PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063655

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063655

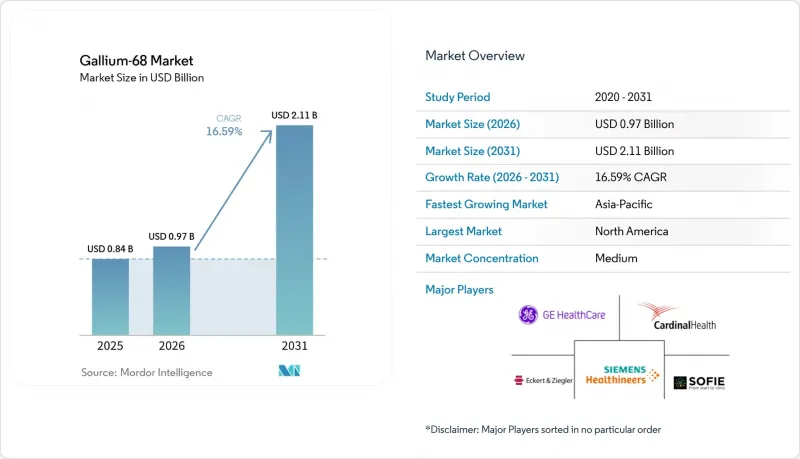

Gallium-68 - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the gallium-68 market size is expected to grow from USD 0.84 billion in 2025 to USD 0.97 billion in 2026 and is forecast to reach USD 2.11 billion by 2031 at 16.59% CAGR over 2026-2031.

This report is Segmented by Production Route (Generator-Produced, Cyclotron-Produced), Product (Ge-68/Ga-68 Generators, PSMA-11 Cold Kits, and More), Radiopharmaceutical/Indication (Prostate Cancer Imaging, NET Imaging, FAPI Imaging), End User (Hospitals, Imaging Centers, Radiopharmacies), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Value (USD).

Global Gallium-68 Market Trends and Insights

PSMA PET Adoption Accelerated by Approvals and Guideline Endorsements

Multiple 2025 regulatory milestones converted PSMA PET from optional to standard practice in staging and recurrence assessment. Telix's Gozellix gained FDA clearance in March 2025 with a six-hour shelf life that lets radiopharmacies batch morning syntheses for afternoon scans, trimming labor costs 15-20%. NCCN Prostate Cancer Guidelines v1.2025 elevated PSMA PET to Category 1 evidence for high-risk disease, expanding eligible U.S. patients by roughly 40%. Japan's simultaneous approval of Locametz, GalliaPharm, and Pluvicto created a reimbursed theranostic pathway priced at JPY 550,000 (USD 3,700) per scan. China accepted the Illuccix NDA in January 2026 on the strength of a 94.8% positive-predictive study in more than 134,000 annual cases, setting the stage for a late-2026 launch. U.S. procedure volumes topped 350,000 in 2024, a 30% jump that underscores payer adoption.

Sustained Demand from SSTR Imaging in NETs

Ga-68 DOTATATE and DOTATOC maintain a stable revenue base because neuroendocrine tumor (NET) incidence continues to rise in aging populations and because Lu-177 DOTATATE therapy requires serial diagnostic scans before and during treatment. A 2025 Chinese comparative study confirmed that Ga-68 DOTATATE outperforms F-18 FDG for well-differentiated NET detection, reinforcing physician preference for somatostatin-receptor tracers. Longitudinal operating data from the University of Parma show roughly 610 DOTATOC batches through 2024, proving that SSTR use remains robust even as PSMA volumes surge. The isotope's 68-minute half-life aligns with somatostatin analog pharmacokinetics, yielding high lesion-to-background ratios within an hour of injection. That clinical efficiency anchors shipments when PSMA supply is disrupted, cushioning overall market revenue during competitive cycles.

Competition from F-18 PSMA Agents with Wider Distribution

Lantheus' Pylarify TruVu, approved in March 2026, exploits F-18's 110-minute half-life to supply imaging centers up to 500 miles away, creating a structural cost and reach advantage over Ga-68 kits. U.S. uptake exceeded 760,000 scans by 2024, and larger 20-dose syntheses lower per-patient costs roughly 25-30%. Installed F-18 cyclotrons already outnumber Ga-68 generators four-to-one, letting hospitals add PSMA labeling with little incremental capital. Switzerland's 2025 approval of Pylclari signals a pending wave of European entrants. As more F-18 competitors secure reimbursement, Ga-68 conversion in rural areas may plateau near 60-70% of the PSMA opportunity.

Other drivers and restraints analyzed in the detailed report include:

- Greater Availability of Higher-Activity Generators Expands Access

- Cyclotron-Produced Ga-68 Scaling Augments Supply Capacity

- Short Half-Life and Generator Logistics/Quality-Control Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Generator-based supply retained 82.18% of the Gallium-68 market in 2025, but cyclotron activity is rising at an 18.76% CAGR as networks deploy ARTMS QIS and IBA Cyclone platforms capable of over 5,000 mCi per two-hour run. That scale supports 40-50 patient doses, driving down per-dose costs and expanding the practical service radius to 200 miles. Generator lines still suit academic centers managing 2-4 daily scans; the recently approved 100 mCi GalliaPharm unit lifts daily elutions from three to ten, preserving relevance where on-site throughput matters. Sichuan University's 3.26 GBq TiO2 generator prototype shows that academic R&D continues to push generator ceilings.

The cyclotron build-out also diversifies supply risk that once hinged on three German-designed generator brands, a vulnerability exposed by Eckert & Ziegler's 2025 cyberattack. Radiopharmacies view dual-isotope production as a hedge: a single facility can mint both FDG and Ga-68 doses, amortizing capital faster than single-nuclide sites. Hospitals, meanwhile, gain flexibility, generators for low-volume days, cyclotron deliveries for peak PSMA clinics, without breaching radiation licensing caps. Overall, increasing route optionality underpins resilience in the Gallium-68 market.

PSMA-11 cold kits accounted for 44.38% of 2025 revenue, but the shipment of radiopharmacy-prepared doses is escalating 19.15% annually as facilities outsource labeling to specialized compounders. Telix's purchase of RLS added 31 pharmacies and vertically integrated everything from eluate to courier van, capturing both kit and service margin. Six-hour shelf-life Gozellix further supports morning synthesis for afternoon deliveries, smoothing courier logistics across multi-state regions. In contrast, hospitals that keep generators in-house shoulder USP 825/797 sterility workflows, daily Ge-68 breakthrough checks, and media-fill validations, burdens that radiopharmacies spread across high volume.

SSTR cold kits for neuroendocrine tumors remain a resilient niche; NETSPOT and DOTATOC enjoy stable reimbursement and continue to anchor demand where PSMA volumes have yet to dominate. The near-term pipeline suggests a similar adoption curve for FAPI kits: academic hospitals will label in-house through Phase III trials, then migrate to outsourced doses once payers codify procedure codes. This gradual pivot toward service-based delivery reinforces the service revenue stream inside the Gallium-68 market.

Geography Analysis

North America generated 48.19% of 2025 revenue as hospitals executed more than 350,000 PSMA PET scans and as the NCCN upgrade boosted guideline-driven demand. Telix strengthened vertical control by acquiring RLS Radiopharmacy Solutions, adding 31 sites that synchronize generator elution, cyclotron output, and last-mile couriers. Cardinal Health operates more than 130 nuclear pharmacies, 110 of which hold Ga-68 licenses, underpinning same-day delivery across most U.S. metropolitan clusters. Canada added Locametz in 2023, while Mexico's PET/CT fleet exceeded 50 cameras by 2025, although limited radiopharmacy density tempers penetration outside primary cities. Lantheus' Pylarify TruVu approval now provides an F-18 alternative that may capture rural demand where Gallium-68 logistics remain challenging.

Asia-Pacific advances at a 21.65% CAGR as Japan approved Locametz, Pluvicto, and 100 mCi generators in September 2025 and set reimbursement at JPY 550,000 (USD 3,700) per scan across 108 hospitals. China's NMPA accepted the Illuccix NDA in January 2026, backed by a pivotal trial showing 94.8% positive predictive value in over 134,000 annual prostate-cancer cases, and the country's PET/CT install base passed 1,600 cameras in 2025, positioning it for rapid uptake.

Europe retains a generator-centric model anchored by university hospitals; Eckert & Ziegler's 100 mCi GalliaPharm approval doubled daily elutions and mitigated backlog risk after its 2025 cyberattack disrupted shipments for several weeks. Although GCC states and Brazil invest in PET infrastructure, limited radiopharmacy networks restrict Gallium-68 to urban hubs; in these regions, F-18's longer half-life currently offers broader coverage.

- ABX advanced biochemical compounds GmbH

- ARTMS

- Cardinal Health

- COMECER

- Curium Pharma

- Eckert & Ziegler Radiopharma GmbH

- Elysia-Raytest

- GE Healthcare

- IBA Radiopharma Solutions

- IRE ELiT

- Isologic Radiopharm

- Isotope Technologies Garching

- Jubilant Radiopharma

- NovartisAG

- PharmaLogic

- RLS Radiopharmacies

- SCINTOMICS

- Siemens Healthineers

- SOFIE Biosciences

- Telix Pharmaceuticals Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 PSMA PET Adoption Accelerated by Approvals and Guideline Endorsements

- 4.2.2 Sustained Demand from SSTR Imaging in Nets (DOTATATE/DOTATOC)

- 4.2.3 Greater Availability of Higher-Activity Ga-68 Generators Expands Access

- 4.2.4 Cyclotron-Produced Ga-68 Scaling Augments Supply Capacity

- 4.2.5 Emerging FAPI Tracers Broaden Ga-68 Use Across Tumor Types

- 4.2.6 Radiopharmacy Network Expansion Enabling National Ga-68 Kit Labeling

- 4.3 Market Restraints

- 4.3.1 Competition From F-18 PSMA Agents With Wider Distribution

- 4.3.2 Short Half-Life and Generator Logistics/QC Constraints

- 4.3.3 Concentrated Ge-68 Supply and Cost Pressures

- 4.3.4 GMP/Aseptic and QC Complexity for Ga-68 Kit Labeling

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Production Route

- 5.1.1 Generator-produced Ga-68

- 5.1.2 Cyclotron-produced Ga-68

- 5.2 By Product

- 5.2.1 Ge-68/Ga-68 Generators

- 5.2.2 PSMA-11 Cold Kits (Ga-68 gozetotide)

- 5.2.3 SSTR Cold Kits (Ga-68 DOTATATE/DOTATOC)

- 5.2.4 Ready-to-use Patient Doses (radiopharmacy prepared)

- 5.3 By Radiopharmaceutical / Indication

- 5.3.1 Prostate Cancer Imaging (Ga-68 PSMA-11)

- 5.3.2 Neuroendocrine Tumor Imaging (Ga-68 SSTR)

- 5.3.3 Fibroblast Activation Protein Imaging (Ga-68 FAPI)

- 5.4 By End User

- 5.4.1 Hospitals & Academic Medical Centers

- 5.4.2 Independent Imaging Centers

- 5.4.3 Centralized Radiopharmacies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 ABX advanced biochemical compounds GmbH

- 6.3.2 ARTMS

- 6.3.3 Cardinal Health

- 6.3.4 COMECER

- 6.3.5 Curium

- 6.3.6 Eckert & Ziegler Radiopharma GmbH

- 6.3.7 Elysia-Raytest

- 6.3.8 GE HealthCare

- 6.3.9 IBA Radiopharma Solutions

- 6.3.10 IRE ELiT

- 6.3.11 Isologic Radiopharm

- 6.3.12 Isotope Technologies Garching

- 6.3.13 Jubilant Radiopharma

- 6.3.14 NovartisAG

- 6.3.15 PharmaLogic

- 6.3.16 RLS Radiopharmacies

- 6.3.17 SCINTOMICS

- 6.3.18 Siemens Healthineers

- 6.3.19 SOFIE Biosciences

- 6.3.20 Telix Pharmaceuticals Limited

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment