PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063754

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063754

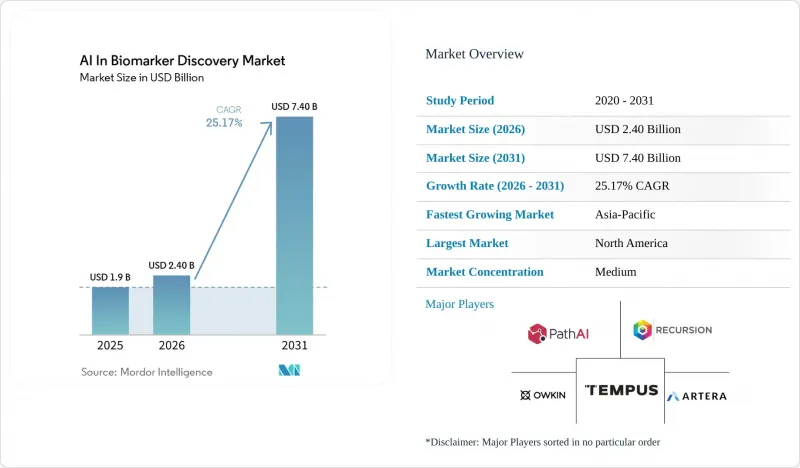

AI In Biomarker Discovery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the aI in biomarker discovery market size is expected to grow from USD 1.9 billion in 2025 to USD 2.40 billion in 2026 and is forecast to reach USD 7.40 billion by 2031 at 25.17% CAGR over 2026-2031.

This report is Segmented by Data Modality (Genomics, Transcriptomics, and More), Disease Area (Oncology, Immunology/Inflammation, and More), AI Approach (Supervised/Classical ML, and More), Biomarker Type (Predictive, and More), End User (Biopharma, and More), Deployment Model (Cloud/SaaS, Hybrid, and More), and Geography (North America, and More). Market Forecasts are Provided in Value (USD).

Global AI In Biomarker Discovery Market Trends and Insights

Oncology-Led Precision Medicine Demand

Clinical practices are increasingly adopting AI-driven molecular subtyping over traditional histopathology. In 2025, the FDA approved 17 oncology AI biomarker tests, up from 9 in 2024. Of these, 12 focused on immunotherapy responses, while 5 targeted minimal residual disease. Whole-slide imaging combined with spatial transcriptomics now achieves an 82% positive predictive value for predicting checkpoint-inhibitor efficacy, a 14-point improvement over traditional PD-L1 staining. Liquid-biopsy panels, with a sensitivity of 1 ppm in detecting circulating tumor DNA, are growing at an annual rate of 31%, driven by their ability to replace invasive biopsies. Additionally, multi-omic panels have significantly reduced discovery timelines from 36 months to under a year, enhancing the protection of drug-patent life.

Expansion of Multi-Omics Datasets and Digital Pathology

High-resolution scanners now archive gigapixel images at a cost-effective rate, enabling hospitals to utilize their archived slide libraries. Single-cell RNA sequencing has advanced to process 1 million cells per run, while spatial platforms map 5,000 genes per cell, uncovering localized niches that bulk profiling often misses. Large-scale initiatives, such as those in the UK and China, are projected to add 1.5 million genomes this decade, strengthening the ability to detect rare-variant associations. Plasma-proteome assays, capable of quantifying 7,000 proteins from minimal sample volumes, are narrowing the functional gap between transcriptomics and proteomics.

Data Silos, Privacy, and Cross-Border Data Transfer Limits

Multi-national data pooling remains uncertain due to regulations such as GDPR, PIPL, and the fragile EU-US Data Privacy Framework. Hospitals increasingly treat omics archives as competitive assets, while re-identification studies indicate that 83% of "anonymized" genomes can be traced, leading to stricter terms for data usage. In the biomarker discovery market, where deployments depend on extensive training datasets, differential-privacy noise can reduce AUROC by up to seven points at stringent epsilon levels. This creates a trade-off between compliance and utility, slowing AI advancements in the sector.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Tailwinds (FDA BQP; Evolving AI/ML SaMD Guidance)

- Cloud/SaaS-Native Analytics and Scalable Compute

- Analytical/Clinical Validation Burden Under IVDR and LDT Reforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Genomics accounted for 35.12% of the revenue, solidifying its foundational role in precision oncology. Meanwhile, Transcriptomics, driven by single-cell and spatial methods, is advancing with a 28.16% CAGR. As per-cell costs decrease below USD 0.10, Transcriptomics is expected to close the gap with Genomics. The integration of these two modalities is uncovering causal signals previously overlooked, driving the growth of AI in the biomarker discovery market, particularly for multi-omic platforms.

Paige's Virchow2 demonstrated that unlabeled slide archives can be utilized to develop models for rare cancers. This indicates that pathology images could play a significant role in providing weak labels for future multimodal pipelines. However, fewer than 5% of cancer patients currently have fully matched genomic, transcriptomic, proteomic, and metabolomic profiles, which limits comprehensive foundation-model training.

Oncology accounted for 43.18% of the 2025 expenditure, reflecting the emphasis on biomarker-guided therapy approvals and the complexity of tumor heterogeneity. Rare disorders are experiencing strong growth at a 29.61% CAGR, driven by sponsors increasingly adopting synthetic cohorts and federated registries to address the challenges of small patient populations. These strategies matured in late 2024 and are now scaling across the AI in biomarker discovery market.

Immunology applications are benefiting from single-cell RNA-seq techniques that effectively profile T-cell clonotypes. In contrast, cardiometabolic projects remain underdeveloped due to reimbursement processes lagging behind oncology by approximately two years. However, with AI-driven polygenic-risk engines achieving a 0.75 AUROC for 10-year cardiovascular predictions, this segment is positioned for significant growth once payer codes are introduced.

Geography Analysis

In 2025, North America accounted for 43.16% of the revenue, driven by the expansion of the NIH's "All of Us" cohort and Medicare's coverage of multi-cancer early-detection tests. A strong flow of venture capital and the FDA's expedited PCCP pathway enable startups to maintain a competitive edge, reinforcing the region's leadership in the AI-driven biomarker discovery market.

Asia-Pacific, supported by significant investments such as China's USD 9.2 billion Precision Medicine Initiative and the rise of AI-focused diagnostic ventures in India, is projected to grow at a robust 30.08% CAGR through 2031. The implementation of data-sovereignty laws is accelerating the adoption of privacy-preserving machine learning and federated computing, driving innovation in product development. Additionally, Japan's alignment with FDA guidelines for 2025 simplifies dual-filing strategies for global developers.

Europe is experiencing steady growth, although the IVDR's stringent evidence requirements pose challenges. Meanwhile, genomics projects in the Gulf Cooperation Council and AI-based tuberculosis screening initiatives in Brazil highlight how emerging markets are rapidly adopting AI in biomarker applications. While these regions currently contribute less than 15% of the total revenue, they represent high-growth opportunities as infrastructure development progresses.

- ArteraAI

- Caris Life Sciences Inc.

- ConcertAI

- Foundation Medicine (Roche)

- Freenome

- GeneDx

- GRAIL

- Guardant Health

- Ibex Medical Analytics

- Imagene AI

- Immunai

- Insitro

- Lunit

- nference

- Owkin Inc.

- Paige

- PathAI Inc.

- Recursion

- SOPHiA GENETICS

- Tempus AI, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 arket Drivers

- 4.2.1 Oncology-Led Precision Medicine Demand

- 4.2.2 Expansion of Multi-Omics Datasets and Digital Pathology

- 4.2.3 Regulatory Tailwinds (FDA BQP; Evolving AI/ML Samd Guidance)

- 4.2.4 Cloud/Saas-Native Analytics and Scalable Compute

- 4.2.5 Federated Learning Unlocking Cross-Institution Discovery

- 4.2.6 Multimodal Foundation Models Linking Omics-Imaging Clinical

- 4.3 Market Restraints

- 4.3.1 Data Silos, Privacy, and Cross-Border Data Transfer Limits

- 4.3.2 Analytical/Clinical Validation Burden Under IVDR And LDT Reforms

- 4.3.3 Batch Effects and Assay Drift Causing Model Non-Stationarity

- 4.3.4 Explainability and Lifecycle Change Control (PCCP) for AI Biomarkers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Data Modality

- 5.1.1 Genomics (WES/WGS, targeted panels)

- 5.1.2 Transcriptomics (bulk, single-cell)

- 5.1.3 Proteomics

- 5.1.4 Metabolomics/Lipidomics

- 5.1.5 Epigenomics

- 5.1.6 Others

- 5.2 By Disease Area

- 5.2.1 Oncology (solid and hematologic)

- 5.2.2 Immunology/Inflammation

- 5.2.3 Cardiometabolic (CVD, diabetes, NASH)

- 5.2.4 Neurology/Neurodegeneration

- 5.2.5 Infectious Diseases

- 5.2.6 Rare/Genetic Disorders

- 5.2.7 Others

- 5.3 By AI Approach

- 5.3.1 Supervised and Classical ML

- 5.3.2 Deep Learning (CNNs/RNNs/Transformers)

- 5.3.3 Self-/weakly-supervised and Transfer Learning

- 5.3.4 Foundation Models (pathology, radiology, omics)

- 5.3.5 Graph and Network-based ML

- 5.3.6 Others

- 5.4 By Bimarker Type

- 5.4.1 Predictive Biomarkers

- 5.4.2 Prognostic Biomarkers

- 5.4.3 Safety Biomarkers

- 5.4.4 Surrogate Endpoints

- 5.4.5 Other Types

- 5.5 By End User

- 5.5.1 Biopharma and Biotech Sponsors

- 5.5.2 Diagnostics and CDx Developers

- 5.5.3 Contract Research/Central Labs

- 5.5.4 Academic and Research Institutes

- 5.5.5 Others

- 5.6 By Deployment / Access Model

- 5.6.1 Cloud/SaaS

- 5.6.2 Hybrid

- 5.6.3 On-premises

- 5.6.4 Federated/Edge Deployments

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East & Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 ArteraAI

- 6.3.2 Caris Life Sciences Inc.

- 6.3.3 ConcertAI

- 6.3.4 Foundation Medicine (Roche)

- 6.3.5 Freenome

- 6.3.6 GeneDx

- 6.3.7 GRAIL

- 6.3.8 Guardant Health

- 6.3.9 Ibex Medical Analytics

- 6.3.10 Imagene AI

- 6.3.11 Immunai

- 6.3.12 Insitro

- 6.3.13 Lunit

- 6.3.14 nference

- 6.3.15 Owkin Inc.

- 6.3.16 Paige

- 6.3.17 PathAI Inc.

- 6.3.18 Recursion

- 6.3.19 SOPHiA GENETICS

- 6.3.20 Tempus AI, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment