PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063743

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063743

Skin Resurfacing Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

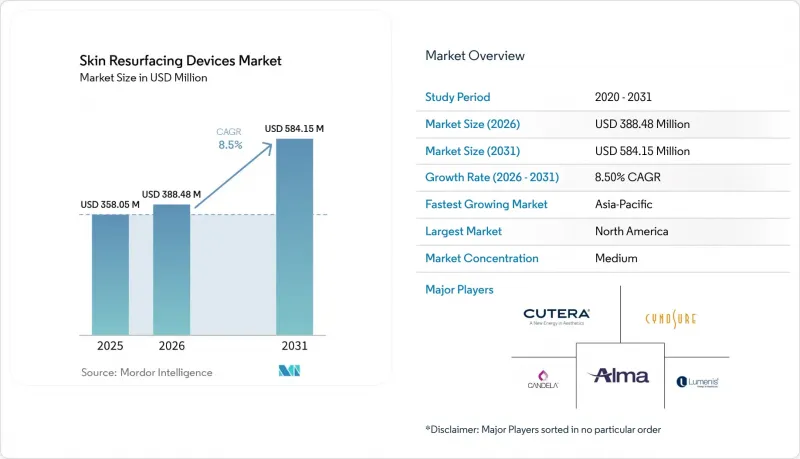

According to Mordor Intelligence, the skin resurfacing devices market size is projected to be USD 358.05 million in 2025, USD 388.48 million in 2026, and reach USD 584.15 million by 2031, growing at a CAGR of 8.5% from 2026 to 2031.

This report is Segmented by Product (Laser Resurfacing Devices, RF Microneedling Systems, and More), Technology (Ablative, Non-Ablative), Application (Wrinkle & Fine-Line Reduction, Melasma, Skin Tightening & Texture Improvement and More), End User (Dermatology Clinics, Hospitals, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Skin Resurfacing Devices Market Trends and Insights

Aging-driven demand for minimally-invasive aesthetics

Global population aging accelerates interest in procedures that rejuvenate appearance without surgical downtime. The Aesthetic Society recorded a 14% increase in nonsurgical aesthetic procedures from 2020 to 2024, underscoring durable demand. Fractional CO2 lasers further validate this preference by delivering superior scar management when used within one month post-surgery, according to peer-reviewed studies. Improved safety profiles encourage older patients to seek preventive care earlier, reinforcing long-term procedure adoption.

Surge in combination treatments (laser + RF microneedling)

Pairing fractional lasers with radiofrequency microneedling lifts collagen stimulation while moderating epidermal damage. A four-and-a-half-year safety review found no adverse events when RF microneedling was combined with cosmetic injectables, highlighting the modality's versatility. Manufacturers now embed both energies in single consoles, enabling clinics to offer multi-effect sessions that reduce overall chair time and boost revenue per patient.

High capital cost of laser workstations

Professional-grade resurfacing consoles cost USD 100,000-500,000 before maintenance and training outlays. Upcoming U.S. Quality System Regulation Amendments effective 2026 will further lift compliance expenditure, raising manufacturer list prices[1]. Smaller practices therefore delay purchases or opt for lower-priced single-energy tools, slowing penetration in cost-sensitive locales

Other drivers and restraints analyzed in the detailed report include:

- Rising male consumer adoption of cosmetic procedures

- Rapid expansion of medical-spa chains in Asia-Pacific

- Limited reimbursement for aesthetic indications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Laser resurfacing devices generated 42.78% of 2024 revenue, keeping them the commercial anchor of the skin resurfacing market. They benefit from broad clinical familiarity and premium price points that lift average selling prices. RF microneedling systems, however, are projected to grow at a 9.16% CAGR, reflecting clinician enthusiasm for shorter downtime and versatile protocols. AI-enabled depth control enables practitioners to match energy delivery to dermal thickness, thereby improving safety for individuals with darker skin phenotypes. The combined momentum positions RF units as central to incremental demand even as lasers preserve headline revenue status.

Platform integration also advances. Multimodal workstations now combine fractional laser, bipolar RF, and IPL in a single footprint, enabling clinics to add services without requiring multiple capital purchases. As bundled consoles roll out, the skin resurfacing market gains resilience because purchasers can serve a broader range of indications from a single asset.

Ablative systems held a 56.10% revenue share in 2024, a testament to their proven efficacy in deep scar revision and the treatment of pronounced rhytides. They command higher treatment prices, sustaining device ROI. Non-ablative platforms, in contrast, are expected to expand at a 9.57% CAGR as patients value weekend-length recovery windows and reduced risk of post-inflammatory hyperpigmentation. Advanced 1550 nm fractional lasers stimulate dermal collagen without vaporizing surface tissue, enabling lip and perioral rejuvenation for working professionals.

Hybrid solutions blur traditional boundaries: temperature-modulated CO2 lasers deliver fractional patterns that limit thermal diffusion, merging ablative precision with non-ablative safety. Such convergence reinforces the skin resurfacing market as manufacturers differentiate through parameter flexibility rather than energy type alone.

Geography Analysis

North America generated the largest 36.89% share of the skin resurfacing market in 2024, driven by high disposable incomes, a dense network of providers, and a robust training infrastructure. The region's medical-spa count surpassed 10,000 outlets, with average site revenue of USD 1.398 million. FDA rule changes slated for 2026 will standardize quality systems and diversify clinical trial cohorts, potentially increasing development costs but enhancing public confidence once approvals are obtained.

Asia-Pacific is on course for a 10.93% CAGR, outpacing all other regions. Urban millennials in China, Japan, and South Korea are allocating a growing portion of their discretionary income to preventive aesthetics; 91% of high-income Chinese consumers either maintained or increased their spending on cosmetic procedures in 2024. National regulators in South Korea and Singapore fast-track device clearance when domestic manufacturing is involved, accelerating market entry for local innovators. With the broader regional med-tech sector projected to reach USD 190 billion by 2025, suppliers are prioritizing distributor partnerships and localized education to convert latent demand.

Europe delivers steady mid-single-digit growth anchored by stringent safety culture and a well-insured patient base. Demand also reflects environmental stewardship; clinics in Germany and the Nordics increasingly specify low-consumable handpieces to meet internal ESG goals. South America and the Middle East & Africa remain emerging but compelling. Brazil's long-standing cosmetic culture sustains procedure tourism, while Saudi Arabia's approval of Cytrellis's Micro-Coring platform signals policy support for device-based aesthetics. Collectively, these geographies provide expansion corridors that diversify manufacturer revenue beyond core Western markets.

- Aerolase

- Aerolase

- Alma Sisram Medical

- Alma Lasers

- Asclepion Laser

- Bausch Health - Solta Medical

- Bison Medical

- BTL

- Candela Medical

- Cutera

- Cutera Japan K.K.

- Cynosure

- DEKA M.E.L.A.

- Fotona

- Jeisys Medical

- Lumenis

- Lutronic

- Sciton

- Shanghai Fosun Pharmaceutical - Sisram

- Sharplight Technologies

- Candela Medical

- Venus Concept

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging-Driven Demand for Minimally-Invasive Aesthetics

- 4.2.2 Surge in Combination Treatments (Laser + RF Microneedling)

- 4.2.3 Rising Male Consumer Adoption of Cosmetic Procedures

- 4.2.4 Rapid Expansion of Medical-Spa Chains in Asia-Pacific

- 4.2.5 AI-Guided Laser Platforms Improving Treatment Outcomes

- 4.2.6 ESG-Linked Preference for Low-Consumable Devices

- 4.3 Market Restraints

- 4.3.1 High Capital Cost of Laser Workstations

- 4.3.2 Stringent Device Safety Regulations & Lengthier Approvals

- 4.3.3 Limited Reimbursement for Aesthetic Indications

- 4.3.4 Growing Popularity of Home-Use Resurfacing Gadgets

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Laser Resurfacing Devices

- 5.1.2 RF Microneedling Systems

- 5.1.3 Microdermabrasion Devices

- 5.1.4 Chemical Peel Solutions & Kits

- 5.2 By Technology

- 5.2.1 Ablative

- 5.2.2 Non-Ablative

- 5.3 By Applications

- 5.3.1 Wrinkle & Fine-Line Reduction

- 5.3.2 Scar & Acne-Scar Revision

- 5.3.3 Hyper-Pigmentation / Melasma

- 5.3.4 Skin Tightening & Texture Improvement

- 5.4 By End User

- 5.4.1 Dermatology Clinics

- 5.4.2 Hospitals

- 5.4.3 Medical Spas & Aesthetic Centers

- 5.4.4 Home-Use / Consumer

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Aerolase

- 6.3.2 Aerolase Corporation

- 6.3.3 Alma Sisram Medical

- 6.3.4 Alma Lasers

- 6.3.5 Asclepion Laser

- 6.3.6 Bausch Health - Solta Medical

- 6.3.7 Bison Medical

- 6.3.8 BTL Aesthetics

- 6.3.9 Candela Medical

- 6.3.10 Cutera

- 6.3.11 Cutera Japan K.K.

- 6.3.12 Cynosure

- 6.3.13 DEKA M.E.L.A.

- 6.3.14 Fotona

- 6.3.15 Jeisys Medical

- 6.3.16 Lumenis

- 6.3.17 Lutronic

- 6.3.18 Sciton

- 6.3.19 Shanghai Fosun Pharmaceutical - Sisram

- 6.3.20 Sharplight Technologies

- 6.3.21 Syneron Medical

- 6.3.22 Venus Concept

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment