PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063552

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063552

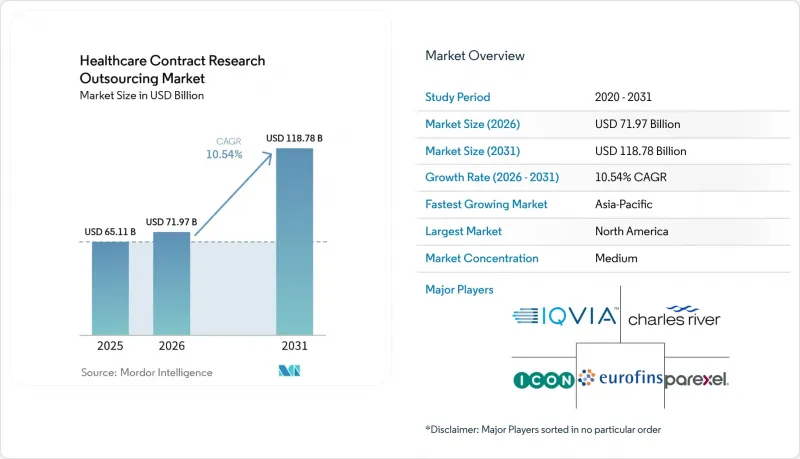

Healthcare Contract Research Outsourcing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the healthcare contract research outsourcing market size is expected to increase from USD 65.11 billion in 2025 to USD 71.97 billion in 2026 and reach USD 118.78 billion by 2031, growing at a CAGR of 10.54% over 2026-2031.

The Healthcare Contract Research Outsourcing Market is Service Type (Clinical Trial Services (Phase I-IV), Regulatory Services, Clinical Data Management, and More), Type (Drug Discovery, Pre-Clinical Research, and Clinical Research), End User (Pharmaceutical Companies, Biotechnology Companies, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasted in Terms of Value (USD).

Global Healthcare Contract Research Outsourcing Market Trends and Insights

Rising Biopharma R&D Investments and Pipeline Intensity

Novel drug approvals across leading regulators in 2025 confirm continued sponsor focus on specialized indications where clinical complexity and regulatory scrutiny require strong development partners. A higher share of orphan-designated therapies within the annual approval mix points to sustained emphasis on targeted patient populations, which raises the need for protocol designs that maximize data yield per subject and accelerate demand for outsourced biostatistics and site operations. Continuous platform-style studies in oncology and other complex areas favor CRO partners that can stand up governance structures and adaptive analytics across multi-arm frameworks rather than isolated single-protocol engagements. Sponsors increasingly rely on embedded statistical and data science capacity to segment subpopulations, align endpoints to regulatory expectations, and streamline submission pathways, which strengthens program-level outsourcing relationships. As larger providers integrate real-world data and technology capabilities into research solutions, they extend support from early evidence development to late-phase outcomes research, reinforcing the outsourcing value proposition across the asset lifecycle.

Cost Pressure and Speed-To-Market Imperatives Drive Externalization

Sponsors under budget constraints balance time-to-data with predictable resourcing, leading many to expand functional service provider models that embed teams within sponsor systems while preserving accountability for delivery quality. Backlog visibility and near-term conversion at large players indicate that staged commitments and flexible contracting are now a standard approach to manage portfolio risk and to match spend to milestone attainment.AI-enabled contracting and study start-up tools flag document misalignments early and reduce reconciliation cycles, shrinking activation timelines that often impede first patient. Site intelligence platforms now index hundreds of thousands of institutions and millions of study sites across dozens of countries, which strengthens feasibility accuracy and lifts enrollment performance when sponsors prioritize speed. These operational gains help sponsors compress decision gates and direct investment to the most promising programs, creating a reinforcing cycle for the healthcare contract research outsourcing market as timelines and cost per data point improve.

Regulatory Divergence and CTR/GCP Tightening Across Regions

Evolving GCP guidance places stronger emphasis on risk-based quality management and continuous quality improvement, which requires CROs and sponsors to upgrade SOPs, retrain teams, and adapt monitoring models to centralized analytics and clear traceability of risk decisions. Sponsors are expected to demonstrate why and how particular risks were prioritized, including the evidence and thresholds applied, which increases documentation workloads for protocol teams and vendor oversight groups. Functional teams must realign data flows and audit trails to ensure that remote monitoring, eConsent, and sensor-derived data remain inspection-ready, which can extend transition timelines during multi-country study execution. To address this, many sponsors strengthen embedded partnerships where CROs manage regulatory intelligence and training programs that keep global studies on a consistent quality baseline. These adjustments create near-term drag but support longer-term efficiency gains once standardized analytics, documentation, and RBQM platforms are in place, which steadies compliance across a diversified study portfolio.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Clinical Trial Complexity

- Preference for Specialized Full-Service and FSP Models

- Data Security, IP Protection, and Vendor Governance Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Clinical trial services (Phase I-IV) captured 62.34% of the healthcare contract research outsourcing market in 2025, while clinical data management is set to grow fastest at a 12.56% CAGR through 2031 as real-time capture and centralized analytics become standard practice. Functional teams focused on data curation, edit checks, and anomaly detection are embedded earlier in the workflow to support risk-based quality management and drive predictable database lock performance under evolving GCP guidance. Providers with site intelligence platforms help sponsors improve screening and enrollment by targeting institutions with proven infrastructure for telehealth, ePRO, imaging, and cardiology endpoints, which reduces screen failure and accelerates milestone attainment. As AI support extends from feasibility to medical writing and data cleaning, large providers maintain margin stability even as protocol demands rise, which sustains investment in analytics capabilities within research delivery units. Study start-up is another focal area, with contract and budget automation reducing administrative latency that often slows first patient in and creates cost risk for sponsors.

Clinical data management gains momentum as sponsors standardize data flows across decentralized components, imaging, and specialty labs, which increases the need for harmonized dictionaries, reusable edit checks, and real-time dashboards. Vendors expand biometrics and programming hubs to address these needs; this evolution is visible in regional capacity investments that bring statistical programming and clinical data operations closer to multinational study footprints. As real-world evidence and late-phase work move closer to clinical operations, sponsors increasingly look for integrated solutions that manage observational cohorts, registries, and safety follow-up under one governance umbrella. The cumulative effect is a service mix where high-volume Phase I-IV activity anchors demand, while data-centric functions command premium growth on the back of RBQM, decentralized elements, and expanding endpoint complexity.

Geography Analysis

North America accounted for 37.23% of the healthcare contract research outsourcing market in 2025, supported by extensive investigator networks, mature site infrastructure, and a large base of sponsors. Strong vendor presence in the United States ensures access to full-service and FSP models along with advanced data platforms that align to updated GCP expectations on documentation and centralized monitoring. Study start-up and contract optimization capabilities further enhance execution speed across this region, as AI-powered checks reduce friction in agreements with sites and vendors. As large providers integrate obesity, cardiometabolic, and real-world evidence collaborations into research offerings, the region benefits from scaled infrastructure that supports late-phase and outcomes studies alongside pivotal trials. These features sustain North America's anchor role in the healthcare contract research outsourcing market even as sponsors diversify trial footprints globally.

Asia-Pacific is the fastest-growing region with a projected 15.83% CAGR through 2031, reflecting the rapid buildout of clinical infrastructure and strategic collaborations that expand early-phase capacity. Partnerships that link university health systems with global CRO capabilities give sponsors efficient access to large patient bases and integrated clinical ecosystems, which are vital for first-in-human and dose-ranging studies. Regional platform and modality specialists continue to scale capabilities in biologics and complex modalities, which increases outsourcing options for sponsors seeking APAC patient access with high-quality analytics and manufacturing integration. As integrated discovery-to-manufacturing pipelines mature in the region, sponsors can align pre-clinical and clinical supply chains with study timelines, supporting faster program progression and reinforcing the healthcare contract research outsourcing market in APAC.

European expansions by CROs increase access to specialized early-phase and biometrics capabilities, which helps sponsors balance regulatory and operational needs across the continent. Oncology-focused providers with embedded FSP capacity continue to build on regional strengths in precision medicine, where complex master protocols and biomarker-driven cohorts demand strong governance and analytics. As centralized monitoring and RBQM-based oversight are standardized in European operations, vendors with validated processes and training programs gain selection advantages, strengthening contributions to the healthcare contract research outsourcing market.

- Allucent Inc.

- Caidya Inc.

- Charles River

- CMIC Holdings Co., Ltd.

- CTI Clinical Trial & Consulting Services, Inc.

- EPS Holdings, Inc.

- Eurofins

- Fortrea Holdings Inc.

- Hangzhou Tigermed Consulting Co., Ltd.

- ICON

- IQVIA

- Linical Co., Ltd.

- Medpace Holdings, Inc.

- Novotech

- Parexel International

- Pharmaron Beijing Co., Ltd.

- Premier Research International LLC

- PSI CRO

- SGS Life Sciences

- Syneos Health

- Thermo Fisher Scientific (PPD Clinical Research)

- Worldwide Clinical Trials, LLC

- WuXi AppTec Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Biopharma R&D Investments and Pipeline Intensity

- 4.2.2 Cost Pressure and Speed-To-Market Imperatives Drive Externalization

- 4.2.3 Increasing Clinical Trial Complexity

- 4.2.4 Preference for Specialized Full-Service and FSP Models

- 4.2.5 Expansion of Platform/Master Protocols Elevates Program-Level CRO Demand

- 4.2.6 AI-Enabled Protocol, Site, and RBQM Optimization Expands Data/Tech-Led CRO Revenue

- 4.3 Market Restraints

- 4.3.1 Regulatory Divergence and CTR/GCP Tightening Across Regions

- 4.3.2 Data Security, IP Protection, and Vendor Governance Risks

- 4.3.3 Geopolitical/Biosecurity Scrutiny Reshapes China-Linked Vendor Risk

- 4.3.4 Site Workforce Shortages and Investigator Burnout Extend Timelines

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service Type

- 5.1.1 Clinical Trial Services (Phase I-IV)

- 5.1.2 Regulatory Services

- 5.1.3 Clinical Data Management

- 5.1.4 Pharmacovigilance

- 5.1.5 Site Management & Monitoring

- 5.1.6 Central Lab & Bioanalytical Services

- 5.1.7 Real World Evidence & Late Phase

- 5.1.8 Others

- 5.2 By Type

- 5.2.1 Drug Discovery

- 5.2.2 Pre-clinical Research

- 5.2.3 Clinical Research

- 5.3 By End User

- 5.3.1 Pharmaceutical Companies

- 5.3.2 Biotechnology Companies

- 5.3.3 Medical Device Companies

- 5.3.4 Academic & Research Institutes

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Allucent Inc.

- 6.3.2 Caidya Inc.

- 6.3.3 Charles River Laboratories International, Inc.

- 6.3.4 CMIC Holdings Co., Ltd.

- 6.3.5 CTI Clinical Trial & Consulting Services, Inc.

- 6.3.6 EPS Holdings, Inc.

- 6.3.7 Eurofins Scientific

- 6.3.8 Fortrea Holdings Inc.

- 6.3.9 Hangzhou Tigermed Consulting Co., Ltd.

- 6.3.10 ICON plc

- 6.3.11 IQVIA Holdings Inc.

- 6.3.12 Linical Co., Ltd.

- 6.3.13 Medpace Holdings, Inc.

- 6.3.14 Novotech

- 6.3.15 Parexel International Corporation

- 6.3.16 Pharmaron Beijing Co., Ltd.

- 6.3.17 Premier Research International LLC

- 6.3.18 PSI CRO AG

- 6.3.19 SGS Life Sciences

- 6.3.20 Syneos Health, Inc.

- 6.3.21 Thermo Fisher Scientific (PPD Clinical Research)

- 6.3.22 Worldwide Clinical Trials, LLC

- 6.3.23 WuXi AppTec Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment