PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063532

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063532

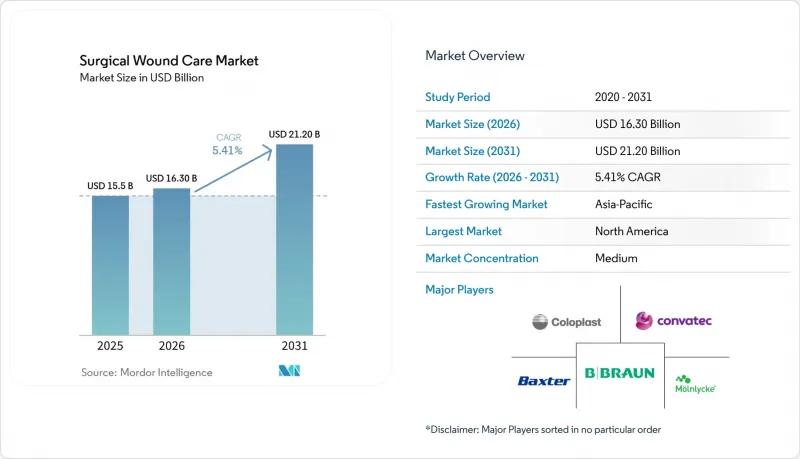

Surgical Wound Care - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the surgical wound care market size is expected to increase from USD 15.5 billion in 2025 to USD 16.30 billion in 2026 and reach USD 21.20 billion by 2031, growing at a CAGR of 5.41% over 2026-2031.

This report is Segmented by Product Type (Traditional Products, Advanced Dressings, Sutures & Stapling Devices, Surgical Sealants & Glues, Hemostats, Anti-Infective Agents), Wound Type (Acute Wounds, Chronic Wounds), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Surgical Wound Care Market Trends and Insights

Growing Adoption of Minimally Invasive Surgical Procedures

Robotic and laparoscopic techniques are increasingly being adopted due to their ability to minimize incision sizes, reduce tissue trauma, and shorten hospital stays. These advancements have led to a decline in the use of traditional gauze while driving demand for barbed sutures, tissue adhesives, and thin antimicrobial films. This shift has also contributed to a reduction in infection rates, with robotic procedures showing a 1.2% infection rate compared to 4.7% for open hysterectomies. Smaller wounds are shifting postoperative care to outpatient or home settings, where telehealth monitoring enhances adherence and reduces readmission risks. In response, manufacturers are expanding their product portfolios to include self-adhering antimicrobial dressings designed for delicate tissue planes and robotic workflows.

Rising Prevalence of Chronic Diseases Requiring Surgical Interventions

The increasing prevalence of chronic conditions such as diabetes, obesity, and peripheral vascular disease is complicating surgical wound management and prolonging healing times. Diabetic foot ulcers affect 6.3% of the population, with a lifetime risk of 34%, contributing to approximately 1 million diabetes-related amputations annually. In the United States, direct treatment costs range between USD 9-13 billion annually, with 80% of amputations preceded by a foot ulcer. Although guidelines recommend maintaining peri-operative HbA1c levels at 8% and intra-operative glucose levels between 100-180 mg/dL by 2026, compliance challenges in community hospitals continue to result in higher infection rates. These challenges are driving the development of advanced solutions such as bioactive collagen matrices, peptide-infused barriers, and growth-factor-laden foams, which aim to stimulate stalled angiogenesis and accelerate the inflammatory phase.

High Costs Hinder Adoption of Advanced Surgical Wound Care Products

Premium closures and bioactive dressings are priced 3-10 times higher than standard gauze and nylon sutures, limiting their adoption in cost-sensitive regions. Newly introduced antimicrobial-peptide dressings are sold at USD 15-25 per 10X10 cm sheet, compared to USD 2-4 for traditional foams. Negative-pressure wound-therapy (NPWT) systems, such as AOTI's NEXA, require an upfront investment of USD 1,500-3,000, excluding disposables, which discourages adoption in resource-constrained hospitals. Supply-chain disruptions in 2025 caused a 50% increase in the cost of polymer and aluminum inputs in India, driving up overall device prices. As a result, budget-constrained facilities often resort to basic care, leading to persistently high infection rates.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Volume of Ambulatory Surgeries

- Technological Advancements in Antimicrobial Sutures & Dressings

- Emerging Economies Face Reimbursement Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, wound-closure systems, considered essential in surgeries, accounted for 53.10% of the surgical wound care market size. In March 2026, Smith+Nephew introduced ALLEVYN COMPLETE CARE, a product designed to manage high-exudate wounds by combining silicone contact layers with superabsorbent foam cores. Advanced dressings, enhanced by antimicrobial peptides, collagen matrices, and smart foams, are projected to grow at the fastest rate of 5.83% CAGR through 2031. ConvaTec's AQUACEL Ag Foam continues to gain traction in burn units, while Freudenberg's Tacnera is increasingly used for pressure ulcer prevention in long-term care settings.

Surgical sealants and hemostats are becoming more relevant in minimally invasive and robotic procedures, where suture placement can be challenging. In February 2026, Baxter launched Hemopatch, designed for rapid hemostasis in cardiovascular and hepatobiliary applications. Grifols' VISTASEAL expanded its pediatric labeling in October 2024, addressing congenital heart surgeries.

Geography Analysis

In 2025, North America accounted for 41.98% of the revenue, driven by ASC expansion, high per-capita spending, and a robust payer infrastructure in the United States. Reimbursement reforms are driving clinic consolidation and reinforcing hospital dominance, while also creating opportunities for AI-enabled home monitoring solutions. Canada and Mexico contribute smaller shares but are experiencing growth due to aging populations and increasing diabetes prevalence.

Asia-Pacific is projected to achieve a 5.86% CAGR from 2026 to 2031, supported by rising surgical volumes, new insurance initiatives, and infrastructure investments in China, India, and Japan. India's PM-JAY scheme, despite its coverage limitations, is expanding procedural access, although the private sector continues to dominate. Japan, where 28% of the population is aged 65 or older, is scaling up pressure ulcer prevention and chronic wound care programs. South Korea and Australia are deploying AI-integrated imaging solutions to enhance healthcare delivery.

Europe maintains steady growth due to universal healthcare coverage. However, supply chain disruptions caused by geopolitical tensions are increasing device costs, prompting providers to explore regional sourcing strategies. The Middle East & Africa and South America, despite facing reimbursement challenges, are seeing incremental growth through private hospitals catering to medical tourism and expatriate communities.

- 3M Company (Solventum)

- Advanced Medical Solutions Group

- Argentum Medical LLC

- B. Braun

- Baxter

- BSN medical (Essity AB)

- Coloplast

- ConvaTec Group plc

- Derma Sciences Inc. (Integra)

- HARTMANN Group

- Integra LifeSciences Holdings Corp.

- Johnson & Johnson

- Lohmann & Rauscher

- Medline Industries

- Medtronic

- MIMEDX Group Inc.

- Molnlycke Health Care

- Organogenesis

- PolyNovo Ltd.

- Smiths Group

- Zimmer Biomet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Minimally Invasive Surgical Procedures

- 4.2.2 Rising Prevalence of Chronic Diseases Requiring Surgical Interventions

- 4.2.3 Increasing Volume of Ambulatory Surgeries

- 4.2.4 Technological Advancements in Antimicrobial Sutures & Dressings

- 4.2.5 Surge in Surgical Site Infections Prompting Preventive Care

- 4.2.6 Shift to Outpatient Wound Centers Integrated With AI-Enabled Remote Monitoring

- 4.3 Market Restraints

- 4.3.1 High Cost of Advanced Surgical Wound Care Products

- 4.3.2 Reimbursement Challenges in Emerging Economies

- 4.3.3 Sterile Supply-Chain Disruptions Due to Geopolitical Conflicts

- 4.3.4 Growing Preference for Non-Surgical Treatment Alternatives

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Pricing Analysis

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Wound Closure System

- 5.1.2 Advanced Dressings

- 5.1.3 Sutures & Stapling Devices

- 5.1.4 Surgical Sealants & Glues

- 5.1.5 Hemostats

- 5.1.6 Anti-infective Agents

- 5.2 By Wound Type

- 5.2.1 Acute Wounds

- 5.2.1.1 Incisional Wounds

- 5.2.1.2 Traumatic Wounds

- 5.2.2 Chronic Wounds

- 5.2.2.1 Diabetic Foot Ulcers

- 5.2.2.2 Pressure Ulcers

- 5.2.2.3 Venous Leg Ulcers

- 5.2.1 Acute Wounds

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Specialty Clinics

- 5.3.4 Home Healthcare

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 3M Company (Solventum)

- 6.3.2 Advanced Medical Solutions Group plc

- 6.3.3 Argentum Medical LLC

- 6.3.4 B. Braun Melsungen AG

- 6.3.5 Baxter International Inc.

- 6.3.6 BSN medical (Essity AB)

- 6.3.7 Coloplast A/S

- 6.3.8 ConvaTec Group plc

- 6.3.9 Derma Sciences Inc. (Integra)

- 6.3.10 HARTMANN Group

- 6.3.11 Integra LifeSciences Holdings Corp.

- 6.3.12 Johnson & Johnson (Ethicon)

- 6.3.13 Lohmann & Rauscher GmbH & Co. KG

- 6.3.14 Medline Industries, LP

- 6.3.15 Medtronic plc

- 6.3.16 MIMEDX Group Inc.

- 6.3.17 Molnlycke Health Care

- 6.3.18 Organogenesis Holdings Inc.

- 6.3.19 PolyNovo Ltd.

- 6.3.20 Smith & Nephew plc

- 6.3.21 Zimmer Biomet Holdings Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment