PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063542

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063542

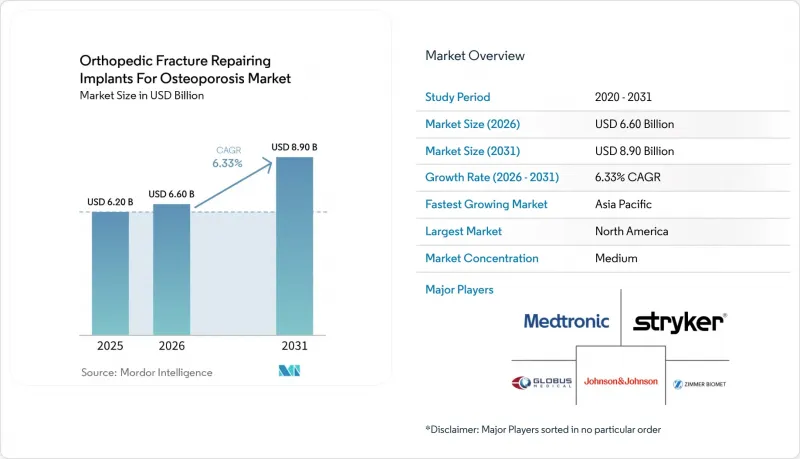

Orthopedic Fracture Repairing Implants For Osteoporosis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the orthopedic fracture repairing implants for osteoporosis market size is expected to increase from USD 6.20 billion in 2025 to USD 6.60 billion in 2026 and reach USD 8.90 billion by 2031, growing at a CAGR of 6.33% over 2026-2031.

This report is Segmented by Implant Type (Fixation Devices, and More), Fracture Site (Hip/Proximal Femur, Vertebral, Distal Radius, Proximal Humerus, and More), Material (Titanium Alloys, Stainless Steel, Cobalt-Chromium, Bioabsorbable Polymers, and More), End User (Hospitals, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global Orthopedic Fracture Repairing Implants For Osteoporosis Market Trends and Insights

Aging Population and Rising Fragility Fracture Burden

Fragility fractures already reach more than 2 million episodes annually in the United States, and each hip fracture carries a one-year mortality above 20% with direct costs around USD 40,000. Japan reports 180,000 hip fractures per year, while 29.1% of its citizens are now at least 65 years old. A 2024 hospital audit in northeastern China showed hip fractures made up a significant number of overall osteoporotic fractures and revealed that fewer than 9% of patients received anti-osteoporotic drugs afterward, setting the stage for refracture. These numbers confirm the demographic "locked-in" demand for orthopedic fracture-repairing implants for osteoporosis, but they also highlight the engineering challenge of anchoring implants securely in bone that has lost structural density.

Minimally Invasive Vertebral Augmentation Adoption

The North American Spine Society's 2025 clinical guideline endorses vertebral augmentation after 4-6 weeks of failed conservative care, aligning payer policy with clinical preference. Systems such as Merit Medical's DFINE StabiliT MX use steerable osteotomes and high-viscosity PMMA to cut leakage rates, while Stryker's FDA-cleared SpineJack lifts the endplate with up to 1,000 N of force before cement fill. Because the procedure is percutaneous and lasts under 40 minutes, it is quickly moving into ambulatory surgical centers, where average payer savings are USD 2,602 per case and weekday block time is plentiful.

Evidence Controversy and Variable Payer Coverage for Vertebral Augmentation

Early placebo-controlled trials showed limited benefit compared with sham procedures, so several U.S. regional plans still require advanced imaging evidence of a vertebral cleft before authorizing treatment. Denials force practices to spend administrative time on appeals, slowing the growth of procedures in lower-margin offices. Manufacturers are therefore underwriting large post-market registries to produce the real-world evidence that payers demand.

Other drivers and restraints analyzed in the detailed report include:

- Advances in Osteoporotic Fixation Technology

- Favorable Reimbursement and Care Pathways for Early Hip-Fracture Surgery

- Cement Leakage and Perioperative Safety Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vertebral augmentation systems are forecast to clock a 6.76% CAGR through 2031. Fixation devices generated 58.30% of 2025 revenue but now face generic competition in plating and nailing. Cement toolkits remain the smallest slice yet ride the shift toward fenestrated hardware and calcium-phosphate cements.

Surgeons are demanding expandable implants that restore height and use smaller cement volumes, opening the door to differentiated pricing. FDA clearance of Medtronic's Catalyft PTC for tibial applications hints at expansion beyond the spine. Suppliers that harmonize delivery devices, PMMA cartridges, and fenestrated screws within a single kit are capturing purchasing-committee preference for integrated solutions.

Hip and proximal femur fractures still accounted for 38.63% of revenue in 2025, as emergency-department protocols ensure near-universal surgical intervention. Yet vertebral compression fractures logged the fastest growth, with a 6.95% CAGR, as opportunistic CT scanning and Fracture Liaison Services highlight silent wedge deformities. The orthopedic fracture-repairing implants for osteoporosis market share for vertebral cases is expected to surge significantly by 2031.

Distal radius practice is shifting toward low-profile volar plates, allowing immediate wrist motion, while proximal humerus management is turning to cement-augmented screws after randomized data confirmed lower varus collapse. Minimally invasive navigation-guided screws now make pelvic fixation possible in frail octogenarians, expanding a niche that once defaulted to bed rest.

Geography Analysis

North America generated 43.18% of global revenue in 2025, buoyed by Medicare's separate payment for device-intensive procedures. Asia-Pacific is the growth engine, with a 7.5% CAGR by 2031 as China and India scale trauma infrastructure. Europe benefits from integrated secondary-prevention networks that funnel fragility-fracture patients to surgeons at a rate 20-30 points above minimally organized systems.

South America and the Middle East are trailing, but GCC governments are funding orthopedic centers of excellence, and Brazil's aging urban cohort is driving demand for hip nails. The orthopedic fracture-repairing implants for osteoporosis market share in Asia-Pacific is forecast to surge significantly by 2031.

- AAP Implantate

- Acumed (Colson Medical)

- B. Braun (Aesculap)

- Bioretec

- CarboFix (Carboclear)

- Double Medical (China)

- G21 S.r.l.

- Globus Medical

- Johnson & Johnson

- Medartis

- Medtronic

- Merit Medical (DFINE StabiliT)

- Orthofix

- OSSIO

- Paragon 28

- Smiths Group

- Stryker

- Tecres S.p.A.

- Teknimed

- Waston Medical

- Weigao Orthopaedic

- Zimmer Biomet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Population and Rising Fragility Fracture Burden

- 4.2.2 Minimally Invasive Vertebral Augmentation Adoption

- 4.2.3 Advances In Osteoporotic Fixation (Locking Plates, CM Nails, Fenestrated Screws)

- 4.2.4 Favorable Reimbursement and Care Pathways for Early Hip-Fracture Surgery

- 4.2.5 Fracture Liaison Services (FLS) Scaling Surgical Capture

- 4.2.6 Cement-Augmented Fixation Expanding Indications in Poor Bone

- 4.3 Market Restraints

- 4.3.1 Evidence Controversy and Variable Payer Coverage for Vertebral Augmentation

- 4.3.2 Cement Leakage and Perioperative Safety Risks

- 4.3.3 Hospital Tendering and DRG Cost Pressure on Premium Kits

- 4.3.4 Under diagnosis/Under-Reporting of Vertebral Fractures

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Implant Type

- 5.1.1 Fixation Devices

- 5.1.2 Vertebral augmentation

- 5.1.3 Cement delivery & augmentation toolkits

- 5.2 By Fracture Site

- 5.2.1 Hip/proximal femur (intertrochanteric, femoral neck, subtrochanteric)

- 5.2.2 Vertebral compression fractures (thoracic/lumbar)

- 5.2.3 Distal radius (Colles/Smith)

- 5.2.4 Proximal humerus

- 5.2.5 Pelvic ring & acetabular fractures in elderly

- 5.2.6 Proximal tibia

- 5.2.7 Ankle fractures

- 5.3 By Material

- 5.3.1 Titanium & Ti alloys

- 5.3.2 Stainless steel

- 5.3.3 Cobalt-chromium alloys

- 5.3.4 Bioabsorbable polymers (PLLA/PGA)

- 5.3.5 PEEK & carbon fiber-reinforced polymers

- 5.3.6 PMMA bone cement

- 5.3.7 Calcium phosphate/Calcium sulphate cements

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers (ASCs)

- 5.4.3 Other End Users (Specialty orthopedic & spine centers)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 aap Implantate AG

- 6.3.2 Acumed (Colson Medical)

- 6.3.3 B. Braun (Aesculap)

- 6.3.4 Bioretec

- 6.3.5 CarboFix (Carboclear)

- 6.3.6 Double Medical (China)

- 6.3.7 G21 S.r.l.

- 6.3.8 Globus Medical

- 6.3.9 Johnson & Johnson

- 6.3.10 Medartis AG

- 6.3.11 Medtronic Plc

- 6.3.12 Merit Medical (DFINE StabiliT)

- 6.3.13 Orthofix

- 6.3.14 OSSIO

- 6.3.15 Paragon 28

- 6.3.16 Smith+Nephew

- 6.3.17 Stryker Corporation

- 6.3.18 Tecres S.p.A.

- 6.3.19 Teknimed

- 6.3.20 Waston Medical

- 6.3.21 Weigao Orthopaedic

- 6.3.22 Zimmer Biomet Holdings, Inc

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment