PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063534

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063534

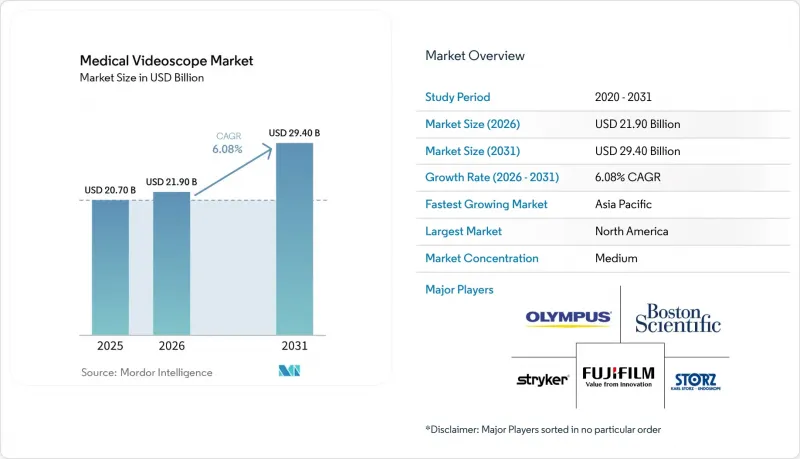

Medical Videoscope - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the medical videoscope market size is projected to be USD 20.70 billion in 2025, USD 21.90 billion in 2026, and reach USD 29.40 billion by 2031, growing at a CAGR of 6.08% from 2026 to 2031.

This report is Segmented by Scope Design (Flexible Reusable, Rigid, Single-Use/Disposable), Clinical Application (Gastroenterology, Pulmonology, and More), End User (Hospitals, Ascs & AECs, and More), Imaging/Resolution (HD, 4K/UHD, 3D, NIR/Fluorescence), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Value (USD).

Global Medical Videoscope Market Trends and Insights

Rising Endoscopy Volumes From GI, Respiratory, And Urologic Disease Burdens

Demographic shifts toward aging populations and the increasing prevalence of chronic diseases are driving higher volumes of gastrointestinal, pulmonary, and urologic procedures, sustaining the demand for videoscope platforms. Australia's National Lung Cancer Screening Program, launched in 2025, conducted 37,000 low-dose CT scans in its initial five months, identifying 426 high-risk nodules for bronchoscopic evaluation. In the United States, lung cancer screening eligibility expanded in 2024, removing the 15-year post-smoking limit and lowering the age threshold to 50 for individuals with a 20-pack-year smoking history, effectively doubling the eligible population. Navigational bronchoscopy and robotic-assisted platforms are increasingly preferred over percutaneous biopsy due to their ability to significantly reduce pneumothorax risk from 28.3% to 3.3% in comparative studies. Similar growth trends are observed in colorectal, bladder, and upper-GI procedures, driven by broader screening programs and the transition from open surgery to therapeutic endoscopy.

Shift To Minimally Invasive Surgery And Outpatient/ASC Sites Of Care

Payment reforms and capacity constraints are shifting procedures from inpatient departments to ambulatory surgical centers (ASCs). Between 2017 and 2024, the number of Medicare-certified endoscopy ASCs in the United States increased by 46.7%, accompanied by a parallel rise in ASC spending on gastrointestinal procedures. ASCs are increasingly adopting leasing arrangements and single-use scopes, contributing to a 6.35% compound annual growth rate (CAGR) in disposable videoscopes. Additionally, the consolidation of physician employment, with 78% of U.S. physicians working for hospitals or corporations in 2023, is centralizing procurement decisions and encouraging the adoption of standardized, AI-ready tower platforms.

High Capital Intensity And Lifecycle Service/Repair Costs

Smaller facilities and hospitals in emerging markets face significant financial challenges due to substantial upfront equipment investments and ongoing maintenance expenses. These factors limit market penetration and extend replacement cycles. An endoscopy tower, which includes a processor, light source, insufflator, and display, can cost over USD 200,000. Adding 4K or 3D capabilities increases the cost to over USD 300,000. In 2024, the total cost per endoscopy procedure was estimated at approximately USD 135, with equipment depreciation and service contracts accounting for 22% of the total. Repairing flexible videoscopes typically incurs an average cost of USD 1,200 per incident. Preventive-maintenance protocols have proven effective in reducing repair costs, with one high-volume academic center cutting annual repair expenses from USD 1.2 million to USD 724,000. Leasing models and refurbished-equipment markets have emerged as alternatives to address capital constraints. However, these options often exclude the latest imaging modalities and AI-enabled processors, perpetuating a technology gap between well-funded tertiary centers and community hospitals.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Upgrades To 4K/UHD, 3D, NIR/Fluorescence, And AI-Assisted Visualization

- Infection-Prevention Push Accelerating Adoption Of Single-Use Videoscopes

- Reprocessing Complexity And Regulatory Scrutiny Increasing Compliance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, reusable flexible scopes accounted for 53.10% of the revenue, highlighting their cost efficiency in high-volume gastroenterology suites. However, with stricter infection control mandates, single-use models are projected to grow at a compound annual growth rate (CAGR) of 6.35% through 2031. Ambu's aScope 5 Cysto HD offers high-definition imaging while eliminating reprocessing delays. In January 2026, Olympus introduced the SecureFlex single-use biopsy device to address cross-contamination concerns in pancreatic procedures. Adoption trends indicate that gastroenterology continues to favor reusable scopes for colonoscopies, whereas pulmonology and urology increasingly prefer disposable scopes in intensive care and emergency settings due to their immediate availability.

In 2025, gastroenterology led the market with 42.40% of the revenue, driven by colorectal cancer screenings and therapeutic interventions. Pulmonology, however, is expected to grow at an annual rate of 6.46%, supported by expanded screening eligibility and advancements in robotic bronchoscopy, which have significantly improved diagnostic sensitivity to 85%. National screening programs in Australia and pilot initiatives in China are further accelerating this growth. As these programs mature, pulmonology is anticipated to narrow its revenue gap with gastroenterology in the medical videoscope market.

Geography Analysis

In 2025, North America accounted for 32.19% of the revenue, driven by extensive ASC networks, strong reimbursement systems, and rapid adoption of AI-ready processors. The region's growth aligns with the global 6.08% CAGR but is moderated by market maturity and staffing constraints. Additionally, regulatory safety alerts regarding duodenoscope reprocessing are accelerating the transition to single-use instruments. Canada and Mexico are investing in colon cancer screening programs, although their budgets remain lower compared to those of the United States.

Europe is prioritizing reusable scopes, supported by stringent reprocessing protocols. Regulatory changes under the EU Medical Device Regulation are compelling suppliers to simplify channel geometries. Furthermore, France's 2025 guidelines recommend limiting the use of disposable scopes to high-risk cases. However, sustainability concerns are hindering the growth of single-use instruments in Western Europe.

Asia-Pacific is the fastest-growing region, with a 6.43% CAGR. China's localization initiatives enabled a major manufacturer to secure regulatory approval for domestically produced gastroscopes in September 2025, opening opportunities in public procurement. Additionally, Australia's nationwide screening programs and India's rapid hospital infrastructure development are driving regional demand. In Japan, despite stagnant population growth, the aging population sustains high procedure volumes.

The Middle East, Africa, and South America represent smaller market shares but demonstrate significant growth potential. Gulf Cooperation Council countries are investing in advanced 4K systems to strengthen their medical tourism offerings. Meanwhile, Brazil is incorporating endoscopy expansion into its national cancer-control strategies. However, these regions face challenges such as currency fluctuations and import restrictions.

- Ambu

- Arthrex

- B. Braun

- Boston Scientific

- Conmed

- EndoMed Systems GmbH

- FUJIFILM

- HOYA Corporation (PENTAX Medical)

- Karl Storz

- Medtronic

- Mindray

- Olympus

- Pristine Surgical

- Richard Wolf

- Smith+Nephew plc

- SonoScape Medical

- Stryker

- Verathon

- Xenocor, Inc.

- XION GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Endoscopy Volumes From GI, Respiratory, And Urologic Disease Burdens

- 4.2.2 Shift To Minimally Invasive Surgery and Outpatient/ASC Sites of Care

- 4.2.3 Rapid Upgrades To 4K/UHD, 3D, NIR/Fluorescence, And AI-Assisted Visualization

- 4.2.4 Infection-Prevention Push Accelerating Adoption of Single-Use Videoscopes

- 4.2.5 AI-Enabled Detection/Decision Support Embedded in Processors and Workflows

- 4.2.6 Localization And Public Procurement Programs in China and Emerging Markets

- 4.3 Market Restraints

- 4.3.1 High Capital Intensity and Lifecycle Service/Repair Costs

- 4.3.2 Reprocessing Complexity and Regulatory Scrutiny Increasing Compliance Burden

- 4.3.3 Shortage Of Trained Endoscopists and Reprocessing Technicians

- 4.3.4 Sustainability And Waste Pressures Limiting Single-Use Adoption in Some Regions

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Scope Design

- 5.1.1 Flexible Reusable Videoscopes

- 5.1.2 Rigid Videoscopes

- 5.1.3 Single-use/Disposable Videoscopes

- 5.2 By Clinical Application

- 5.2.1 Gastroenterology

- 5.2.2 Pulmonology

- 5.2.3 Urology

- 5.2.4 General Surgery / Laparoscopy

- 5.2.5 ENT / Otolaryngology

- 5.2.6 Orthopedics / Arthroscopy

- 5.2.7 Gynecology / Hysteroscopy

- 5.2.8 Others

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers (ASCs) & Ambulatory Endoscopy Centers (AECs)

- 5.3.3 Specialty Clinics / Office-based Settings

- 5.3.4 Others

- 5.4 By Imaging / Resolution

- 5.4.1 High Definition (HD)

- 5.4.2 4K / Ultra High Definition (UHD)

- 5.4.3 3D imaging

- 5.4.4 Near-Infrared (NIR) / Fluorescence-enabled

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Ambu A/S

- 6.3.2 Arthrex, Inc.

- 6.3.3 B. Braun SE

- 6.3.4 Boston Scientific Corporation

- 6.3.5 CONMED Corporation

- 6.3.6 EndoMed Systems GmbH

- 6.3.7 FUJIFILM Holdings Corporation

- 6.3.8 HOYA Corporation (PENTAX Medical)

- 6.3.9 KARL STORZ SE & Co. KG

- 6.3.10 Medtronic plc

- 6.3.11 Mindray

- 6.3.12 Olympus Corporation

- 6.3.13 Pristine Surgical

- 6.3.14 Richard Wolf GmbH

- 6.3.15 Smith+Nephew plc

- 6.3.16 SonoScape Medical

- 6.3.17 Stryker Corporation

- 6.3.18 Verathon Inc.

- 6.3.19 Xenocor, Inc.

- 6.3.20 XION GmbH

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment