PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063666

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063666

AI-Powered Software Testing And QA - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

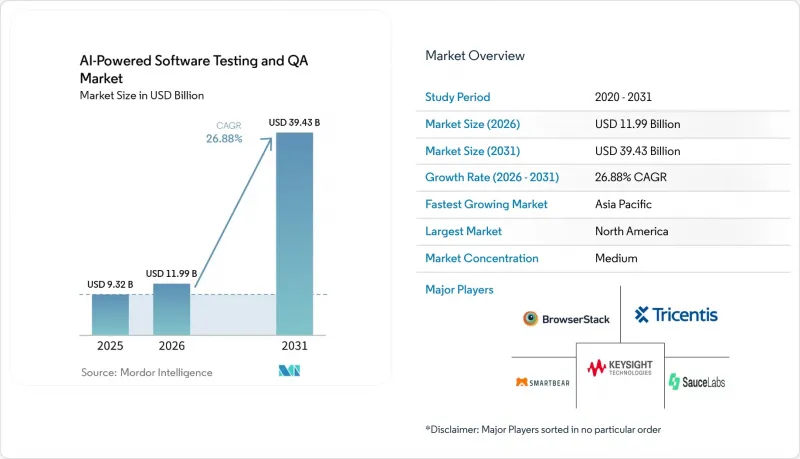

According to Mordor Intelligence, the aI-powered software testing and QA market size is expected to grow from USD 9.32 billion in 2025 to USD 11.99 billion in 2026 and is forecast to reach USD 39.43 billion by 2031 at a 26.88% CAGR over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, and On-Premise), Testing Type (Functional Testing, Performance Testing, Security Testing, Regression Testing, and More), End-User Industry (IT and Telecom, BFSI, Healthcare and Life Sciences, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global AI-Powered Software Testing And QA Market Trends and Insights

Mainstream Adoption of Continuous Testing Pipelines

Organizations embed quality gates inside CI/CD workflows so that code, infrastructure, and security controls are validated in a single transaction. After a series of critical zero-day exploits, 61% of enterprises now run AI test engines across every development stage, slashing release cycles from weeks to hours. Europe's NIS2 Directive builds on this momentum by requiring incident-response drills for essential service operators, making continuous testing a compliance prerequisite. Automated test-selection algorithms further reduce redundant executions by allocating compute budgets to the riskiest code paths.

Rising Complexity of Microservices Architectures

A single cloud system can contain hundreds of loosely coupled services; validating the thousands of possible API pairs is beyond the capacity of manual validation. AI-powered contract-testing tools auto-generate interaction stubs from OpenAPI specs, reducing inter-service defect rates by 40% in production studies. Telecommunications providers deploying 5G core networks view such tooling as essential to meet sub-10 ms latency thresholds. Service-mesh routing adds still more variability, forcing chaos-engineering platforms to inject controlled failures so teams can observe cascade effects in real time.

Data Privacy Concerns in Test-Data Lakes

Copying production data into non-production environments violates GDPR Article 25, a lapse that triggered average fines of EUR 2.1 million (USD 2.24 million) during a 2025 enforcement sweep. Synthetic-data generators like Synthesized use differential privacy algorithms to create statistically rich, yet anonymized, datasets. Yet distribution drift remains a hurdle, especially in financial crime detection, where subtle graph patterns matter. Confidential computing enclaves encrypt data in use, though the latency overhead makes them impractical for high-throughput performance testing.

Other drivers and restraints analyzed in the detailed report include:

- Growing Cloud-Native Application Deployments

- Increasing Regulatory Emphasis on Software Reliability

- Shortage of Skilled AI Testing Professionals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services accounted for 36.79% of 2025 revenue yet are projected to climb at a 27.28% CAGR, outpacing software subscriptions. Implementation partners increasingly design synthetic-data pipelines and monitor self-healing test bots for drift. Pharmaceutical firms outsource validation of clinical-trial platforms to certified specialists who maintain FDA Part 11 and EU Annex 11 credentials, illustrating how compliance drives services uptake. In contrast, commoditization pressure weighs on generic test-automation licenses as hyperscalers embed baseline capabilities into their platforms. Even so, niche software modules for chaos engineering or edge-device validation retain pricing power.

The AI-powered software testing and QA market size for software platforms remains significant, driven by the increasing adoption of advanced technologies across industries. Embedded analytics, which provide detailed explanations of model actions to auditors, play a crucial role in maintaining enterprise renewal rates by ensuring transparency and compliance. However, a persistent skills deficit in the market compels organizations to enter into multi-year managed-testing agreements, thereby shifting a significant portion of their budget toward service providers. This scenario highlights a dual trend, such as services are expected to gain momentum even as autonomous agents and automation technologies continue to evolve and mature.

Cloud platforms captured 72.48% of 2025 revenue, reflecting the economics of spinning up thousands of browser instances simultaneously. Elastic grids slash capital outlays once required for on-premise device farms, and usage-based billing aligns cost with demand peaks. The AI-powered software testing and QA market for cloud deployments is expanding steadily, but latency-sensitive automotive and aerospace workloads still rely on air-gapped rigs to meet safety standards. As a result, enterprises adopt hybrid topologies, running functional suites in the cloud while reserving performance and security testing for local infrastructure that complies with data-sovereignty laws.

Vendor roadmaps now prioritize seamless artifact portability, ensuring that a failing test executed in the cloud can be replayed on an on-premise bench without any loss of telemetry data. This capability allows organizations to maintain consistency and accuracy in their testing processes across different environments. Additionally, the adoption of consumption-based pricing models has introduced budget unpredictability, prompting procurement teams to advocate for monthly spending caps to manage costs effectively. As a result, organizations' deployment strategies have evolved significantly. It is no longer a binary choice between cloud and on-premises solutions; most large enterprises are adopting a hybrid approach that integrates public, private, and edge computing resources to optimize performance and flexibility.

Geography Analysis

North America remains the revenue epicenter, driven by hyperscaler ecosystems and a dense concentration of software start-ups. Procurement budgets increasingly favor vendors that seamlessly integrate with mature DevSecOps toolchains and offer explainability dashboards, which corporate governance committees highly seek after. However, despite maintaining its lead, rising infrastructure energy costs in North America are prompting enterprises to shift AI inference workloads to more cost-efficient regions. This shift is creating opportunities for Asia-Pacific providers to expand their market presence and capture a larger share of the global market.

Asia-Pacific is emerging as the fastest-growing region, with a remarkable 27.52% CAGR, driven by a combination of aggressive digital government initiatives, efforts to achieve semiconductor self-sufficiency, and a rapidly expanding pool of AI research talent. Governments in countries like India and Singapore are actively funding AI testbeds to foster innovation, while Chinese firms are heavily investing in hardware-in-the-loop rigs to support the development of home-grown chips. The replication of successful practices across industries such as telecommunications, banking, and the public sector is further accelerating the adoption of autonomous testing solutions throughout the region.

Europe continues to grow at a steady pace, supported by increasingly stringent regulatory frameworks. The EU AI Act's conformity procedures are driving demand for certified third-party validation services, creating a niche market where local consultancies are thriving. Additionally, the continent's strict data-protection laws have positioned Europe as an early adopter of synthetic-data platforms, which are gaining traction across various industries. Meanwhile, the Middle East and Africa are focusing on smart-city initiatives and autonomous-transit pilot projects, often relying on imported expertise to address skill shortages in these areas. In South America, adoption is progressing at a slower pace, but Brazil's burgeoning fintech sector demonstrates how localized regulations, such as compliance with instant-payment schemes, can stimulate targeted bursts of demand and drive growth in specific market segments.

- Tricentis GmbH

- SmartBear Software, Inc.

- Applitools Ltd.

- Sauce Labs, Inc.

- LambdaTest, Inc.

- Mabl Inc.

- Functionize, Inc.

- ACCELQ Inc.

- Parasoft Corporation

- Eggplant Software Ltd.

- Keysight Technologies, Inc.

- Cigniti Technologies Limited

- Qualitest Group Ltd.

- Mindful QA, LLC

- Test IO Inc.

- Rainforest QA Inc.

- Leapwork A/S

- Testsigma Technologies Inc.

- BrowserStack Limited

- Perfecto Mobile Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream Adoption of Continuous Testing Pipelines

- 4.2.2 Rising Complexity of Microservices Architectures

- 4.2.3 Growing Cloud-Native Application Deployments

- 4.2.4 Increasing Regulatory Emphasis on Software Reliability

- 4.2.5 Shift Toward Autonomous Testing Agents

- 4.2.6 Emergence of Synthetic Data Generation for QA

- 4.3 Market Restraints

- 4.3.1 Data Privacy Concerns in Test-Data Lakes

- 4.3.2 Shortage of Skilled AI Testing Professionals

- 4.3.3 Opaque Black-Box AI Model Decisions

- 4.3.4 Limited Benchmarking Standards for AI QA Tools

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.3 By Testing Type

- 5.3.1 Functional Testing

- 5.3.2 Performance Testing

- 5.3.3 Security Testing

- 5.3.4 Regression Testing

- 5.3.5 Other Testing Types

- 5.4 By End-user Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Retail and E-commerce

- 5.4.5 Manufacturing

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Tricentis GmbH

- 6.4.2 SmartBear Software, Inc.

- 6.4.3 Applitools Ltd.

- 6.4.4 Sauce Labs, Inc.

- 6.4.5 LambdaTest, Inc.

- 6.4.6 Mabl Inc.

- 6.4.7 Functionize, Inc.

- 6.4.8 ACCELQ Inc.

- 6.4.9 Parasoft Corporation

- 6.4.10 Eggplant Software Ltd.

- 6.4.11 Keysight Technologies, Inc.

- 6.4.12 Cigniti Technologies Limited

- 6.4.13 Qualitest Group Ltd.

- 6.4.14 Mindful QA, LLC

- 6.4.15 Test IO Inc.

- 6.4.16 Rainforest QA Inc.

- 6.4.17 Leapwork A/S

- 6.4.18 Testsigma Technologies Inc.

- 6.4.19 BrowserStack Limited

- 6.4.20 Perfecto Mobile Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment