PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063578

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063578

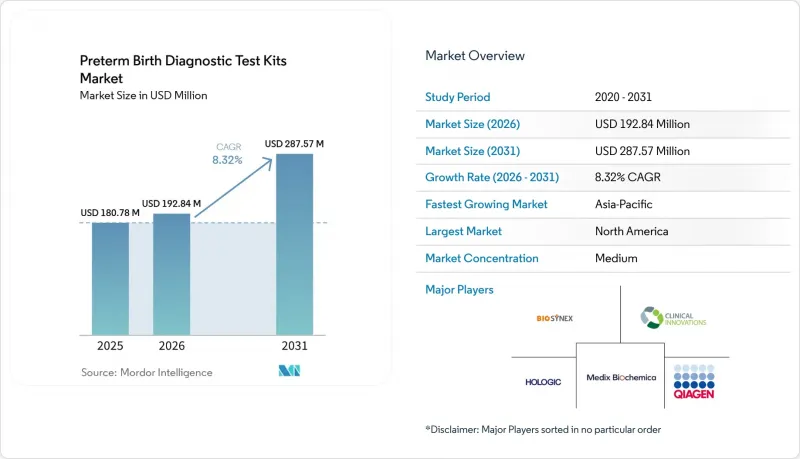

Preterm Birth Diagnostic Test Kits - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the preterm birth diagnostic test kits market size is projected to be USD 180.78 million in 2025, USD 192.84 million in 2026, and reach USD 287.57 million by 2031, growing at a CAGR of 8.32% from 2026 to 2031.

This report is Segmented by Product Type (Fetal Fibronectin, and More), Material (Vaginal/Cervical Swab, Blood), End User (Hospitals & Maternity Centers, Diagnostic Laboratories, Birthing Centers/Outpatient OB-GYN Clinics, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Preterm Birth Diagnostic Test Kits Market Trends and Insights

Rising Global Incidence and Burden of Preterm Births

Preterm birth remains a leading cause of neonatal morbidity and mortality worldwide, which sustains clinical demand for earlier and more accurate risk assessment. Hospitals seek to standardize triage to limit unnecessary transfers and to support timely corticosteroid use only when risk is credible and near term. Persistent burden in low-resource settings exposes a gap between need and access, which sustains use of simpler tests and delays adoption of advanced biomarker assays. Health systems weigh the operational value of tests that can quickly rule out imminent delivery, preventing avoidable hospital stays and reducing strain on tertiary units. These dynamics keep the preterm birth diagnostic test kits market focused on speed and clarity of result to strengthen frontline decisions.

Integration of Biomarker-Based Triage in Clinical Pathways (fFN, PAMG-1, IGFBP-1)

Many institutions in North America and Europe have integrated biomarker-based triage into standardized protocols for patients with symptoms between 24 and 34 weeks, reducing unwarranted admissions when a clear negative result is returned. The discontinuation of quantitative fetal fibronectin cassettes prompted national guidance in 2024 to transition to alternative platforms, which reshaped procurement and encouraged broader evaluation of IGFBP-1 and PAMG-1 options. The role of ROM diagnostics persists as part of the care pathway, since membrane status directly influences near-term labor risk and clinical surveillance choices. Protocol-driven triage limits variation among clinicians and channels resources to cases with measurable risk rather than precautionary observation. Professional guidance and institutional committees continue to shape uptake, anchoring the preterm birth diagnostic test kits market to tests that deliver binary or near-binary clarity within minutes.

Mixed/Conditional Guideline Endorsements for Some Biomarkers and Uses

Guideline variability across regions slows standardized adoption and sustains a patchwork of testing practices within and across countries. Professional documents often reference biomarker classes rather than specific brands, which leaves procurement teams to decide based on price, availability, and local familiarity. Inconsistent endorsement for use cases such as asymptomatic screening contributes to uneven uptake outside tertiary centers. Clinicians also face divergent payer rules on which tests are reimbursed in specific scenarios, which adds friction to routine ordering. These factors temper the pace at which the preterm birth diagnostic test kits market can move from pilot usage to stable, protocol-driven deployment.

Other drivers and restraints analyzed in the detailed report include:

- Rapid, Point-of-Care Lateral-Flow Kits Enabling Fast Rule-Out Decisions in Maternity Triage

- Hospital-Protocol and Reimbursement Support for Targeted Testing in High-Risk/Symptomatic Cases

- EU IVDR Elevates Clinical Evidence, Cost, and Time-to-Market for IVDs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fetal fibronectin accounted for 43.89% share of the preterm birth diagnostic test kits market size in 2025, reflecting legacy entrenchment before a supply shift changed ordering behavior. The discontinuation of quantitative fFN cassettes in 2024 replaced the quantitative standard with qualitative and alternative biomarkers within many hospital pathways. PAMG-1 platforms are projected to grow at a 9.67% CAGR through 2031 as hospitals adopt binary rule-out formats that streamline triage decisions for symptomatic women. ROM diagnostics remain a complementary pillar in the pathway because confirming membrane status substantially influences near-term risk management. The preterm birth diagnostic test kits market is also redefining timing as proteomic blood tests, led by PreTRM, focus on risk at 18 to 20 weeks with a prevention strategy built around progesterone, aspirin, and intensified care navigation. Randomized evidence reported in 2026 showed a reduction in very early preterm births and fewer newborn complications when PreTRM screening was paired with targeted interventions. These shifts move the center of gravity upstream from crisis management at 24 to 34 weeks to earlier risk stratification that may avert high-cost episodes. Hospitals still value actionable negative predictive value to avoid transfers, while laboratories emphasize centralized workflows for complex assays. Together, these product dynamics sustain a two-speed market in which rapid swab kits support acute triage and blood proteomics expands into preventive care.

The product mix reflects clear operational trade-offs that shape buyer preferences. Point-of-care swabs that return results within minutes fit emergency and observation units that need immediate clarity for rule-out decisions. PAMG-1 and IGFBP-1 options compete on price, availability, and local guideline familiarity as procurement teams seek reliable supply after fFN disruptions. Blood-based proteomic assays require centralized processing but open a new prevention play that targets the many spontaneous preterm births that lack traditional risk flags. The preterm birth diagnostic test kits market, therefore, aligns products to clinical timing, with symptomatic triage anchored by lateral-flow kits and asymptomatic risk addressed by proteomic tests that influence care plans weeks before symptoms appear. This complementary positioning helps vendors defend against price-only competition by linking tests to outcomes and budget impact.

Geography Analysis

North America held 43.64% of 2025 revenue and anchors the preterm birth diagnostic test kits market with protocols that embed biomarker use in labor and delivery units. The 2024 discontinuation of quantitative fFN drove expedited transitions to alternative biomarkers and reinforced the weight of national guidance in shaping practice. Canada and Mexico trail U.S. adoption as procurement and coverage rules vary across provinces and payer mixes. U.S. growth now includes asymptomatic screening pilots under commercial plans and Medicaid, which nudges adoption beyond crisis triage toward prevention. The preterm birth diagnostic test kits market in North America continues to balance rapid swab usage with emerging proteomic workflows that can demonstrate measurable outcomes.

Asia-Pacific is projected to grow at a 9.45% CAGR through 2031 as laboratories scale in China, India, and South Korea and as public pilots examine coverage for newer assays. Domestic manufacturing and price-sensitive tenders influence swab adoption in public networks, while private hospital chains concentrate on PAMG-1 and IGFBP-1 in urban centers. Japan's declining birth rate and a constrained obstetric workforce temper demand growth, yet targeted adoption persists in tertiary centers. In Australia, clinical groups monitored implications of fFN supply changes on rural transfer practices and sought consistent alternatives to preserve triage confidence. Across Southeast Asia, limited cold-chain and fragmented regulatory pathways slow uptake of novel biomarkers, which keeps the preterm birth diagnostic test kits market anchored to affordable and robust options.

Europe maintained share as institutions navigated evolving regulatory expectations and deadlines for IVD compliance. Germany, France, and the United Kingdom embed biomarker testing in maternity pathways, though budget evaluations can slow inclusion on national reimbursement schedules. The 2024 shift in the United Kingdom toward alternative triage tests after the fFN discontinuation highlighted public-sector cost sensitivity and the central role of national guidance. Southern and Eastern Europe exhibit uneven adoption due to regionalized health administration and lower per-capita spend, which sustains reliance on clinical judgment and older tests in some settings. The preterm birth diagnostic test kits market in Europe increasingly rewards vendors that can meet documentation and post-market needs without interrupting supply.

The Middle East and Africa show nascent growth with private hospitals in the Gulf importing Western biomarker platforms and tertiary centers in South Africa using diagnostics selectively. Sub-Saharan Africa bears a high preterm burden but faces infrastructure constraints that limit test usage to urban hubs. Programmatic efforts continue to target related complications such as preeclampsia, where new rapid tests under development seek to broaden access in lower-resource settings. South America's private sectors in Brazil and Argentina support adoption in urban clinics, while public systems face budget pressures that moderate scale. These regional factors keep the preterm birth diagnostic test kits market growth tied to procurement sophistication, laboratory capacity, and payer willingness to link tests to measurable outcomes.

- BIOSYNEX S.A.

- CiTest Diagnostics

- Healgen Scientific LLC

- Hologic

- Laborie Medical Technologies (Clinical Innovations)

- Medix Biochemica (Actim)

- Nanjing Liming Bio

- NX Prenatal Inc.

- Pro-Lab Diagnostics

- QIAGEN

- Sera Prognostics, Inc.

- Vitrosens Biotechnology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising global incidence and burden of preterm births

- 4.2.2 Integration of biomarker-based triage in clinical pathways (fFN, PAMG-1, IGFBP-1)

- 4.2.3 Rapid, point-of-care lateral-flow kits enabling fast rule-out decisions in maternity triage

- 4.2.4 Hospital-protocol and reimbursement support for targeted testing in high-risk/symptomatic cases

- 4.2.5 Expansion of blood-based proteomic risk tests informing earlier care pathways

- 4.2.6 Digital decision tools combining quantitative biomarkers with cervical length

- 4.3 Market Restraints

- 4.3.1 Mixed/conditional guideline endorsements for some biomarkers and uses

- 4.3.2 Modest PPV/false positives necessitating confirmatory assessment

- 4.3.3 Operational sampling constraints (timing, co-interference) limit universal deployment

- 4.3.4 EU IVDR elevates clinical evidence, cost, and time-to-market for IVDs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Fetal Fibronectin

- 5.1.2 PAMG-1-based

- 5.1.3 IGFBP-1-based

- 5.1.4 Dual-marker ROM tests

- 5.1.5 Blood-based proteomic risk tests

- 5.2 By Material

- 5.2.1 Vaginal/Cervical swab

- 5.2.2 Blood

- 5.3 By End User

- 5.3.1 Hospitals & Maternity Centers

- 5.3.2 Diagnostic Laboratories

- 5.3.3 Birthing Centers / Outpatient OB-GYN Clinics

- 5.3.4 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 BIOSYNEX S.A.

- 6.3.2 CiTest Diagnostics

- 6.3.3 Healgen Scientific LLC

- 6.3.4 Hologic, Inc.

- 6.3.5 Laborie Medical Technologies (Clinical Innovations)

- 6.3.6 Medix Biochemica (Actim)

- 6.3.7 Nanjing Liming Bio

- 6.3.8 NX Prenatal Inc.

- 6.3.9 Pro-Lab Diagnostics

- 6.3.10 QIAGEN N.V.

- 6.3.11 Sera Prognostics, Inc.

- 6.3.12 Vitrosens Biotechnology

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment