PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063738

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063738

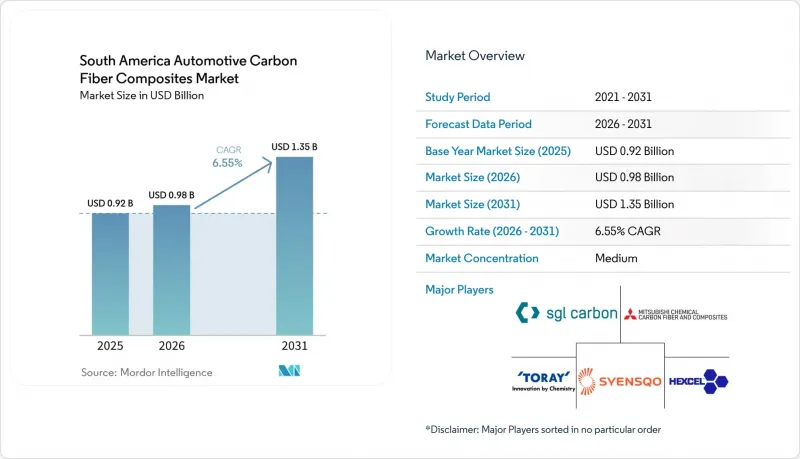

South America Automotive Carbon Fiber Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the south america automotive carbon fiber composites market size is projected to expand from USD 0.92 billion in 2025 and USD 0.98 billion in 2026 to USD 1.35 billion by 2031, registering a CAGR of 6.55% between 2026 to 2031.

This report is Segmented by Production Type (Resin Transfer Molding, Hand Layup, Vacuum Infusion Processing, and Injection Molding), Application Type (Structural Assemblies, Powertrain Components, and More), Vehicle Type (Passenger Cars and Commercial Vehicles), and Geography (Brazil, Argentina, and More). The Market Forecasts are Provided in Terms of Value (USD).

South America Automotive Carbon Fiber Composites Market Trends and Insights

ICE-to-EV Lightweighting Push

Battery-electric platforms carry a 300-400 kg mass penalty versus internal-combustion counterparts, which erodes range unless chassis weight drops. Every 10% curb-weight cut extends EV range by 6-8%, and carbon fiber delivers 50-60% savings against steel in body panels and 30-35% against aluminum in structural nodes. Integrated press-molding that cures roof panels in under five minutes demonstrates the productivity gains now possible, making continuous-fiber parts viable once annual volumes pass 15,000 units. Latin American passenger-car demand is set to rise past 9 million units by 2035, so OEM platforms engineered for lightweighting today will bank scale benefits later. Early commercial success is visible in Brazil, where electric trucks that haul pulp for Suzano show how mass savings can raise payload without breaching axle limits.

Stringent Regional CO2 Fleet Targets

Brazil's Programa de Controle da Poluicao do Ar por Veiculos Automotores (PROCONVE) L-8 caps fleet-average emissions at 101 g CO2/km by 2028, backed by penalties of BRL 150 per excess gram per vehicle. Automakers will incur material-neutral fines unless mass reductions offset combustion or battery penalties, so composite hoods, roof panels, and tailgates are climbing priority lists. Argentina rolled out a similar framework in 2024, though its enforcement remains uneven because currency controls complicate prepreg imports. The Mercosur-EU pact overlays lifecycle-carbon accounting on export models, nudging OEMs toward recycled fiber streams and bio-based resins that carry published environmental product declarations.

High Carbon-Fiber Cost and Precursor Price Spikes

Carbon fiber trades at USD 15-30 per kg, many multiples above steel and aluminum, because PAN precursor forms more than half of the final production cost. Petrobras prioritized acrylic fiber over export precursor in 2025, which lifted spot PAN pricing 21% inside six months. Since a ton of fiber consumes up to 30,000 kWh, Brazil's industrial power tariff adds nearly USD 2,700 to production cost, deterring local carbonization. Chinese large-tow grades are lower on a free-on-board basis, yet a 35% antidumping duty blocks easy arbitrage inside the bloc.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Sustainable Materials

- Domestic-Content Rules Within Mercosur Bloc

- Skills Shortage in Advanced-Composite Processing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Injection molding's 6.95% CAGR through 2031 shows how servo-driven presses and in-mold coatings are scaling toward 50,000 parts per year. Syensqo's Fibreject process supports short-fiber thermoplastic housings that drop cycle times below two minutes, a critical gate for high-volume sedans in the South America automotive carbon fiber composites market. In contrast, resin transfer molding held 40.87% South America automotive carbon fiber composites market share in 2025. Hand Layup persists in low-volume bus and truck parts where tool amortization stays minor, but rising Brazilian wage inflation narrows its cost edge.

Vacuum Infusion splits the difference, with mid-volume battery enclosures molded in 4-8 hours and tooling costs half that of autoclaves. Toray's next-gen press-molding could displace RTM for roof panels by 2030 if local fiber cost hurdles fall. Demand for Injection Molding aligns with passenger-car electrification because lower part cost offsets the battery premium. Producers betting on automated fiber placement still need a domestic tow-spreading line to lock in feedstock security, reinforcing the strategic case for upstream integration.

List of Companies Covered in this Report:

- 3M

- ACTION COMPOSITES

- Aksa Carbon

- Carbon Revolution

- Formosa Plastics Corporation

- Hexcel Corporation

- Mitsubishi Chemical Carbon Fiber and Composites, Inc.

- Mubea CarboTech

- Owens Corning

- Plasan North America

- SGL Carbon

- Syensqo

- TEIJIN Ltd.

- TORAY INDUSTRIES, INC.

- Voith Composites

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 ICE-to-EV lightweighting push

- 4.2.2 Stringent regional CO2-fleet targets

- 4.2.3 Government incentives for sustainable materials

- 4.2.4 Domestic-content rules within Mercosur bloc

- 4.2.5 Modular battery-pack designs demanding CFRP enclosures

- 4.3 Market Restraints

- 4.3.1 High carbon-fiber cost and precursor price spikes

- 4.3.2 Skills shortage in advanced-composite processing

- 4.3.3 Limited acrylonitrile precursor availability regionally

- 4.3.4 Uncertain Brazilian import tariff policy on PAN fibers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Production Type

- 5.1.1 Resin Transfer Molding

- 5.1.2 Hand Layup

- 5.1.3 Vacuum Infusion Processing

- 5.1.4 Injection Molding

- 5.2 By Application Type

- 5.2.1 Structural Assemblies

- 5.2.2 Power-train Components

- 5.2.3 Interiors

- 5.2.4 Exteriors

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Colombia

- 5.4.4 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 ACTION COMPOSITES

- 6.4.3 Aksa Carbon

- 6.4.4 Carbon Revolution

- 6.4.5 Formosa Plastics Corporation

- 6.4.6 Hexcel Corporation

- 6.4.7 Mitsubishi Chemical Carbon Fiber and Composites, Inc.

- 6.4.8 Mubea CarboTech

- 6.4.9 Owens Corning

- 6.4.10 Plasan North America

- 6.4.11 SGL Carbon

- 6.4.12 Syensqo

- 6.4.13 TEIJIN Ltd.

- 6.4.14 TORAY INDUSTRIES, INC.

- 6.4.15 Voith Composites

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment