PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063563

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063563

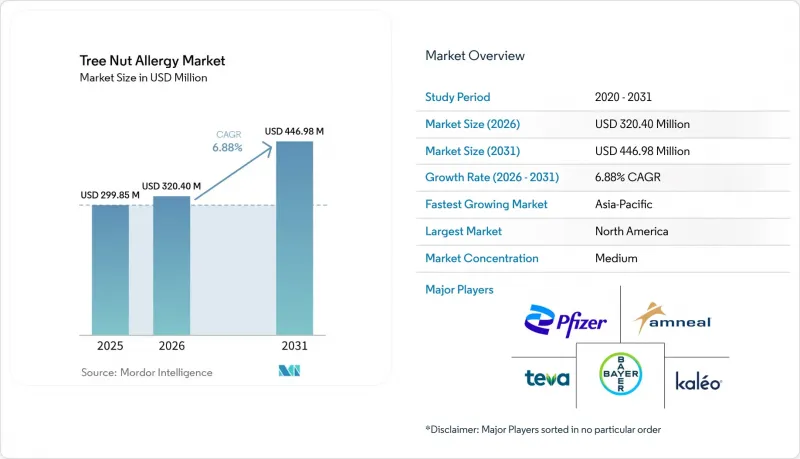

Tree Nut Allergy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the tree nut allergy market size is projected to expand from USD 299.85 million in 2025 and USD 320.40 million in 2026 to USD 446.98 million by 2031, registering a CAGR of 6.88% between 2026 to 2031.

This report is Segmented by Product Type (Acute Care Drugs, Disease-Modifying Therapies, Diagnostics), Tree Nut Type (Walnut, Cashew, Almond, Hazelnut, and More), End User (Hospital Pharmacies, Retail Pharmacies, and More), Age Group (Paediatric, Adult, Geriatric), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Tree Nut Allergy Market Trends and Insights

Rising Pediatric Prevalence of IgE-Mediated Tree-Nut Allergy

A 2024 Turkish cohort reported that 60% of newly diagnosed tree-nut allergic children experienced multi-system reactions requiring epinephrine. Additionally, a 2025 European registry identified hazelnut, walnut, and cashew as the cause of 73% of pediatric anaphylaxis cases across Germany, France, and Italy. The POSEIDON Phase 3 trial demonstrated a 68.4% desensitization rate to 1,000 mg of peanut protein in children aged 1-4 years, highlighting the significance of early-life intervention. Furthermore, real-world data from France associated sublingual immunotherapy with a 38% reduction in asthma risk, reinforcing its preventive potential.

Accelerated Approvals of Disease-Modifying Immunotherapies (OIT, SLIT, EPIT)

In 2026, DBV Technologies submitted a Biologics License Application following positive VITESSE Phase 3 results, which demonstrated significant desensitization in children aged 4-7 years. In February 2024, Omalizumab became the first anti-IgE therapy approved for multiple food allergies, driving a shift in treatment guidelines toward the integration of biologics. Additionally, ALK-Abello's successful peanut-tablet Phase 2 results in April 2026 indicated further diversification in administration methods.

High Costs & Limited Reimbursement Hurdles for Biologic Therapies

Omalizumab, a leading biologic therapy, is priced at over USD 2,000 per month. U.S. payers enforce prior-authorization requirements, including the submission of serum-IgE documentation and prescriptions from allergists. Medicare Part D beneficiaries face coinsurance rates of 25-33%, resulting in monthly out-of-pocket expenses ranging from USD 500 to 700. By 2025, 14 state Medicaid plans are expected to mandate step therapy through oral immunotherapy before approving biologics, potentially restricting access for low-income families.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Component-Resolved Diagnostics in Clinical Practice

- Launch of Smart, Connected Epinephrine Autoinjectors with Adherence Analytics

- Safety Concerns & Adherence Issues with Extended Immunotherapy Protocols

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acute-care drugs, including epinephrine autoinjectors, antihistamines, and corticosteroids, accounted for 42.50% of 2025 revenue, highlighting their critical role in emergency management. The demand for epinephrine has been strengthened by the introduction of infant-dose products and affordable generics. However, disease-modifying agents, led by oral immunotherapy and omalizumab, are growing at an 8.88% CAGR, shifting the clinical focus from emergency interventions to preventive care. Guidelines emphasize that biologics are preventive in nature and should not replace epinephrine in acute situations.

Walnuts captured 28.55% of the 2025 segment revenue, reflecting their widespread use in baked goods and plant-based milks. Hazelnut oral immunotherapy achieved a high desensitization rate but provided minimal cross-protection to other nuts, underscoring the need for nut-specific treatment approaches. Rising cashew consumption in Asia is driving a 6.99% CAGR, with increasing demand for cashew-specific allergy treatments as exposure grows.

Geography Analysis

In 2025, North America secured 39.67% of the geographic revenue, driven by the United States' rapid adoption of omalizumab following its FDA approval in February 2024. This growth was supported by the widespread availability of epinephrine auto-injectors through retail and specialty pharmacies and a well-established network of allergy clinics providing Oral Immunotherapy (OIT). In January 2025, the American Academy of Allergy, Asthma & Immunology issued consensus guidance on omalizumab, standardizing patient selection criteria and dosing regimens. Additionally, the 2024 AAAAI-EAACI PRACTALL update aligned oral food challenge protocols, reducing variability across centers and facilitating multi-site clinical trials. Europe, accounting for approximately 28% of the market in 2025, saw Germany, the United Kingdom, France, Italy, and Spain leading in OIT adoption. However, a regulatory gap emerged as the European Medicines Agency's Committee for The EAACI 2024 guidelines recommended omalizumab and OIT for peanut allergies but highlighted limited evidence for tree nuts, which slowed reimbursement and broader adoption.

Asia-Pacific, experiencing a 7.90% CAGR through 2031, is driven by dietary westernization, which has increased tree nut consumption and sensitization rates. A 2025 study documented that eliciting doses for walnut and cashew in Japanese children are now approaching Western thresholds, attributed to rising nut consumption over the past decade. Additionally, China's tree nut import volume grew significantly between 2015 and 2024. The Middle East and Africa, led by Gulf Cooperation Council countries and South Africa, along with South America, anchored by Brazil and Argentina, collectively represent approximately 10% of the market. Growth in these regions is constrained by a limited number of specialists, low awareness of immunotherapy, and high out-of-pocket costs for biologics and diagnostics. However, urbanization and rising incomes are expected to narrow these gaps over the forecast period.

- Abbvie

- Aimmune Therapeutics (Nestle Health Science)

- ALK-Abello

- Amneal Pharmaceuticals

- Amphastar Pharmaceuticals

- AstraZeneca

- Bayer

- Cipla

- DBV Technologies

- Dr. Reddy's Laboratories

- Eli Lilly and Company

- GlaxoSmithKline

- Johnson & Johnson

- Kaleo, Inc.

- Novartis

- Perrigo Company

- Pfizer

- Regeneron Pharmaceuticals

- Roche

- Sanofi

- Stallergenes Greer

- Sun Pharmaceuticals Industries

- Takeda Pharmaceuticals

- Teva Pharmaceutical Industries

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Pediatric Prevalence of IgE-Mediated Tree-Nut Allergy

- 4.2.2 Accelerated Approvals of Disease-Modifying Immunotherapies (OIT, SLIT, EPIT)

- 4.2.3 Expansion of Component-Resolved Diagnostics (CRD) in Clinical Practice

- 4.2.4 Launch of Smart, Connected Epinephrine Autoinjectors with Adherence Analytics

- 4.2.5 Surging Venture Capital Into AI-Enabled Precision-Allergy Platforms

- 4.2.6 Westernization of Asian Diets Increasing Nut Exposure

- 4.3 Market Restraints

- 4.3.1 High Cost & Limited Reimbursement for Biologic Therapies

- 4.3.2 Safety & Adherence Challenges with Multi-Year Immunotherapy Protocols

- 4.3.3 Frequent Shortages in Global Epinephrine Auto-Injector Supply Chain

- 4.3.4 Lack of Harmonised Treatment Guidelines Across Regions & Centers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Supplier Power

- 4.7.2 Buyer Power

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Acute Care Drugs

- 5.1.1.1 Epinephrine Auto-Injectors

- 5.1.1.2 Antihistamines

- 5.1.1.3 Corticosteroids

- 5.1.2 Disease-Modifying Therapies

- 5.1.2.1 Oral Immunotherapy (OIT)

- 5.1.2.2 Sublingual Immunotherapy (SLIT)

- 5.1.2.3 Epicutaneous Immunotherapy (EPIT)

- 5.1.2.4 Biologic Monoclonal Antibodies (Anti-IgE, Anti-IL-4/13)

- 5.1.3 Diagnostics

- 5.1.3.1 Skin Prick Tests

- 5.1.3.2 Serum-specific IgE Tests

- 5.1.3.3 Component-Resolved Diagnostics (CRD)

- 5.1.3.4 At-home Digital Test Kits

- 5.1.1 Acute Care Drugs

- 5.2 By Tree Nut Type

- 5.2.1 Walnut

- 5.2.2 Cashew

- 5.2.3 Almond

- 5.2.4 Hazelnut

- 5.2.5 Pecan

- 5.2.6 Pistachio

- 5.2.7 Macadamia

- 5.2.8 Brazil Nut

- 5.2.9 Others (e.g., Chestnut, Pine Nut)

- 5.3 By End User

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 Specialty Allergy Clinics

- 5.3.4 Homecare / Direct-to-Patient

- 5.4 By Age Group

- 5.4.1 Paediatric (<18 yrs)

- 5.4.2 Adult (18-64 yrs)

- 5.4.3 Geriatric (>65 yrs)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Aimmune Therapeutics (Nestle Health Science)

- 6.3.3 ALK-Abello

- 6.3.4 Amneal Pharmaceuticals

- 6.3.5 Amphastar Pharmaceuticals

- 6.3.6 AstraZeneca plc

- 6.3.7 Bayer AG

- 6.3.8 Cipla Ltd.

- 6.3.9 DBV Technologies

- 6.3.10 Dr. Reddy's Laboratories

- 6.3.11 Eli Lilly and Company

- 6.3.12 GlaxoSmithKline plc

- 6.3.13 Johnson & Johnson

- 6.3.14 Kaleo, Inc.

- 6.3.15 Novartis AG

- 6.3.16 Perrigo Company plc

- 6.3.17 Pfizer Inc.

- 6.3.18 Regeneron Pharmaceuticals, Inc.

- 6.3.19 Roche Holding AG

- 6.3.20 Sanofi S.A.

- 6.3.21 Stallergenes Greer

- 6.3.22 Sun Pharmaceutical Industries Ltd.

- 6.3.23 Takeda Pharmaceutical Company Limited

- 6.3.24 Teva Pharmaceutical Industries Ltd.

- 6.3.25 Viatris Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment