PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063628

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063628

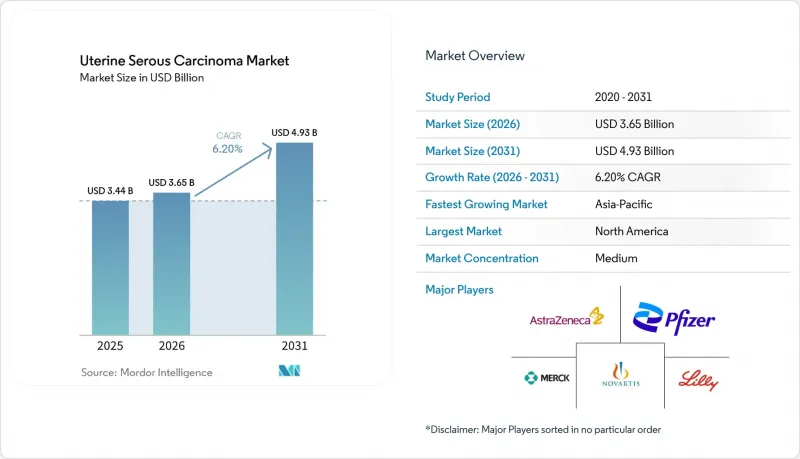

Uterine Serous Carcinoma - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the uterine serous carcinoma market size is projected to expand from USD 3.44 billion in 2025 and USD 3.65 billion in 2026 to USD 4.93 billion by 2031, registering a CAGR of 6.20% between 2026 to 2031.

This report is Segmented by Treatment Modality (Surgery, Chemotherapy, Radiotherapy, Immunotherapy, Targeted Therapy), Drug Class (Immune Checkpoint Inhibitors, and More), Line of Therapy (First-Line, Second-Line & Later), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Uterine Serous Carcinoma Market Trends and Insights

Rising Incidence Linked to Aging & Obesity

The global rise in metabolic syndrome is driving a steady increase in endometrial cancer diagnoses, with a pronounced shift toward serous histology among women over 60. Obesity-related inflammation elevates peripheral estrogen levels, encouraging TP53 mutations that typify the serous subtype and shorten the interval from stage I to metastatic disease. Japan, Italy, and South Korea face a triple burden of aging populations, delayed first pregnancies, and reduced parity, all of which extend lifetime estrogen exposure. Consequently, the addressable patient pool is expanding faster than historical averages, stimulating sustained demand for first-line immune-checkpoint doublets and salvage antibody-drug conjugates through 2031. Health ministries are already signaling higher budget allocations for gynecologic oncology, locking in multiyear procurement contracts that underpin volume certainty for drug makers.

Regulatory Approvals for Immuno-Oncology Combinations

The FDA's June 2024 accelerated approval of pembrolizumab plus carboplatin-paclitaxel for newly diagnosed advanced disease cut the standard four-year bench-to-bedside interval in half, encouraging sponsors to file combination biologics earlier in development. The European Commission's conditional nod four months later enabled pan-EU reimbursement negotiations and prompted several national payers to waive sequential chemotherapy prerequisites. Regulators in Japan, South Korea, and Australia rapidly adopted comparable review pathways, reducing the lag between U.S. and Asia-Pacific launches to under one year. These synchronized approvals compress time-to-revenue and push manufacturers to initiate global pivotal trials from day one to secure a wider uterine serous carcinoma market footprint.

High Costs & Reimbursement Hurdles for IO Agents

In the United States, checkpoint inhibitors are priced between USD 150,000 and 200,000 annually per patient, resulting in prior-authorization requirements that can delay treatment by up to a month.Fourteen Medicaid programs in the United States mandate chemotherapy failure before approving immunotherapy, restricting its use as a first-line treatment. In Latin America, public insurers negotiate confidential rebates of 30-50%. However, budget caps limit drug availability to major academic centers. Private payers in the Gulf Cooperation Council require biomarker evidence and impose annual spending limits, often causing interruptions to therapy mid-cycle. These challenges collectively reduce the global market's compound annual growth rate for uterine serous carcinoma by nearly one percentage point.

Other drivers and restraints analyzed in the detailed report include:

- Uptake of Molecular Profiling & HER2 Testing

- Companion-Diagnostic Reimbursement Incentives

- Limited Biomarker-Testing in LMICs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Immunotherapy accounted for a 38.15% share of the uterine serous carcinoma market size in 2025 and is projected to grow at a 7.34% CAGR through 2031. Pembrolizumab, combined with carboplatin-paclitaxel, advanced to first-line therapy following its FDA approval in June 2024, quickly replacing chemotherapy-only regimens at NCCN-designated centers. Dostarlimab monotherapy has become a preferred option for mismatch-repair-deficient tumors, achieving objective response rates exceeding 40%. Surgery continues to be the standard for early-stage disease, but neoadjuvant immunotherapy is reducing tumor volume in bulky stage III cases, improving resectability. Radiation therapy is now primarily used for palliating symptomatic pelvic relapse or brain metastases, reflecting a shift toward systemic control.

Geography Analysis

In 2025, North America held a dominant 43.13% share of the uterine serous carcinoma market, attributed to Medicare's efficient reimbursement process. Medicare reimburses drugs such as pembrolizumab, dostarlimab, and trastuzumab deruxtecan for FDA-approved indications without requiring prior authorization. Starting January 2026, the Inflation Reduction Act allows Medicare to negotiate prices for oncology drugs. This initiative is expected to reduce net costs by 25-40% for the highest-spending drugs. While this measure ensures continued patient access, it also moderates revenue growth, prompting manufacturers to explore opportunities in Asia to increase volumes.

Asia-Pacific is the fastest-growing region, advancing at a 6.98% CAGR. China's rapid approval of sintilimab and tislelizumab for MSI-high tumors, along with Japan's expedited designation for trastuzumab deruxtecan, has reduced the time-to-launch to less than nine months after first-in-class approvals. In South Korea and Australia, checkpoint inhibitors are reimbursed within 60 days of regulatory approval, making these countries early contributors to revenue.

Europe holds a stable share but displays heterogeneity. Germany and France reimburse immune-checkpoint combinations promptly, whereas Italy and Spain impose budget caps that delay adoption at the hospital level. Eastern European countries negotiate significant rebates but primarily restrict access to urban tertiary centers. In the Middle East and Africa, the uterine serous carcinoma market accounts for less than 5% of the total size due to systemic therapy penetration remaining low. Challenges such as limited cold-chain infrastructure, currency volatility, and insufficient local biologic manufacturing capacity hinder drug availability, emphasizing the need for international funding initiatives.

- AstraZeneca PLc

- Clovis Oncology

- Eisai

- Eli Lilly and Company

- Exelixis

- Roche

- GlaxoSmithKline

- ImmunoGen

- Incyte

- Innovent Biologics, Inc.

- MacroGenics

- Merck

- Mersana Therapeutics

- Myovant Sciences Ltd.

- Novartis

- OncXerna Therapeutics Inc.

- Pfizer

- Regeneron Pharmaceuticals

- Seagen

- Zai Lab Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence Linked to Aging & Obesity

- 4.2.2 Regulatory Approvals for Immuno-Oncology Combinations

- 4.2.3 Uptake of Molecular Profiling & HER2 Testing

- 4.2.4 Expansion of Investigator-Sponsored Trials & EAPS

- 4.2.5 Companion-Diagnostic Reimbursement Incentives (OECD)

- 4.2.6 Fast-Track Synthetic-Lethality Pipeline Inflection

- 4.3 Market Restraints

- 4.3.1 High Cost & Reimbursement Hurdles for IO Agents

- 4.3.2 Low Biomarker-Testing Penetration in LMICs

- 4.3.3 Patient-Pool Limitations Slowing Trial Recruitment

- 4.3.4 Safety Concerns Over TKI + Checkpoint Blockade Combos

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Epidemiology Trends & Incidence Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Treatment Modality

- 5.1.1 Surgery

- 5.1.2 Chemotherapy

- 5.1.3 Radiotherapy

- 5.1.4 Immunotherapy

- 5.1.5 Targeted Therapy

- 5.2 By Drug Class

- 5.2.1 Immune Checkpoint Inhibitors

- 5.2.2 Tyrosine-Kinase Inhibitors

- 5.2.3 HER2-targeted Monoclonal Antibodies

- 5.2.4 Hormonal Agents

- 5.2.5 Cytotoxic Agents

- 5.3 By Line of Therapy

- 5.3.1 First-Line

- 5.3.2 Second-Line & Later

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AstraZeneca PLc

- 6.3.2 Clovis Oncology

- 6.3.3 Eisai Co.

- 6.3.4 Eli Lilly & Co.

- 6.3.5 Exelixis Inc.

- 6.3.6 F. Hoffmann-La Roche Ltd

- 6.3.7 GlaxoSmithKline PLC

- 6.3.8 ImmunoGen

- 6.3.9 Incyte Corporation

- 6.3.10 Innovent Biologics, Inc.

- 6.3.11 MacroGenics, Inc.

- 6.3.12 Merck & Co.

- 6.3.13 Mersana Therapeutics

- 6.3.14 Myovant Sciences Ltd.

- 6.3.15 Novartis AG

- 6.3.16 OncXerna Therapeutics Inc.

- 6.3.17 Pfizer Inc.

- 6.3.18 Regeneron Pharmaceuticals, Inc.

- 6.3.19 Seagen Inc.

- 6.3.20 Zai Lab Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment