PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063644

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063644

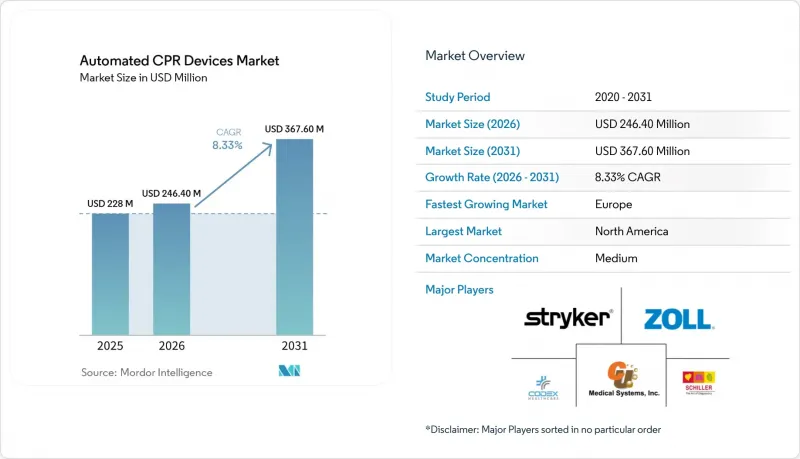

Automated CPR Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the automated CPR devices market size was valued at USD 228 million in 2025 and is estimated to grow from USD 246.40 million in 2026 to reach USD 367.60 million by 2031, at a CAGR of 8.33% during the forecast period (2026-2031).

This report is Segmented by Device Type (Piston-Driven, Load-Distributing Band), Power Source (Battery-Electric, Pneumatic/Oxygen-driven), End User (Hospitals, EMS Providers, Military & Defense, Ambulatory Surgical Centers & Specialty Clinics), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Automated CPR Devices Market Trends and Insights

Rising OHCA Incidence and Persistently Low Survival Rates Drive Adoption of CPR Adjuncts

Global out-of-hospital cardiac arrest (OHCA) survival to discharge remained below 10% through 2025, prompting care systems to test adjuncts that minimize pauses during airway management, vascular access, or defibrillation. In the United States, the CARES registry reported 9.1% survival for all-rhythm arrests, while Ireland documented 8.0% survival across 2,746 cases, 53% of which used mechanical CPR. A Vienna dataset echoed the challenge with 9.3% survival, reinforcing the need for devices that sustain perfusion during inevitable hands-off periods. Tehran University researchers demonstrated a 14.1-percentage-point absolute improvement in return of spontaneous circulation when LUCAS-3 replaced the manual technique, underscoring why tertiary centers embed mechanical CPR in refractory-arrest algorithms. Collectively, these findings point to a durable demand driver for the Automated CPR devices market among systems seeking incremental gains in neurologically intact survival.

Growing EMS and Hospital Use for Transport, Cath Lab PCI, and Prolonged Resuscitation Codes

Catheterization laboratories now treat ongoing arrest with simultaneous percutaneous coronary intervention, a practice linked to 51% return of spontaneous circulation and 26% good neurological outcome in a Swedish cohort. Mechanical devices maintain diastolic pressures above 30 mmHg, safeguarding cerebral perfusion while guidewires advance. Air-medical fleets logged over 600 CPR transports in 2025, compelling Air Methods to standardize AutoPulse NXT across its aircraft to keep crew members restrained during turbulence. Ground agencies facing 30-mile interfacility transfers followed suit. Such operational realities cement the Automated CPR devices market as a transport-critical technology rather than a mere in-station convenience.

Clinical Guidelines Discourage Routine Use; Selective Indications Only

ILCOR's 2025 Consensus issued a weak recommendation against routine mechanical CPR after six randomized trials showed no survival benefit in unselected arrests, a conclusion echoed by AHA and the European Resuscitation Council. Canada's technology-assessment agency added concerns over fracture risk and absent cost-effectiveness data, prompting budget committees to delay large-scale procurement. Consequently, many purchasers now restrict devices to transport, catheterization labs, or limited-personnel cases, trimming near-term volumes in the Automated CPR devices market even as niche demand persists.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Battery-Powered Mechanical CPR for Transport Consistency and Crew Safety

- Rural EMS Staffing Gaps and Aging Volunteer Workforce Elevate Device Adoption Need

- High Total Cost of Ownership (Device, Consumables, Training, Maintenance)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Piston systems commanded 68.90% of the automated CPR devices market share in 2025 and are projected to expand at an 8.93% CAGR through 2031. The architecture's motorized plunger consistently delivers 102 compressions per minute at 5.0-5.5 cm depth, a standard difficult to maintain manually for more than 3 minutes. Multi-year service contracts lock hospitals and emergency medical services (EMS) providers into proprietary suction cups and software, creating annuity streams that underpin the automated CPR devices market size for Stryker and its distributors. Load-distributing band rivals such as Zoll's AutoPulse apply circumferential thoracic pressure and claim better perfusion indexes for bariatric patients; nonetheless, trained crews favor piston units' faster setup when seconds matter.

Emerging Chinese manufacturers price comparable piston devices 30-40% below Western incumbents yet face regulatory delays in the United States and Europe, limiting near-term share gain. Corpuls' Bluetooth synchronization, which trims peri-shock pause to 2.00 seconds, illustrates how incremental feature gains can win tenders in highly scrutinized European markets.

Geography Analysis

North America retains the largest installed base, translating to 41.90% of 2025 revenue, yet guideline restraint and cost-effectiveness debates temper growth in the forecasted period. High-profile contracts, such as the Los Angeles Fire Department's USD 9.4 million monitor procurement that deliberately excluded mechanical devices, illustrate selective spending. In contrast, Europe is posting the fastest 8.78% CAGR on the back of protocol harmonization across 24 of 27 member states and rising cross-border funding for cardiology centers.

Asia-Pacific lags in penetration but not ambition, with China's 2023 clinician survey revealing a transition from manual to mechanical CPR during prolonged codes despite limited device availability. Domestic innovation, typified by Korea's ROSCER prototype, could localize supply and accelerate the diffusion of Automated CPR devices in the region. Middle East and Africa, along with South America, accounted for less than a modest share of revenue in 2025; however, Qatar's registry-reported mechanical CPR rate demonstrates niche pockets of high uptake, albeit with mixed survival outcomes.

- Ambulanc (Shenzhen) Tech.

- GS Elektromedizinische Gerate G. Stemple GmbH

- CU Medical Systems, Inc.

- Defibtech

- Codex Healthcare

- Henan Meisong Medical

- Michigan Instruments

- Resuscitation International

- Schiller

- Shenzhen Bangvo Technology

- Stryker

- SunLife Science

- ZOLL Medical Corportation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising OHCA and Low Survival Drive Adoption of CPR Adjuncts

- 4.2.2 Shift To Battery-Powered mCPR for Transport and Consistency

- 4.2.3 Growing EMS/Hospital Use for Transport, Cath Lab, Prolonged Codes

- 4.2.4 Product Refresh Cycles and Launches Expand Installed Base

- 4.2.5 Air Medical Transport Standardization for Uninterrupted CPR

- 4.2.6 Rural EMS Staffing Gaps Elevate Device Adoption Need

- 4.3 Market Restraints

- 4.3.1 Guidelines Discourage Routine Use; Selective Indications Only

- 4.3.2 High Total Cost of Ownership (Device + Consumables + Training)

- 4.3.3 Reliability/Recall Risks Disrupt Service and Confidence

- 4.3.4 Improper Use Can Delay First Shock/Medication In EMS

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Piston-driven (piston/arm)

- 5.1.2 Load-distributing band (vest)

- 5.2 By Power Source

- 5.2.1 Battery-electric

- 5.2.2 Pneumatic/oxygen-driven

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 EMS Providers

- 5.3.3 Military & Defense

- 5.3.4 Ambulatory Surgical Centers & Specialty Clinics

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Ambulanc (Shenzhen) Tech.

- 6.3.2 GS Elektromedizinische Gerate G. Stemple GmbH

- 6.3.3 CU Medical Systems, Inc.

- 6.3.4 Defibtech LLC

- 6.3.5 Codex Healthcare

- 6.3.6 Henan Meisong Medical

- 6.3.7 Michigan Instruments

- 6.3.8 Resuscitation International

- 6.3.9 SCHILLER AG

- 6.3.10 Shenzhen Bangvo Technology

- 6.3.11 Stryker Corporation

- 6.3.12 SunLife Science

- 6.3.13 ZOLL Medical Corportation

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment