PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063582

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063582

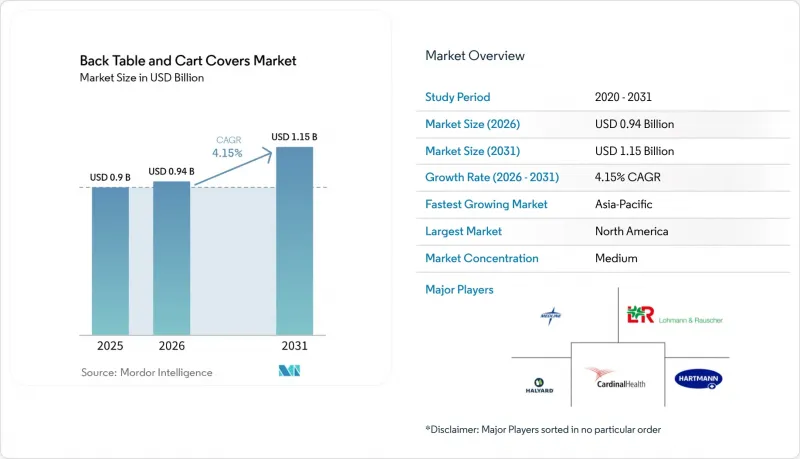

Back Table And Cart Covers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the back table and cart covers market size is expected to grow from USD 0.9 billion in 2025 to USD 0.94 billion in 2026 and is forecast to reach USD 1.15 billion by 2031 at 4.15% CAGR over 2026-2031.

This report is Segmented by Product Type (Back Table Covers, Cart Covers), Sterility (Sterile, Non-Sterile), Material (SMS/PP Nonwoven, PE Film-Laminate, Spunlace/Rayon, Reusable Textile), End User (Hospitals, Ascs, Specialty Clinics), Distribution Channel (Direct Tenders/GPO, Distributor, Online), and Geography (North America, Europe, and More). Market Forecasts are in Value (USD).

Global Back Table And Cart Covers Market Trends and Insights

Stricter Sterile-Field Protocols and Table-Cover Use in OR Workflows Post-2019 Guideline Updates

Hospitals and surgical centers are prioritizing barrier performance and packaging integrity in all sterile-field components, which is tightening specifications for back table and cart covers. European facilities are aligning to EN 13795 classifications, which codify standard and high-performance drape requirements and drive procurement toward products that demonstrate repeatable liquid barrier and microbiological protection. EU MDR 2017/745 has also accelerated stock refresh cycles as legacy inventory certified under older frameworks must be retired and replaced with MDR-conformant supplies. These dynamics elevate preference for validated sterile-pack configurations and standardized cover systems that simplify evidence collection for audits and clinical governance reviews. In fluid-intensive service lines, product selection is gravitating to higher-grade barriers and robust tensile performance profiles that maintain integrity over multi-hour procedures and repeated instrument transfers. Together, these trends are reinforcing premium performance tiers within the back table and cart covers market and concentrating spend with suppliers that can document compliance across international standards.

Rising Outpatient or ASC Surgical Procedure Volumes Shifting Barrier Product Demand to High-Turnover Settings

Procedure migration to ambulatory and office-based settings is rebalancing demand toward single-use cover solutions that enable quick room flips and reduce the need for complex reprocessing workflows. Facilities operating high-throughput schedules favor preconfigured carts and back table draping that keep equipment protected during transit and minimize touchpoints that could compromise sterility. As outpatient capacity expands, procurement teams are adopting digital marketplaces and direct-to-facility channels that streamline replenishment and shorten lead times for standardized barrier components. These channels also make it simpler to filter products by documentation requirements and quality management certifications when small teams manage purchasing alongside clinical tasks. Manufacturers that offer sterile cover packs designed for compact OR footprints and focused specialty workflows are well positioned to capture growth in these settings. This shift supports steady volume gains for disposable cover formats while pushing suppliers to provide reliable availability and elastic capacity for episodic surges.

Environmental Pressure Favoring Reusables or Lower-Footprint Alternatives to Single-Use Covers

Extended Producer Responsibility policies are shaping purchasing strategies by adding per-unit cost signals to disposable textiles and setting the stage for broader lifecycle accounting. In the United States, California's SB 707 established a statewide textile EPR framework that directly affects how hospitals evaluate single-use versus reusable pathways across defined product categories. Suppliers are responding with lighter-weight mono-material designs and bio-based content to reduce waste and align with health system sustainability targets. Large drape and pack providers now publish sustainability roadmaps and product-level documentation that address recycled or renewable content and greenhouse gas reduction. This evidence base supports hospital initiatives to balance clinical performance, logistics efficiency, and environmental impacts in operating room supply decisions. Over the forecast period, EPR implementation milestones and hospital climate-action commitments will continue to influence design direction and refresh timing for back table and cart cover portfolios.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Custom Procedure Packs that Include Back Table and Instrument Table Covers

- Higher Penetration of Nonwoven SMS or Laminate Barrier Materials in Surgical Drapes and Covers

- Polypropylene or Nonwoven Raw-Material Price And Availability Volatility Impacting Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Back table covers held 62.19% in 2025 and remain foundational as facilities standardize sterile-field setup across general surgery, orthopedics, and cardiac programs. Cart covers are the fastest-growing product at a 6.45% CAGR through 2031, supported by pre-set sterile carts that move directly into operating rooms and reduce setup steps that can stretch room reset times. The back table and cart covers market benefits from this operational focus because streamlined draping lowers preparation variability and helps smaller teams sustain throughput during peak schedules. In settings that run compact rooms and rely on predictable case sequences, the appeal of dedicated cart covers is rising along with pre-bundled pack usage. Product specifications continue to converge toward international drape norms, and purchasing committees prioritize solutions with validated barrier and tensile ratings aligned to surgical risk categories.

As tendering cycles proceed, hospitals balance the unit price of single-use cart covers with the staffing and logistics savings associated with faster room flips. Product decisions also factor storage convenience, packaging integrity, and compatibility with sterile-pack programs that include related components. Suppliers that offer cart covers optimized for high-fluid specialties retain an edge when case mix demands higher-grade barrier performance. Regional sourcing strategies use laminate-backed or spunbond-heavy designs to meet diverse budgets and standards without complicating inventory. The back table and cart covers market size for cart covers is projected to expand in line with standardized turnover initiatives that favor preconfigured barrier solutions across ambulatory and inpatient sites.

Sterile back table and cart covers accounted for 65.89% in 2025 and lead growth at a 6.85% CAGR over the forecast period. This outcome reflects hospitals' zero-tolerance approach to contamination risk in direct patient-contact zones and the administrative need for lot traceability. Non-sterile covers continue to address preparatory and transport tasks where immediate patient exposure is not present, which provides a cost lever during budget-constrained cycles. Clinical governance trends support sterile products for high-acuity procedures and encourage systematic documentation across draping and sterile barrier workflows. In markets where facility licensing references medical device classifications, sterile cover variants align with stricter oversight and structured conformity assessment steps under standard frameworks.

As EPR policies scale and lifecycle costs face scrutiny, procurement teams may evaluate partial shifts to reusable sterile textiles for select high-volume procedures. The policy direction in California is notable because it applies per-unit costs to covered single-use textiles while positioning reusables differently under the program's fee structure. Product roadmaps from leading vendors show investment in packaging and materials aimed at lighter designs and renewable content, an approach that lowers disposal volumes and strengthens the clinical-economic case for single-use sterility in high-risk procedures. Over the forecast horizon, sterile back table and cart cover adoption is anchored by clinical policy, survey readiness, and pack standardization, while non-sterile cover demand remains stable in supporting roles. The back table and cart covers market continues to reflect this dichotomy as sites tune sterile allocations to case complexity and infection control targets.

Geography Analysis

North America held 43.44% in 2025 and maintains leadership based on a broad base of hospital infrastructure, a deep roster of acute-care and specialty programs, and long-standing group purchasing frameworks that enforce standardization. Updates to sterile-field expectations and multi-year contracting patterns combine to keep short-cycle replacement steady for back table and cart cover lines, while sustainability plans encourage material redesigns. Public-sector procurement and veteran health systems also reinforce vetted product lists and supply assurance through federal schedules and daily-updated contract catalogs. Over the forecast period, stable inpatient volumes and steady outpatient migration sustain balanced growth across hospital systems and independent facilities. The back table and cart covers market in North America continues to reward suppliers that pair manufacturing scale with documentation depth and timely distribution performance.

Asia-Pacific is the fastest-growing geography at a 6.19% CAGR over 2026-2031 as hospital capacity expansions, clinical safety adoption, and local production of nonwovens widen availability. Regional producers are releasing laminate-backed covers that match evolving barrier expectations while keeping unit costs aligned to public and private tender dynamics. These introductions allow facilities to align product selection to case complexity, with SMS formats for moderate procedures and laminate-backed covers for higher fluid volumes. As new hospitals come online, standardized pack approaches that bundle back table and cart covers are gaining acceptance because they simplify logistics and training. Growth is strongest where suppliers provide complete documentation sets and support qualification under multiple regulatory regimes across the region.

Europe remains steady as hospitals align to EN 13795 and sustain procurement programs that prioritize consistent barrier performance and documented conformity. MDR 2017/745 compliance deadlines have driven stock refresh and codified expectations around drape and cover performance, which benefits manufacturers with robust quality systems and audited production. Regional suppliers with vertically integrated capabilities are positioned to serve country-specific tendering and to hedge manufacturing footprints in support of resilience goals. Ongoing investments by premium producers in capacity, geographic reach, and sustainability attributes have supported continuity for sterile-field consumables across major EU health systems. The back table and cart covers market in Europe will continue to reflect these structural supports as procurement teams balance clinical outcomes, lifecycle documentation, and operational efficiency.

- Medline Industries

- Cardinal Health

- Owens & Minor (HALYARD)

- Lohmann & Rauscher (L&R)

- Hartmann Group

- Molnlycke Health Care

- TIDI Products

- STERIS

- DeRoyal Industries

- Healthmark (a Getinge company)

- Vital Care Industries

- AdvaCare

- Henry Schein (Custom Packs)

- Parity Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter sterile-field protocols and table-cover use in OR workflows post-2019 guideline updates

- 4.2.2 Rising outpatient/ASC surgical procedure volumes shifting barrier product demand to high-turnover settings

- 4.2.3 Adoption of custom procedure packs that include back table and instrument table covers

- 4.2.4 Higher penetration of nonwoven SMS/laminate barrier materials in surgical drapes and covers

- 4.2.5 OR turnover-time optimization using standardized table/cart covers (pre-set sterile fields)

- 4.2.6 Sustainability-led redesign (lighter, bio-based laminates) catalyzing product refresh cycles

- 4.3 Market Restraints

- 4.3.1 Environmental pressure favoring reusables or lower-footprint alternatives to single-use covers

- 4.3.2 Polypropylene/nonwoven raw-material price and availability volatility impacting costs

- 4.3.3 Practice variability and conflicting guidance on cover methods complicate adoption/training

- 4.3.4 Growing waste-management and EPR pressures increasing lifecycle cost of disposables

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Back Table Covers

- 5.1.2 Cart Covers

- 5.2 By Sterility

- 5.2.1 Sterile

- 5.2.2 Non-Sterile

- 5.3 By Material

- 5.3.1 SMS/PP Nonwoven

- 5.3.2 PE Film-Laminate

- 5.3.3 Spunlace/Rayon Nonwovens

- 5.3.4 Reusable Textile (Polyester/Cotton)

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgery Centers (ASCs)

- 5.4.3 Specialty Clinics / Office-based Surgery

- 5.5 By Distribution Channel

- 5.5.1 Direct Tenders / GPO Contracts

- 5.5.2 Distributor Sales

- 5.5.3 Online

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Medline Industries

- 6.3.2 Cardinal Health

- 6.3.3 Owens & Minor (HALYARD)

- 6.3.4 Lohmann & Rauscher (L&R)

- 6.3.5 Paul Hartmann AG

- 6.3.6 Molnlycke Health Care

- 6.3.7 TIDI Products

- 6.3.8 STERIS

- 6.3.9 DeRoyal Industries

- 6.3.10 Healthmark (a Getinge company)

- 6.3.11 Vital Care Industries

- 6.3.12 AdvaCare Pharma

- 6.3.13 Henry Schein (Custom Packs)

- 6.3.14 Parity Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment