PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063599

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063599

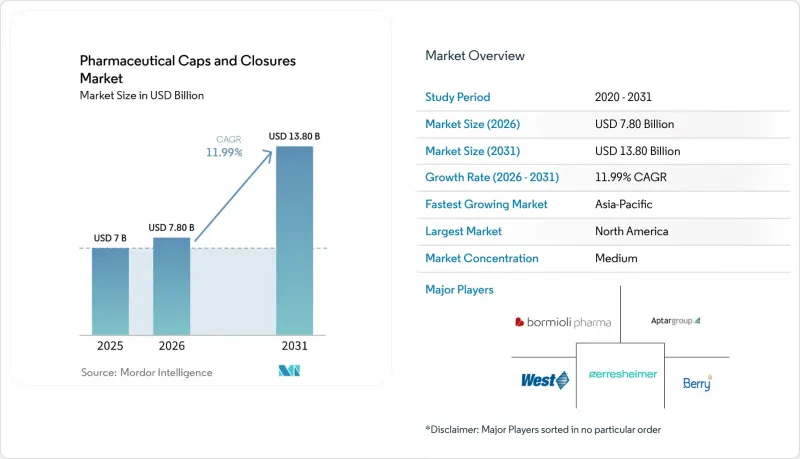

Pharmaceutical Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the pharmaceutical caps and closures market size is expected to grow from USD 7 billion in 2025 to USD 7.80 billion in 2026 and is forecast to reach USD 13.80 billion by 2031 at 11.99% CAGR over 2026-2031.

This report is Segmented by Material (Plastics, Elastomers/Rubber, Metals), Closure Type (Stoppers, Seals, Caps, Syringe & Cartridge Components, and More), Packaging Container (Bottles, Vials, Ampoules, Prefilled Syringes, Cartridges, IV Bags/Containers), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Pharmaceutical Caps And Closures Market Trends and Insights

Biologics Drive Surge in Demand for Vial Stoppers, Seals, and Syringe Closures

In 2025, biologics accounted for a significantly larger share of closure value compared to volume, driving a 20.3% year-on-year increase in high-value component revenue for West Pharmaceutical Services, surpassing the company's overall sales growth. GLP-1 receptor agonists alone contributed 10% to West's total enterprise revenue, demonstrating the substantial impact of a single drug class on closure demand. Larger-format vials and cartridges for biologics present challenges during freeze-thaw cycles, as conventional butyl stoppers fail to address thermal-expansion mismatches. West's FluroTec-coated stoppers addressed this issue by achieving a thermal-expansion delta of under 5 ppm/°C and reducing leak rates by 40% during cryogenic validation. This innovation enabled West to ship 43 billion components in 2025 at premium pricing. As pipeline biologics progress through late-stage trials, the demand for high-quality stoppers, seals, and plungers is expected to drive significant growth in the pharmaceutical caps and closures market.

Stricter Regulations Boost Adoption of Child-Resistant and Tamper-Evident Closures

In January 2024, the U.S. Consumer Product Safety Commission revised regulations, increasing the failure rate threshold for children attempting to open packages from 80% to 85% within five minutes. Simultaneously, ISO 8317 standards in Europe mandated tamper-evident features for all oral solid-dose prescription containers. These regulatory changes are accelerating the adoption of integrated CRC/TE closures, such as those offered by Aptar and Berry Global. Non-compliant packaging now faces recalls and distribution bans, emphasizing the importance of compliance. Additionally, FDA guidance in 2025 identified CRC validation delays as a factor contributing to drug shortages. Consequently, pharmaceutical companies are increasingly partnering with vendors offering pre-validated portfolios, strengthening the position of established players and driving the adoption of CRC/TE features in the pharmaceutical caps and closures market.

E&L and CCIT Compliance Complexity Increases Validation Costs/Time-to-Market

Comprehensive E&L studies on a single closure-container pair can cost over USD 30,000, while method development may delay approval timelines by up to a year. The FDA's 2024 draft guidance mandates quantitative risk assessments for all patient-contacting materials, significantly increasing the E&L burden. Furthermore, ICH Q3E, set for release in 2025, lowers the daily genotoxic leachable threshold to 1.5 µg, requiring reformulation of legacy elastomers. Deterministic CCIT methods, such as laser headspace analysis, demand capital investments nearing USD 500,000, along with annual calibration costs. These challenges force smaller firms to weigh the high costs of in-house laboratories against extended outsourced timelines, potentially restricting growth in the pharmaceutical caps and closures market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Ready-to-Use Sterile Components for Aseptic Fill-Finish Fuels Demand for RTU Closures

- Growing Trend of Self-Administration Elevates Demand for Intuitive Dosing and Nasal/Ophthalmic Closures

- Raw Material (Butyl Rubber, Aluminum) Price Volatility Pressures Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, plastics accounted for 63.18% of the pharmaceutical caps and closures market revenue, with a projected compound annual growth rate (CAGR) of 13.87% through 2031. The industry's shift toward cyclic olefin polymer and polypropylene barrels for prefilled syringes has driven demand for compatible plastic caps, backstops, and plunger rods. SCHOTT's TOPPAC polymer syringe, introduced in January 2025, reduces carbon emissions by 58% compared to glass alternatives. It is also compatible with SHL Medical's Maggie autoinjector, which has accelerated its adoption among biologic drug manufacturers. Elastomers remain essential for high-barrier applications, such as lyophilized biologics and vaccines requiring a five-year shelf life, relying on butyl-based stoppers with fluoropolymer laminates. Datwyler's NeoFlex and West's FluroTec product lines demonstrate the balance between controlling extractables and managing oxygen transmission.

Geography Analysis

In 2025, North America commanded a dominant 35.18% share of the pharmaceutical caps and closures market revenue, driven by the U.S.'s leadership in biologic R&D and strict enforcement of CCIT. The FDA's nitrosamine guidance, introduced in September 2024, along with ongoing discussions on Annex 1 harmonization, indicates sustained demand for validated closures well beyond 2028. Canada's Biologics and Genetic Therapies Directorate, along with Mexico's growth in near-shoring, is contributing incremental volumes, with Mexico benefiting from shorter lead times compared to Asia.

Europe, ranking second, is propelled by the adoption of ready-to-use solutions and green packaging mandates. A new RTU cartridge facility in Hungary, expected to become operational in 2027, is set to support EU Annex 1 upgrades in Germany, France, and Italy. Germany's strong contract-development sector is driving elastomer demand. Meanwhile, post-Brexit regulatory divergence requires suppliers to validate under both EMA and MHRA standards, extending timelines but increasing service revenues. Biosimilar clusters in Southern Europe, particularly in Spain and Italy, are consuming stoppers and seals at growth rates exceeding GDP, highlighting the region's significant influence on the pharmaceutical caps and closures market.

Asia-Pacific is a standout region, with an anticipated annual growth rate of 14.19% through 2031, fueled by the expansion of biosimilar production in China and India and greenfield investments in Southeast Asia. China's NMPA has streamlined review processes for imported closure systems meeting ICH Q3E standards, reducing entry barriers for premium suppliers. India's export-driven pharmaceutical sector, targeting USD 130 billion by 2030, increasingly demands compliance with FDA and EMA standards, favoring globally certified closure platforms. Although Australia's market is smaller, its enforcement of TGA nitrosamine limits, aligned with European standards, is pushing suppliers toward harmonized formulations.

- Adelphi Healthcare Packaging

- AptarGroup, Inc.

- Berry Global Group, Inc.

- Bormioli Pharma S.p.A.

- Comar LLc

- Datwyler Sealing Solutions

- DWK Life Sciences GmbH

- Gerresheimer

- Hebei First Rubber Medical Technology Co., Ltd.

- Jiangsu Hualan New Pharmaceutical Material Ltd.

- Lonstroff AG

- MRP Solutions

- Nemera Development S.A.

- Nipro

- Origin Ltd.

- Phoenix Closures, Inc.

- Sanner GmbH

- SCHOTT Pharma AG & Co. KGaA

- SGD SA

- Stevanato Group

- TekniPlex Inc.

- West Pharmaceutical Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth of Biologics and Injectables Elevates Demand for Vial Stoppers, Seals, and Syringe/Cartridge Closures

- 4.2.2 Stricter Child-Resistant and Tamper-Evident Mandates Increase CRC/TE Closure Adoption

- 4.2.3 Expansion of Ready-To-Use (RTU) Sterile Components for Aseptic Fill-Finish Boosts RTU Closures

- 4.2.4 Shift to Self-Administration/Home Care Raises Need for User-Friendly Dosing and Ophthalmic/Nasal Closures

- 4.2.5 EU GMP Annex 1 2022 Drives Container Closure Integrity (CCI) Upgrades and CCIT Adoption

- 4.2.6 Ultra-Cold/Cryogenic Storage for Atmps Requires Next-Gen Elastomer/Laminated Closures

- 4.3 Market Restraints

- 4.3.1 E&L and CCIT Compliance Complexity Increases Validation Costs/Time-To-Market

- 4.3.2 Raw Material (Butyl Rubber, Aluminum) Price Volatility Pressures Margins

- 4.3.3 Blow-Fill-Seal (BFS) Integration Can Reduce Use of Separate Closures in Select Liquid Formats

- 4.3.4 Nitrosamine Risk Management Constrains Elastomer Choices and Supply Flexibility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Plastics

- 5.1.2 Elastomers/Rubber

- 5.1.3 Metals (Aluminum seals)

- 5.2 By Closure Type

- 5.2.1 Stoppers

- 5.2.2 Seals

- 5.2.3 Caps

- 5.2.4 Syringe & Cartridge Components

- 5.2.5 Dropper & Dispensing Closures

- 5.2.6 Ports & IV Closure Systems

- 5.3 By Packaging Container

- 5.3.1 Bottles

- 5.3.2 Vials

- 5.3.3 Ampoules

- 5.3.4 Prefilled Syringes

- 5.3.5 Cartridges

- 5.3.6 IV Bags/Containers

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Adelphi Healthcare Packaging

- 6.3.2 AptarGroup, Inc.

- 6.3.3 Berry Global Group, Inc.

- 6.3.4 Bormioli Pharma S.p.A.

- 6.3.5 Comar LLc

- 6.3.6 Datwyler Sealing Solutions

- 6.3.7 DWK Life Sciences GmbH

- 6.3.8 Gerresheimer AG

- 6.3.9 Hebei First Rubber Medical Technology Co., Ltd.

- 6.3.10 Jiangsu Hualan New Pharmaceutical Material Ltd.

- 6.3.11 Lonstroff AG

- 6.3.12 MRP Solutions

- 6.3.13 Nemera Development S.A.

- 6.3.14 Nipro Corporation

- 6.3.15 Origin Ltd.

- 6.3.16 Phoenix Closures, Inc.

- 6.3.17 Sanner GmbH

- 6.3.18 SCHOTT Pharma AG & Co. KGaA

- 6.3.19 SGD SA

- 6.3.20 Stevanato Group S.p.A.

- 6.3.21 TekniPlex Inc.

- 6.3.22 West Pharmaceutical Services, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment