PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063619

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063619

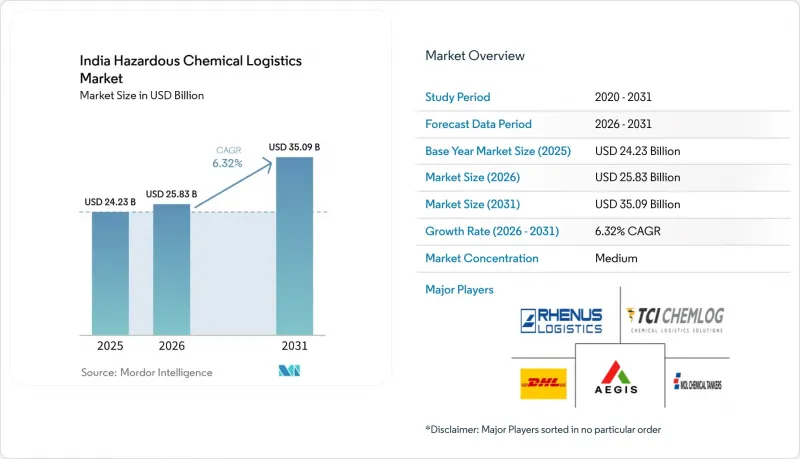

India Hazardous Chemical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, india hazardous chemical logistics market size is expected to increase from USD 24.23 billion in 2025 to USD 25.83 billion in 2026 and reach USD 35.09 billion by 2031, growing at a CAGR of 6.32% over 2026-2031.

This trajectory reflects a blend of new petrochemical capacity along the coastline, rising demand for outsourced compliance services, and multimodal investments that shift bulk cargo from roads to pipelines, rail, and inland waterways. This report is Segmented by Service Type (Transportation, and Others), by Hazardous Chemical Class (Flammable Liquids, Compressed Gases, Corrosive Substances, and Others), by End-User Industry (Petrochemicals and Bulk Chemicals, and Others), and by Geography (North India, South India, West India, East India, and Central India). Market Forecasts are Provided in Terms of Value (USD).

India Hazardous Chemical Logistics Market Trends and Insights

Expansion of India's Overall Chemical Output (Bulk & Basic)

India's chemicals output reached more than USD 220 billion in 2025 and is pegged to keep rising as new crackers in Rajasthan and Odisha ramp up capacity. Each additional tonne of caustic soda, chlorine, or methanol must move in PESO-certified tankers, ISO containers, or rail rakes, driving sustained demand for compliant logistics services. Indian Oil's Paradip-Haldia pipeline alone is expected to displace roughly 10,000 annual truck trips, freeing road bandwidth for specialty cargoes. Similar pipeline and tank-farm expansions by Aegis Logistics show how storage and evacuation assets scale line by line with upstream production. The long-term volume uplift persists because India's per capita petrochemical consumption is one-third the world average.

Surge in Specialty & Pharma-Chemical Production Requiring Compliant Logistics

Specialty and pharmaceutical chemicals entail smaller lot sizes, stricter temperature bands, and real-time traceability. New active pharmaceutical ingredient (API) parks in Una and Vizag, plus fluorochemical investments in Gujarat and Tamil Nadu, create high-margin lanes for temperature-controlled trucking, repackaging, and emergency response planning. Snowman Logistics and Kuehne + Nagel are already commissioning 15-25 °C warehouses with gas detection and batch-level barcoding to win five-year outsourcing contracts. Mid-term growth remains solid as commissioned plants ramp from trial to commercial output over 24-36 months.

High CAPEX and Compliance Costs for Hazmat-Graded Fleets & Warehouses

A stainless-steel chemical tanker that meets PESO's Static & Mobile Pressure Vessels Rules 2016 costs USD 60,000-85,000, roughly double a standard fuel tanker. Annual certifications, specialized insurance, and driver training add another USD 6,000-10,000 per vehicle, making fleet renewal a capital-intensive exercise for small operators. Warehouse automation is equally pricey: Godrej's new 120-foot rack-clad store in Mumbai required robotic shuttles and explosion-proof wiring, pushing investment past USD 500 per square foot. In the short run, high entry costs curb fresh capacity and slow response to demand spikes.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Petrochemical and Refining Capacity Across Coastal Clusters

- Stricter Hazardous-Materials Rules (PESO, IMDG, DG Shipping) Raising Outsourcing Demand

- Acute Shortage of HAZMAT-Certified Drivers and Handlers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation accounted for 64.51% of the India hazardous chemical logistics market share in 2025, reflecting the country's reliance on road tankers for last-mile delivery. Rail is regaining ground as AVG Logistics' ISO-tank trains cut unit costs by 25% and bypass driver shortages. Sea and inland waterways remain underpenetrated despite clear cost advantages; draft limits on National Waterways 4 and 5 keep barge sizes small. Over 2026-2031, value-added services, led by blending, relabeling, and emergency-response planning, will post the fastest 9.52% CAGR as pharma and specialty shippers outsource compliance headaches. Snowman's new 50,000 sq ft hazmat-cold store in Tamil Nadu and Kuehne+Nagel's expanded 450,000 m2 contract-logistics footprint show providers pivoting toward high-margin ancillary work that cushions rate volatility.

The India hazardous chemical logistics market size for value-added services is forecast to advance steadily as PESO tightens warehouse rules. AIS-140 telematics unlock geo-fencing, predictive maintenance, and batch-level audit trails, thereby raising switching costs. Bigger players leverage captive tech stacks to bundle transport with warehousing, thus improving retention and margin per load. Investments in foam-suppressed racks and battery-powered forklifts set entry barriers that small regional carriers struggle to cross, signaling ongoing consolidation.

List of Companies Covered in this Report:

- Aegis Logistics Ltd

- TCI Chemlog (Transport Corporation of India)

- Allcargo Logistics Ltd

- DHL Supply Chain India

- DSV A/S (including DB Schenker)

- Kuehne+Nagel

- Rhenus Logistics

- Snowman Logistics Ltd

- CMA CGM (Including CEVA Logistics)

- GEODIS

- Den Hartogh Logistics India

- BDP International India

- Hellmann Worldwide Logistics India

- MOL Chemical Tankers India

- Seashell Logistics Pvt. Ltd.

- Bertschi India

- TVS Supply Chain Solutions

- Hazchem Logistics Management LLP

- AWL INDIA

- Milkyway Chem Logistics India

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of India's Overall Chemical Output (Bulk and Basic)

- 4.2.2 Surge in Specialty and Pharma-Chemical Production Requiring Compliant Logistics

- 4.2.3 Expansion of Petrochemical and Refining Capacity Across Coastal Clusters

- 4.2.4 Stricter Hazardous-Materials Rules (PESO, IMDG, DG Shipping) Raising Outsourcing Demand

- 4.2.5 Development of Petroleum, Chemicals and Petrochemicals Investment Regions (PCPIRs)

- 4.2.6 Inland-Waterway Corridors (NW-1, 4, 5) Opening Low-Cost Chemical Routes

- 4.3 Market Restraints

- 4.3.1 High CAPEX and Compliance Costs for Hazmat-Graded Fleets and Warehouses

- 4.3.2 Acute Shortage of HAZMAT-Certified Drivers and Handlers

- 4.3.3 State-Wise Regulatory Fragmentation Slowing Multimodal Transfers

- 4.3.4 CRZ Clearance Delays for New Coastal Chemical Terminals

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Geo-Political Events

5 Market Size and Growth Forecasts (Value)

- 5.1 Segmentation by Service Type

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Sea / Coastal and Inland Waterways

- 5.1.1.4 Air

- 5.1.2 Storage, Warehousing and Distribution

- 5.1.3 Value Added Services

- 5.1.1 Transportation

- 5.2 Segmentation by Hazardous Chemical Class

- 5.2.1 Flammable Liquids

- 5.2.2 Compressed Gases

- 5.2.3 Corrosive Substances

- 5.2.4 Toxic Substances

- 5.2.5 Oxidizing Substances

- 5.2.6 Radioactive Materials

- 5.2.7 Other Chemicals

- 5.3 Segmentation by End-User Industry

- 5.3.1 Petrochemicals and Bulk Chemicals

- 5.3.2 Specialty Chemicals

- 5.3.3 Pharmaceuticals and Life Sciences

- 5.3.4 Agrochemicals and Fertilizers

- 5.3.5 Batteries, Electronics and EV Materials

- 5.3.6 Other Industries

- 5.4 Segmentation by Region

- 5.4.1 North India

- 5.4.2 South India

- 5.4.3 West India

- 5.4.4 East India

- 5.4.5 Central India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 Aegis Logistics Ltd

- 6.4.2 TCI Chemlog (Transport Corporation of India)

- 6.4.3 Allcargo Logistics Ltd

- 6.4.4 DHL Supply Chain India

- 6.4.5 DSV A/S (including DB Schenker)

- 6.4.6 Kuehne+Nagel

- 6.4.7 Rhenus Logistics

- 6.4.8 Snowman Logistics Ltd

- 6.4.9 CMA CGM (Including CEVA Logistics)

- 6.4.10 GEODIS

- 6.4.11 Den Hartogh Logistics India

- 6.4.12 BDP International India

- 6.4.13 Hellmann Worldwide Logistics India

- 6.4.14 MOL Chemical Tankers India

- 6.4.15 Seashell Logistics Pvt. Ltd.

- 6.4.16 Bertschi India

- 6.4.17 TVS Supply Chain Solutions

- 6.4.18 Hazchem Logistics Management LLP

- 6.4.19 AWL INDIA

- 6.4.20 Milkyway Chem Logistics India

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment