PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063692

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063692

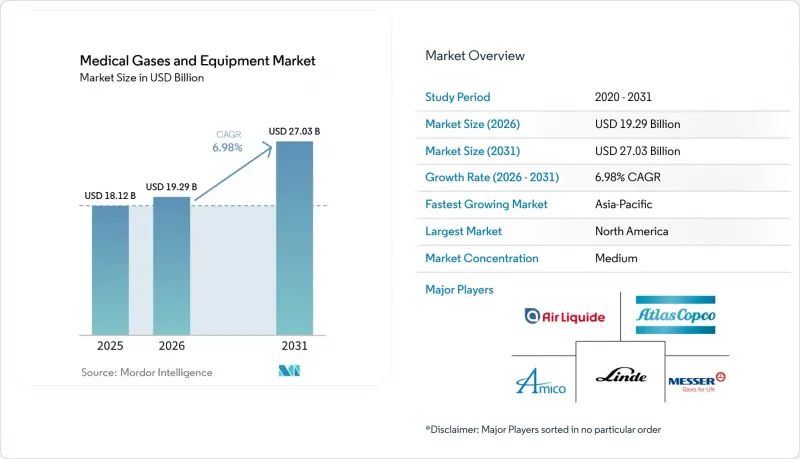

Medical Gases And Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the medical gases and equipment market size is projected to be USD 18.12 billion in 2025, USD 19.29 billion in 2026, and reach USD 27.03 billion by 2031, growing at a CAGR of 6.98% from 2026 to 2031.

This report is Segmented by Product Type (Medical Gases, Medical Gas Equipment), Gas Type (Oxygen, Nitrous Oxide, Medical Air, CO2, Nitrogen, Helium & Others), Equipment Type (Cylinders, Pipelines, Manifolds, Vacuum Systems, Monitoring Systems), Application (Therapeutic, Diagnostic, Pharmaceutical), End User (Hospitals, Ascs, and More), and Geography. Market Forecasts are in Value (USD).

Global Medical Gases And Equipment Market Trends and Insights

Rapid Rise in Chronic Respiratory Diseases

Global COPD and asthma cases climbed to 569.2 million in 2025, yet age-standardized COPD mortality declined 30% between 2000 and 2019. Longer survival is driving millions of dollars into continuous home oxygen therapy, especially in regions with limited refill infrastructure. Europe logged 81.7 million respiratory cases in 2024, with COPD representing 32 million. South Asian and African patients experience an earlier onset due to indoor biomass smoke exposure, pushing governments to subsidize stationary and portable concentrators.

Aging Population Boosting Long-Term Oxygen Therapy

People aged 65 years and older accounted for 10% of the world's population in 2024 and will reach 16% by 2050. A 2024 meta-analysis showed that using oxygen for more than 15 hours daily extends hypoxemic COPD survival by 3.5 years. Japan expanded coverage for nocturnal oxygen therapy in 2025, adding roughly 120,000 eligible patients. Lightweight 2-kilogram devices with 8-hour batteries improve adherence among frail seniors and underpin growth in the medical gases and equipment market.

Stringent Purity & Safety Regulations

USP and Ph.Eur. require 99.5% oxygen purity and moisture below 67 ppm, forcing hospitals to install inline analyzers that cost USD 15,000-25,000 each. Quarterly pipeline testing adds USD 8,000-12,000 in annual overhead for a 200-bed facility. Divergent rules between China's NMPA and overseas markets add up to USD 80,000 per product line and six-month delays, slowing new device launches.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Surgical & Diagnostic Procedures

- Home-Healthcare Shift Driving Portable Equipment Demand

- Global Helium Shortage Affecting Specialty Gases

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medical gases generated 56.02% of the medical gases and equipment market revenue in 2025, and this segment is forecast to grow at 7.87% annually through 2031. Persistent COPD therapy, wider helium demand in imaging, and PSA cost advantages keep consumption recurring even as reimbursement tightens. In contrast, equipment sales lag because pipelines, manifolds, and monitors last 15-20 years and are increasingly bundled into procedural payments. Nonetheless, IoT-enabled manifolds are extending service revenue and anchoring buyers to premium brands, a dynamic that supports overall expansion of the medical gases and equipment market.

Specialty gases such as nitrous oxide, carbon dioxide, and medical air command premium prices due to purity controls. Nitrous oxide must reach 99% purity, whereas medical air compressors must achieve -40 °C dew points. Suppliers are embedding predictive maintenance sensors that cut downtime 25% and push hospitals toward multiyear service contracts. Those advances sustain margins even as competitive bidding intensifies.

Oxygen led with 34.27% of 2025 revenue, but helium & others will outpace all gases at 10.73% CAGR as MRI operators retrofit recovery systems and shift to conduction-cooled magnets. The medical gases and equipment market size for helium recovery and helium-free MRI is forecast to reach USD 1.8 billion by 2030. Nitrous oxide usage tracks the 6.2% rise in global surgical volumes, while carbon dioxide mirrors laparoscopic adoption at 7.8% growth in 2025. Converters moving to energy-efficient oxygen concentrators in home care reduce liquid oxygen consumption but create a backfill of demand for high-purity oxygen in neonatal and hyperbaric applications.

Geography Analysis

North America accounted for 41.78% of 2025 revenue, supported by USD 2.1 billion in Medicare and Medicaid outlays for home oxygen equipment. FDA 510(k) clearances for sub-2-kilogram concentrators hit 47 in 2025, highlighting a robust innovation cadence. Section 301 tariffs, ranging from 7.5% to 25%, are prompting U.S. assemblers to source valves from Mexico, although longer lead times test just-in-time models. Canadian provinces are piloting remote oxygen monitoring, with Ontario reporting a 22% reduction in emergency visits in a 2025 trial.

Europe's demand benefits from strict ISO 7396-1 compliance requirements and the EMA's 2025 Annex 1 revision, which mandates real-time oxygen monitoring. Germany, the U.K., France, Italy, and Spain together create more than 60% of regional volume. The U.K.'s HTM 02-01 guidance obliges annual pipeline integrity tests costing up to USD 13,000 per hospital. Carbon Border Adjustment levies, effective 2026, will add EUR 4-7 per imported cylinder, nudging buyers toward lighter composite models.

Asia-Pacific is the fastest-growing region, albeit from a lower base, at a 11.57% CAGR through 2031. China's plan to add 500,000 beds by 2027 and mandate PSA plants in 40% of new hospitals channels vast capex into local generation. India's Ayushman Bharat program expanded insurance coverage to 550 million citizens by late 2025, boosting oxygen demand in tier-2 cities. Japan's aging society is fueling a surge in nocturnal oxygen therapy, and South Korea raised portable concentrator reimbursement by 8% in 2025.

Middle East & Africa and South America remain smaller but are investing in resilience. Saudi Arabia is spending USD 12 billion to boost hospital capacity by 25% and requires ISO-compliant PSA systems in new builds. In 2025, South Africa purchased 1,200 concentrators for rural clinics. Brazil's SUS added home oxygen coverage for 180,000 COPD patients, yet reimbursement trails private insurers by 35%, limiting equipment uptake.

- Air Liquide S.A.

- Air Products and Chemicals

- Amico Corporation

- Atlas Copco

- Caire

- Chart Industries

- Dragerwerk

- GCE Group

- Gulf Cryo

- Invacare

- Linde plc

- Matheson Tri-Gas

- Messer SE & Co. KGaA

- Norco Inc.

- Ohio Medical

- Philips Healthcare (Respironics)

- Resmed

- Rotarex S.A.

- SOL Group

- Taiyo Nippon Sanso Corp.

- Teijin Pharma Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Rise in Chronic Respiratory Diseases

- 4.2.2 Aging Population Boosting Long-Term Oxygen Therapy

- 4.2.3 Expansion of Surgical & Diagnostic Procedures

- 4.2.4 Home-Healthcare Shift Driving Portable Equipment Demand

- 4.2.5 On-Site Generation/PSA Plants Adoption in Emerging Hospitals

- 4.2.6 Miniaturization of Portable/ Wearable Concentrators & Sensors

- 4.3 Market Restraints

- 4.3.1 Stringent Purity & Safety Regulations

- 4.3.2 Global Helium Shortage Affecting Specialty Gases

- 4.3.3 High Cap-Ex for Pipeline & Manifold Installations

- 4.3.4 Tariff-Driven Supply-Chain Volatility for Equipment Components

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Medical Gases

- 5.1.2 Medical Gas Equipment

- 5.2 By Gas Type

- 5.2.1 Oxygen

- 5.2.2 Nitrous Oxide

- 5.2.3 Medical Air

- 5.2.4 Carbon Dioxide

- 5.2.5 Nitrogen

- 5.2.6 Helium & Others

- 5.3 By Equipment Type

- 5.3.1 Cylinders & Tanks

- 5.3.2 Pipelines & MGPS

- 5.3.3 Manifolds & Regulators

- 5.3.4 Vacuum & Compressor Systems

- 5.3.5 Monitoring & Alarm Systems

- 5.4 By Application

- 5.4.1 Therapeutic

- 5.4.2 Diagnostic & Imaging

- 5.4.3 Pharmaceutical Manufacturing & Research

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Ambulatory Surgical Centers

- 5.5.3 Home Healthcare Settings

- 5.5.4 Academic & Research Institutions

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Air Liquide S.A.

- 6.3.2 Air Products and Chemicals Inc.

- 6.3.3 Amico Corporation

- 6.3.4 Atlas Copco AB

- 6.3.5 CAIRE Inc.

- 6.3.6 Chart Industries Inc.

- 6.3.7 Dragerwerk AG & Co. KGaA

- 6.3.8 GCE Group

- 6.3.9 Gulf Cryo

- 6.3.10 Invacare Corporation

- 6.3.11 Linde plc

- 6.3.12 Matheson Tri-Gas

- 6.3.13 Messer SE & Co. KGaA

- 6.3.14 Norco Inc.

- 6.3.15 Ohio Medical

- 6.3.16 Philips Healthcare (Respironics)

- 6.3.17 ResMed Inc.

- 6.3.18 Rotarex S.A.

- 6.3.19 SOL Group

- 6.3.20 Taiyo Nippon Sanso Corp.

- 6.3.21 Teijin Pharma Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment