PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063618

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063618

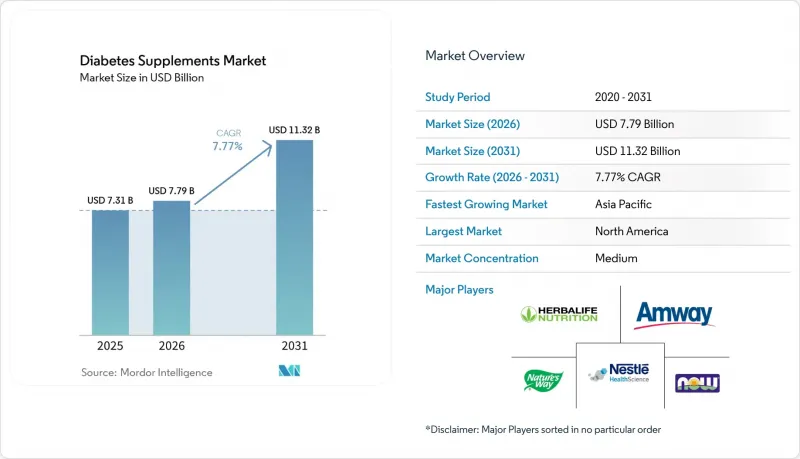

Diabetes Supplements - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the diabetes supplements market size was valued at USD 7.31 billion in 2025 and is estimated to grow from USD 7.79 billion in 2026 to reach USD 11.32 billion by 2031, at a CAGR of 7.77% during the forecast period (2026-2031).

This report is Segmented by Ingredient Type (Botanicals, Vitamins & Minerals, and More), Form (Capsules, Tablets, Softgels, Gummies and More), Distribution Channel (Pharmacies & Drug Stores, Supermarkets & Hypermarkets, Specialty & Practitioner Channels, Direct Selling, Online Channels/E-commerce), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Diabetes Supplements Market Trends and Insights

Rising Diabetes And Prediabetes Prevalence

Prevalence and awareness dynamics continue to define the demand base for the diabetes supplements market. The IDF Diabetes Atlas 11th edition reports elevated global prevalence and ongoing diagnostic gaps, which shape prevention and adjunctive care choices at scale. In the United States, 97.6 million adults live with prediabetes, yet only 19% are aware of their condition, a gap that sustains interest in lifestyle and supplementation before or alongside medications. Economic burden intensifies prevention incentives, with diabetes costs in the United States reported at USD 412.9 billion, reinforcing the rationale for lower-cost adjuncts that target adherence and tolerability.

Asia-Pacific's scale, reflected in large national caseloads in India and China, aligns with higher growth expectations for the diabetes supplements market through the forecast period. Emerging clinical evidence on diet and metabolic risk reinforces consumer interest in evidence-backed nutritional support, which dovetails with prevention programs and self-management resources from public health agencies.

Preventive Nutrition Adoption And Nutraceutical Usage

The diabetes supplements market continues to benefit from preventive frameworks that emphasize weight management and physical activity, where programmatic guidance positions diet and lifestyle as front-line measures for people with prediabetes. Peer-reviewed findings support microbiome-directed supplementation strategies in diabetes and prediabetes, including multi-strain probiotics and synbiotics, demonstrating modest HbA1c and inflammatory marker improvements in controlled settings. Trials and reviews highlight that daily doses at or above 109 CFU over 8-12 weeks underlie observed effects, with variations by strain composition and baseline gut status that inform product design.

Mechanistic research associates prebiotic fibers with short-chain fatty acid production and improved glycemic homeostasis, which strengthens rationale for synbiotic formulations within the diabetes supplements market. At the same time, evidence remains uneven across botanicals such as cinnamon, where the U.S. government's complementary health agency advises that current data do not support therapeutic use in diabetes, tempering clinical adoption while leaving room for consumer-led experimentation.

Regulatory Scrutiny On Diabetes-Disease Claims For Supplements

The regulatory climate places a premium on compliant claims and substantiation, limiting the scope of language that implies treatment or prevention of diabetes and redirecting brands toward structure-function positioning. In the United States, the standard for health claims requires significant scientific agreement, and judicial rulings have enabled qualified claims with disclaimers, which still impose legal and labeling complexity that adds costs and risk controls. EU authorities apply stringent efficacy criteria and close claim definitions, creating distinct EU-U.S. pathways that multinational brands must navigate without confusing consumers. These conditions encourage evidence-first messaging and reinforce the diabetes supplements market's shift toward transparency on dosing, target populations, and duration of use. As agencies prioritize public protection against delayed medical care, category participants invest more in clinician education materials that clarify adjunctive roles. The net effect is a more cautious promotional environment that rewards brands with robust documentation and disciplined label governance.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce And Online Pharmacies Expansion

- EFSA-Eligible Chromium Health Claim Enabling EU Marketing

- Limited High-Quality Clinical Evidence Reduces HCP Endorsements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Botanicals held the largest share at 34.53% of the diabetes supplements market in 2025 as brands balanced familiarity and traditional usage with modern quality controls. In parallel, probiotics and prebiotics are the fastest-growing category at a 9.93% CAGR through 2031 as multi-strain and synbiotic designs demonstrate modest yet consistent support for glycemic and inflammatory markers in controlled trials. Research links daily intakes at or above 109 CFU for 8-12 weeks to effect sizes on HbA1c and C-reactive protein that, while small, are relevant to adjunctive regimens in type 2 diabetes and prediabetes. As a result, the diabetes supplements market features strain-forward product labels and co-formulants like inulin to drive SCFA production associated with improved metabolic signaling. Companies are also refining safety and purity practices for botanicals as variability challenges precise dosing and cross-border compliance, which sustains demand for ingredients with standardized actives and transparent sourcing.

Demand patterns across vitamins, minerals, antioxidants, and omega-3s reflect cross-sell into cardiometabolic comorbidities and neuropathy prevention use cases. Chromium remains present but constrained by qualified-claim rules in the United States and modest glycemic effect sizes in meta-analyses, which shapes positioning toward inclusion within broader blends. Alpha-lipoic acid, vitamin D3, magnesium, and B-complex formulations maintain stable roles where practitioners emphasize nerve health and general nutritional adequacy, keeping assortment breadth across channels. As studies refine personalized response patterns, suppliers prioritize clinical documentation that specifies strain, dose, and duration to align expectations and support practitioner guidance. These shifts reinforce product architectures that can be titrated or bundled, which supports repeat purchase behavior and clearer regimen adherence in the diabetes supplements market.

Geography Analysis

North America held the largest regional position with a 34.53% share in 2025, supported by high care utilization and broad adoption of preventive and adjunctive solutions in the diabetes supplements market. The United States anchors this base with significant diabetes spending, where the reported USD 412.9 billion economic burden elevates consumer and payer interest in affordable adjuncts that can support adherence and comfort alongside standard care. Widespread prediabetes adds to the addressable audience, given that fewer than one in five affected adults are aware of their status, which keeps self-directed prevention and monitoring in focus. Canada and Mexico contribute incremental expansion through pharmacy and online channels as coverage for monitoring technologies evolves and retail assortments broaden. Clinical communication emphasizes realistic expectations for supplements as complements to diet, activity, and medications, which grounds purchasing behavior in safe, long-term use patterns.

Asia-Pacific is the fastest-growing region with a projected 10.02% CAGR through 2031, underpinned by large national caseloads and increasing urban health engagement in the diabetes supplements market. IDF data reflect substantial case volumes in India and China, which steer manufacturers to localized portfolios and language on dosage, format, and diet fit that resonate with younger adults and working-age populations. Digital commerce and health platforms provide route-to-market advantages across cities where pharmacy footprints are fragmented, accelerating access to clinically characterized probiotics, synbiotics, vitamins, and fibers. As product education meets mobile-first content, consumers align choices with lifestyle preferences and feedback from self-monitoring, which encourages repeat purchase patterns. The diabetes supplements market size in these countries will reflect both the scale of metabolic risk and the speed at which transparent labeling and third-party verification practices spread through online marketplaces.

Europe maintains steady growth supported by pharmacy-led distribution, clear claim frameworks, and persistent interest in clinically characterized ingredients. EU-authorized chromium claims shape positioning for glucose-related maintenance, while the United Kingdom's guideline evolution on medication access informs how consumers choose adjuncts and supportive ingredients to fit personalized care plans. In markets such as Germany, France, Italy, and Spain, the diabetes supplements market share for pharmacy channels remains high due to pharmacist influence on product selection and adherence counseling. Middle East and Africa present a patchwork of opportunities aligned to premium imports in the Gulf states and pharmacy chains in South Africa. South America shows expansion focused on Brazil and Argentina as online retail augments traditional pharmacy distribution.

- Amway Corp.

- Arkopharma

- Blackmores

- Curalife

- Dabur

- Glucose Health, Inc.

- Guardian Healthcare Services Pvt. Ltd.

- Herbalife Nutrition

- Himalaya

- Jamieson Wellness Inc.

- Jarrow Formulas

- Life Extension

- Lysulin, Inc.

- Nature's Sunshine Products, Inc.

- Nature's Way Brands, LLC.

- Nestle Health Science

- NOW Foods

- Patanjali Ayurved

- Pure Encapsulations

- Swanson

- Thorne

- Vitabiotics (Diabetone)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Diabetes and Prediabetes Prevalence

- 4.2.2 Preventive Nutrition Adoption and Nutraceutical Usage

- 4.2.3 E-Commerce and Online Pharmacies Expansion

- 4.2.4 EFSA-Eligible Chromium Health Claim Enabling EU Marketing

- 4.2.5 CGM Adoption Beyond Diabetics Catalyzing Supplement Experimentation

- 4.2.6 Comorbidity Cross-Sell (Neuropathy, Eye Health) Boosting Adjunct Demand

- 4.3 Market Restraints

- 4.3.1 Regulatory Scrutiny on Diabetes-Disease Claims for Supplements

- 4.3.2 Limited High-Quality Clinical Evidence Reduces HCP Endorsements

- 4.3.3 GLP-1/SGLT-2 Uptake Substituting for Glucose-Lowering Supplements

- 4.3.4 Botanical Quality Variability Curbing Dosages/Claims

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Ingredient Type

- 5.1.1 Botanicals

- 5.1.2 Vitamins & Minerals

- 5.1.3 Antioxidants

- 5.1.4 Omega-3 Fatty Acids

- 5.1.5 Probiotics/Prebiotics

- 5.1.6 Others (Fibers & Specialty Carbohydrates, Amino Acids)

- 5.2 By Form

- 5.2.1 Capsules

- 5.2.2 Tablets

- 5.2.3 Softgels

- 5.2.4 Powder

- 5.2.5 Liquid

- 5.2.6 Gummies

- 5.3 By Distribution Channel

- 5.3.1 Pharmacies & Drug Stores

- 5.3.2 Supermarkets & Hypermarkets

- 5.3.3 Specialty & Practitioner Channels

- 5.3.4 Direct Selling

- 5.3.5 Online Channels (E-commerce)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Amway Corp.

- 6.3.2 Arkopharma

- 6.3.3 Blackmores

- 6.3.4 Curalife

- 6.3.5 Dabur

- 6.3.6 Glucose Health, Inc.

- 6.3.7 Guardian Healthcare Services Pvt. Ltd.

- 6.3.8 Herbalife Nutrition

- 6.3.9 Himalaya Wellness Company

- 6.3.10 Jamieson Wellness Inc.

- 6.3.11 Jarrow Formulas, Inc.

- 6.3.12 Life Extension

- 6.3.13 Lysulin, Inc.

- 6.3.14 Nature's Sunshine Products, Inc.

- 6.3.15 Nature's Way Brands, LLC.

- 6.3.16 Nestle Health Science

- 6.3.17 NOW Foods

- 6.3.18 Patanjali Ayurved Limited

- 6.3.19 Pure Encapsulations

- 6.3.20 Swanson

- 6.3.21 Thorne

- 6.3.22 Vitabiotics (Diabetone)

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment