PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063831

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063831

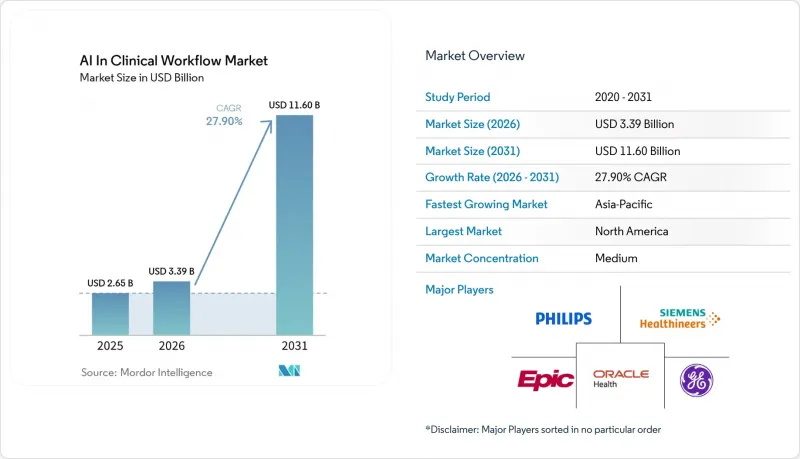

AI In Clinical Workflow - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the aI in clinical workflow market size is expected to grow from USD 2.65 billion in 2025 to USD 3.39 billion in 2026 and is forecast to reach USD 11.60 billion by 2031 at 27.90% CAGR over 2026-2031.

This report is Segmented by Component (Software, and More), Deployment Model (Cloud-Based, On-Premise), Application (Patient Scheduling & Throughput, and More), End User (Hospitals & Health Systems, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global AI In Clinical Workflow Market Trends and Insights

Accelerated EHR-AI Integration by Top EMR Vendors

Leading EHR systems now incorporate native AI functionalities. Epic's Art for Clinicians generates progress notes from in-room conversations, queues medication orders, and condenses discharge summaries, reducing administrative workloads by nearly one-third at early adopter sites. Oracle Health's Clinical AI Agent, integrated into emergency departments, has recorded encounters and saved physicians approximately 200,000 hours. Embedding AI directly at the point of care eliminates log-in delays, accelerates system-wide implementation, and establishes a competitive standard.

Shift to Value-Based Care Driving Workflow Automation

With over half of U.S. reimbursements tied to value-based contracts, healthcare providers are increasingly required to predict risks, address documentation gaps, and demonstrate outcomes. AI platforms streamline these processes by consolidating claims, lab results, and social-determinant data, then automating outreach and care-gap tasks. Providers and payers have reported up to an 80% reduction in prior-authorization turnaround times and significant increases in revenue from Hierarchical Condition Category (HCC) codes flagged by AI. These financial benefits have transitioned AI from an experimental tool to a budgeted necessity.

Interoperability Gaps Among Legacy Hospital IT Stacks

Many community hospitals continue to operate decade-old EHR modules that lack modern application-programming interfaces. Integrating AI requires either custom interfaces or expensive middleware, which delays implementation and increases the total cost of ownership. Vendors have introduced orchestration layers to standardize image routing and results delivery using HL7 and DICOM; however, significant gaps remain, particularly in settings where multiple best-of-breed systems coexist. These slower deployments reduce operational efficiency and limit short-term growth potential.

Other drivers and restraints analyzed in the detailed report include:

- Chronic Disease Burden and Aging Populations Drive Virtual Nursing Assistant Adoption

- FDA Regulatory Pathways Accelerate AI Workflow-Tool Market Entry

- Data-Privacy Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, software accounted for 63.98% of the revenue in the AI in Clinical Workflow market, showcasing the scalability of cloud subscriptions and the minimal costs incurred post-algorithm training. Leading platforms such as Abridge, Viz.ai, and Oracle Health Clinical AI Agent, when integrated into existing EHR workflows, offer near-instant functionality, ensuring a swift return on investment. Conversely, services are witnessing a robust growth rate of 28.77% CAGR, driven by hospitals' needs for implementation expertise, model-performance audits, and bias monitoring. Highlighting the importance of trustworthy AI, third-party assessors now provide continuous-validation dashboards that are presented to board-level risk committees. This underscores the necessity of ongoing human oversight in AI applications.

Service vendors play a pivotal role in workforce training. Given that only a fraction of clinical staff possess formal data-science skills, hospitals are turning to packaged boot camps and on-call AI "help desk" support. These services are not just add-ons; they are reshaping post-go-live maintenance from a once-internal challenge to a streamlined, predictable subscription model, aligning seamlessly with health systems' shift towards operating-expense frameworks.

In 2025, cloud solutions dominated the spending landscape, capturing 75.66% of the market share. With providers increasingly valuing elasticity and vendor-managed compliance, cloud solutions are projected to grow at a robust 28.16% CAGR. Typically, a cloud rollout can be initiated within weeks, often starting with a pilot in a single nursing unit before expanding enterprise-wide. Providers are charged per clinician, with fees ranging from USD 100 to 300 monthly, a model that CFOs favor over hefty multi-million-dollar capital investments.

On-premise installations remain vital in scenarios where latency is critical, such as in acute stroke or pulmonary embolism triage. Data-localization mandates in regions like China and select EU states necessitate localized GPU clusters. Yet, vendors are increasingly offering cloud-style automated updates and monitoring packages, blurring the distinctions between deployment types and ensuring on-premise growth aligns with the broader AI in Clinical Workflow market trajectory.

Geography Analysis

In 2025, North America accounted for 45.12% of total revenue, with over 27% of U.S. health systems investing in commercial AI licenses, which is three times the average for enterprise software. Federal grants, along with clear FDA pathways for Software as a Medical Device, accelerate pilot programs and reduce risks associated with vendor selection. Canadian provinces are collaborating with national AI institutes to develop open-source clinical decision-support models, ensuring broader access beyond major urban areas.

Europe, while demonstrating strong EHR penetration, enforces stringent governance measures. The upcoming EU AI Act categorizes diagnostic algorithms as high-risk, requiring conformity assessments and continuous oversight. Providers are accepting these costs as AI agents assist in achieving sustainability and staffing objectives. In 2026, leading German networks implemented radiology triage across multiple trusts after completing cross-border data protection impact assessments.

Asia-Pacific is experiencing the fastest growth, driven by government-supported "AI-first" digital health strategies. China's "Healthy China 2030" and Japan's "Healthcare DX" initiatives are allocating funds to public-cloud AI for rural imaging and chronic disease management. Local vendors are partnering with global firms to develop language-specific natural language processing models. Additionally, state payers are reimbursing virtual nursing services in both high-density metropolitan areas and remote counties.

- Abridge

- Aidoc

- Butterfly Network

- Cleerly

- CloudMedx

- Epic Systems

- GE Healthcare

- Komodo Health

- Koninklijke Philips

- Lumeon

- Notable Health

- Nuance (Microsoft)

- Olive AI

- Oracle Health

- Qure.ai

- RapidAI

- Siemens Healthineers

- Suki AI

- Tempus AI

- Viz.ai

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated EHR?AI Integration by Top EMR Vendors

- 4.2.2 Shift to Value-Based Care Driving Workflow Automation

- 4.2.3 Chronic-Disease Patient Load Boosting Virtual Nursing Assistants

- 4.2.4 FDA's TAP Voluntary Sprint Fast-Tracks Workflow AI Tools

- 4.2.5 Rise of Ambient Clinical Documentation for Rural Hospitals

- 4.2.6 Gen-AI Copilots Embedded in RIS/PACS Upgrade Cycles

- 4.3 Market Restraints

- 4.3.1 Interoperability Gaps among Legacy Hospital IT Stacks

- 4.3.2 Data-Privacy Compliance Costs (HIPAA, GDPR, Brazil LGPD)

- 4.3.3 GPU Allocation Shortages Inside Hospital Private-Clouds

- 4.3.4 Physician Guild Resistance to Fully Autonomous Triage

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.3 Hardware

- 5.2 By Deployment Model

- 5.2.1 Cloud-based

- 5.2.2 On-premise

- 5.3 By Application

- 5.3.1 Patient Scheduling & Throughput

- 5.3.2 Clinical Decision Support

- 5.3.3 Diagnostic Imaging Workflow

- 5.3.4 Medication Management

- 5.3.5 Virtual Nursing Assistants

- 5.3.6 Others

- 5.4 By End User

- 5.4.1 Hospitals & Health Systems

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Diagnostic Imaging Centers

- 5.4.4 Telehealth Providers

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abridge

- 6.3.2 Aidoc

- 6.3.3 Butterfly Network

- 6.3.4 Cleerly

- 6.3.5 CloudMedx

- 6.3.6 Epic Systems

- 6.3.7 GE HealthCare

- 6.3.8 Komodo Health

- 6.3.9 Koninklijke Philips N.V

- 6.3.10 Lumeon

- 6.3.11 Notable Health

- 6.3.12 Nuance (Microsoft)

- 6.3.13 Olive AI

- 6.3.14 Oracle Health

- 6.3.15 Qure.ai

- 6.3.16 RapidAI

- 6.3.17 Siemens Healthineers AG

- 6.3.18 Suki AI

- 6.3.19 Tempus AI

- 6.3.20 Viz.ai

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment