PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063630

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063630

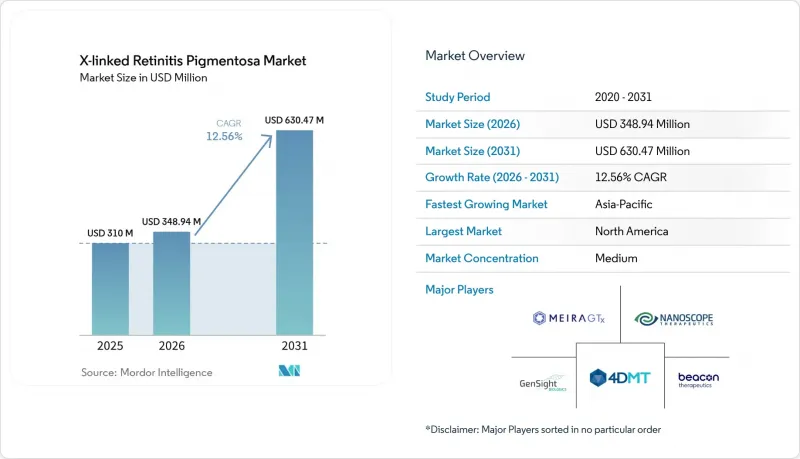

X-linked Retinitis Pigmentosa - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the x-linked retinitis pigmentosa market size is expected to grow from USD 310 million in 2025 to USD 348.94 million in 2026 and is forecast to reach USD 630.47 million by 2031 at 12.56% CAGR over 2026-2031.

This report is Segmented by Therapy Type (Gene Therapy, and More), Stage of Development (Discovery & Preclinical, and More), Route of Administration (Sub-Retinal, Intravitreal, Oral/Systemic, and More), End User (Hospitals & Eye-Care Chains, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global X-linked Retinitis Pigmentosa Market Trends and Insights

Breakthroughs in AAV-Mediated RPGR Gene Therapy

In 2024, MeiraGTx progressed botaretigene sparoparvovec to Phase III, enrolling 60 participants across 12 global sites, with interim data expected in late 2026. The vector employs a codon-optimized RPGR-ORF15 under a rhodopsin-kinase promoter, addressing approximately 70% of genetically confirmed cases. Janssen's investment of USD 1.7 billion highlighted durability expectations initially observed in non-human primates. However, high baseline anti-AAV8 antibodies, present in up to 84% of treatment-naive children, significantly reduced the pool of eligible candidates. Sponsors are developing capsid variants through platforms like NAV to overcome neutralization at titers ten times higher than the wild-type AAV8.

Payer Acceptance of One-Time Curative Pricing Models

In 2024, CMS introduced its cell and gene therapy access model, allocating USD 2 billion for outcomes-based Medicaid contracts. These contracts reimburse therapies priced between USD 850,000 and USD 1.2 million per eye. Early adopter states require 80% of recipients to achieve a 15-letter gain on the ETDRS scale at 24 months, with rebates of up to 40% of the list price triggered if this benchmark is not met. Manufacturers can securitize future rebate obligations, reducing capital costs and enhancing payor confidence in the X-linked retinitis pigmentosa market. However, only six out of 18 surveyed US commercial insurers maintain rare-disease budgets exceeding USD 50 million, and many enforce strict lifetime caps.

Sub-Retinal Surgical Capacity Bottlenecks

In 2024, the American Society of Retina Specialists reported only 3,000 active vitreoretinal surgeons in the U.S., with 40% aged over 55. While sub-retinal injections demand advanced retinotomy skills, reimbursement for the procedure (code 67036) has stagnated at USD 1,200 since 2020.Consequently, only 35 U.S. centers could administer Luxturna in its initial two commercial years, leading to six-month wait times. MeiraGTx is testing a hub-and-spoke training network, but each surgeon's capacity is limited to 2-3 cases daily until intravitreal vectors demonstrate equivalence.

Other drivers and restraints analyzed in the detailed report include:

- Priority-Review Vouchers Accelerating ROI

- Cross-Licensing of CRISPR IP Lowering Barriers

- Uncertain Durability of Vector Expression

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, gene replacement accounted for 82.34% of the x-linked retinitis pigmentosa market share, translating to approximately USD 287 million within the broader market size. Three pivotal AAV8-RPGR programs focus on preserving photoreceptors, a clinical endpoint increasingly recognized by regulators as a surrogate for functional vision. Optogenetics, while holding a smaller share in 2025, is projected to achieve the fastest growth at a 15.23% CAGR, driven by MCO-010's pursuit of FDA approval without requiring vector-serotype matching or intact outer segments.

Nanoscope's opsin activates under ambient light, eliminating the need for bulky goggles and increasing adoption among elderly patients. Meanwhile, BlueRock's iPSC-derived photoreceptors, which entered Phase I/II to address late-stage degeneration, face cost-of-goods challenges that could exceed USD 900,000 per dose. Pharmacologic neuroprotection remains a secondary option, limited by its transient efficacy and the need for continuous dosing.

Phase I/II assets formed 54.06% of the X-linked retinitis pigmentosa market size pipeline in 2025, highlighting clinical immaturity despite growing enthusiasm for novel modalities. Discovery programs driven by CRISPR-based editing are advancing at a 14.95% CAGR, supported by declining royalty rates and modular guide-RNA designs that shorten lead-optimization timelines.

Phase III trials, comprising only 12% of the pipeline, exert significant influence by setting precedents for durability and safety, particularly in pediatric dosing. The first approvals are expected to trigger a follow-the-leader dynamic, with payers benchmarking budget impacts against early pricing signals. Approved therapies remain minimal, limited to off-label Luxturna use in the rare RPGR-RPE65 overlap, a cohort of fewer than 50 patients worldwide.

Geography Analysis

In 2025, North America commanded 41.13% of the X-linked retinitis pigmentosa market size, supported by 19 active trial sites and two CMS reimbursement pilots. The U.S. Orphan Drug Act provides a waiver of USD 3.2 million in FDA fees and grants seven years of exclusivity, reducing sponsor breakeven points. Additionally, Canada's CAD 1.4 billion rare-disease drug strategy acts as a significant payer anchor, offering conditional coverage for gene therapies that meet Health Canada's Notice of Compliance with Conditions pathway.

Europe held a 32% share, but pricing varies threefold across member states due to distinct cost-per-QALY thresholds applied by HTA agencies. For example, Germany's IQWiG limits willingness-to-pay at EUR 80,000 (USD 93,655.60), while England's NHS adjusts thresholds for ultra-orphan drugs. These adjustments lead to parallel negotiations, extending launch timelines by an average of nine months. GenSight's LUMEVOQ experience highlights this disparity: reimbursed in France and Italy within a year but still delayed in Spain as of 2026.

Asia-Pacific, currently at 18%, is the fastest-growing region with a 14.58% CAGR, driven by China's inclusion of 85 rare-disease drugs in its National Reimbursement List and Japan's SAKIGAKE pathway, which grants conditional approval after Phase II data. South Korea's 2024 Rare Disease Act requires the National Health Insurance Service to reimburse 80% of therapy costs for patient populations under 20,000, effectively supporting upcoming X-linked retinitis pigmentosa launches. Latin America and the Middle East & Africa remain in early stages, hindered by limited surgical capacity and fragmented payer systems, but early regulatory developments are evident, such as ANVISA's priority review for three ocular gene therapies in 2024.

- 4D Molecular Therapeutics Inc.

- Adverum Biotechnologies, Inc.

- Alkeus Pharmaceuticals

- Beacon Therapeutics Inc.

- Beam Therapeutics Inc.

- Biogen

- CRISPR Therapeutics AG

- Editas Medicine

- GenSight Biologics S.A

- Horama SA

- Johnson & Johnson (Janssen/Beacon)

- MeiraGTx Holdings PLC

- Nanoscope Therapeutics Inc.

- Neurotech Pharmaceuticals, Inc.

- Novartis

- Ocugen

- ProQR Therapeutics Inc.

- Regenxbio Inc.

- RetinalGenix Technologies

- Spark Therapeutics (Roche)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Breakthroughs in AAV-Mediated RPGR Gene Therapy

- 4.2.2 Payer Acceptance of One-Time Curative Pricing Models

- 4.2.3 Priority-Review Vouchers Accelerating ROI

- 4.2.4 Cross-Licensing of CRISPR IP Lowering Barriers

- 4.2.5 Emergence of AI-Guided Retinal Imaging Endpoints

- 4.2.6 Venture Philanthropy De-Risking Early Trials

- 4.3 Market Restraints

- 4.3.1 Sub-Retinal Surgical Capacity Bottlenecks

- 4.3.2 Uncertain Durability of Vector Expression

- 4.3.3 Anti-AAV Neutralising Antibodies in Paediatric Pools

- 4.3.4 Competing Optogenetic Pipelines Crowding Trial Sites

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Therapy Type

- 5.1.1 Gene Therapy

- 5.1.2 Pharmacological Agents

- 5.1.3 Optogenetics

- 5.1.4 Stem Cell Therapies

- 5.1.5 Others

- 5.2 By Stage of Development

- 5.2.1 Discovery & Preclinical

- 5.2.2 Phase I/II

- 5.2.3 Phase III

- 5.2.4 Approved/Commercial

- 5.3 By Route of Administration

- 5.3.1 Sub-retinal

- 5.3.2 Intravitreal

- 5.3.3 Oral/Systemic

- 5.3.4 Others

- 5.4 By End User

- 5.4.1 Hospitals & Eye-care Chains

- 5.4.2 Academic & Research Institutes

- 5.4.3 Specialty Clinics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 4D Molecular Therapeutics Inc.

- 6.3.2 Adverum Biotechnologies, Inc.

- 6.3.3 Alkeus Pharmaceuticals

- 6.3.4 Beacon Therapeutics Inc.

- 6.3.5 Beam Therapeutics Inc.

- 6.3.6 Biogen Inc.

- 6.3.7 CRISPR Therapeutics AG

- 6.3.8 Editas Medicine

- 6.3.9 GenSight Biologics S.A

- 6.3.10 Horama SA

- 6.3.11 Johnson & Johnson (Janssen/Beacon)

- 6.3.12 MeiraGTx Holdings PLC

- 6.3.13 Nanoscope Therapeutics Inc.

- 6.3.14 Neurotech Pharmaceuticals, Inc.

- 6.3.15 Novartis AG

- 6.3.16 Ocugen Inc.

- 6.3.17 ProQR Therapeutics Inc.

- 6.3.18 Regenxbio Inc.

- 6.3.19 RetinalGenix Technologies

- 6.3.20 Spark Therapeutics (Roche)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment