatives. While reusable covers remain a tactical choice in budget-constrained scenarios, global health organizations increasingly allocate funding to disposables to ensure barrier integrity. Consequently, disposables are driving both volume and innovation in the ultrasound probe cover market.

In 2025, latex accounted for 56.75% of units shipped, largely due to the availability and cost-effectiveness of natural rubber in Southeast Asia. However, materials such as nitrile, polyisoprene, and polyethylene are growing at a 6.03% CAGR, the fastest among material categories. Clinical data indicating that up to 17% of healthcare workers experience latex sensitivities has prompted risk assessments and led procurement teams to eliminate latex from institutional inventories. Synthetic elastomers have nearly matched natural rubber in tensile strength and elasticity, resulting in only a slight cost premium. Hospitals that previously maintained separate inventories for latex and non-latex products now default to latex-free options, simplifying inventory management and protecting staff from hypersensitivity risks.

Geography Analysis

In 2025, North America accounted for 38.96% of global revenue, driven by U.S. hospitals' adherence to stringent infection-control protocols and the adoption of automated high-level disinfection units. In Canada, bulk purchasing by provincial consortia boosts demand, while private healthcare chains in Mexico import premium antimicrobial covers to attract medical tourists. Despite market saturation and reimbursement challenges, the region's ultrasound probe cover market continues to grow steadily, supported by the shift toward outpatient surgery and point-of-care imaging.

Asia-Pacific is the fastest-growing region, with a 6.10% CAGR. In China, government initiatives are equipping township clinics with ultrasound units, driving demand for cost-effective barriers, while urban centers are adopting premium, latex-free products to meet international standards. In India, rising diagnostic volumes under national healthcare programs are offset by affordability challenges in public hospitals, slowing the adoption of premium products. Japan and South Korea lead in per-capita usage, driven by aging populations and early adoption of advanced covers. Australia aligns with North American standards, while Thailand and Singapore invest in robust supply chains to strengthen their medical tourism sectors.

Europe occupies a middle ground, with Germany, France, and the UK driving volume. However, the EU's Single-Use Plastics Directive is prompting suppliers to invest in biodegradable solutions and account for recycling costs. Southern European countries grow moderately, with public tenders emphasizing cost, leading to intense price competition. In the Middle East, Saudi Arabia and the UAE are channeling investments into advanced healthcare infrastructure, increasing demand for sterile covers. In Africa, donor-funded programs dominate, but urban private hospitals in countries like Kenya and Nigeria are beginning to adopt premium products, signaling potential growth as economic conditions improve.

- 3M

- Advance Medical Designs

- Ascent Care Medical

- Aspen Surgical

- B. Braun

- Cardinal Health

- CIVCO Medical solutions

- Ecolab

- Fairmont Medical Products

- FUJILATEX Co., Ltd.

- Karex Berhad

- Mckesson

- Medline Industries

- Nanosonics Ltd.

- Parker Laboratories

- PDC Healthcare

- Protek Medical Products

- Sheathing Technologies

- STERIS

- Vermed

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Ultrasound Procedure Volumes

- 4.2.2 Stricter Infection-Control Regulations

- 4.2.3 Shift to Disposable Covers

- 4.2.4 Growth of Point-of-Care Ultrasound

- 4.2.5 Antimicrobial & Smart-Sensor Covers Adoption

- 4.2.6 Growth of Auto-Replenishment Solutions in the E-Commerce

- 4.3 Market Restraints

- 4.3.1 Single-Use Plastic Sustainability Concerns

- 4.3.2 Cost Pressure In Low-Resource Settings

- 4.3.3 Resin Additive Supply-Chain Risks

- 4.3.4 Probe-Dimension Standardization Gaps

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Cover Type

- 5.1.1 Disposable Covers

- 5.1.2 Reusable Covers

- 5.2 By Material

- 5.2.1 Latex-Free Covers

- 5.2.2 Latex Covers

- 5.3 By Sterility

- 5.3.1 Sterile Covers

- 5.3.2 Non-Sterile Covers

- 5.4 By Probe Application

- 5.4.1 Endocavitary Probes

- 5.4.2 External Surface Probes

- 5.4.3 Intraoperative Probes

- 5.4.4 Other Applications

- 5.5 By End-User

- 5.5.1 Hospitals

- 5.5.2 Ambulatory Surgical Centers

- 5.5.3 Diagnostic Imaging Centers

- 5.5.4 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 3M Healthcare

- 6.3.2 Advance Medical Designs

- 6.3.3 Ascent Care Medical

- 6.3.4 Aspen Surgical

- 6.3.5 B. Braun Melsungen AG

- 6.3.6 Cardinal Health

- 6.3.7 CIVCO Medical Solutions

- 6.3.8 Ecolab

- 6.3.9 Fairmont Medical Products

- 6.3.10 FUJILATEX Co., Ltd.

- 6.3.11 Karex Berhad

- 6.3.12 McKesson Corporation

- 6.3.13 Medline Industries

- 6.3.14 Nanosonics Ltd.

- 6.3.15 Parker Laboratories

- 6.3.16 PDC Healthcare

- 6.3.17 Protek Medical Products

- 6.3.18 Sheathing Technologies

- 6.3.19 Steris Corporation

- 6.3.20 Vermed

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment