PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063833

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063833

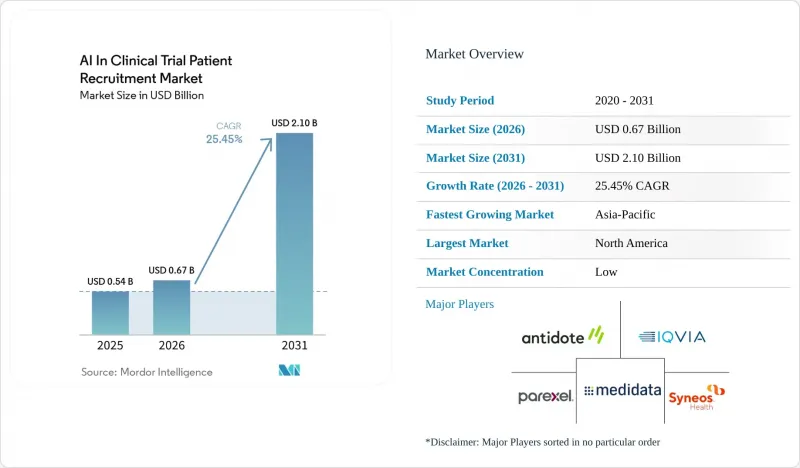

AI In Clinical Trial Patient Recruitment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the aI in clinical trial patient recruitment market size is expected to grow from USD 0.54 billion in 2025 to USD 0.67 billion in 2026 and is forecast to reach USD 2.10 billion by 2031 at 25.45% CAGR over 2026-2031.

This report is Segmented by AI Technology (Machine Learning, NLP, Predictive Analytics, Computer Vision), Deployment (Cloud, On-Premises, Hybrid), Trial Phase (I, II, III, IV), Therapeutic Area (Oncology, Cardiovascular, Neurology, Others), End User (Pharma/Biotech, Cros, and More), Data Source (EHR, Genomics, Registries, Wearables), and Geography. Market Forecasts are in Value (USD).

Global AI In Clinical Trial Patient Recruitment Market Trends and Insights

Increasing Complexity and Cost of Patient Enrollment Propel AI Adoption

Manual chart reviews require an average of 44.7 hours per protocol, whereas AI systems can perform the same task in just 2.5 hours with a high accuracy rate of 96%. Enrollment delays remain a significant challenge, with 80% of trials failing to meet their timelines and 50% of sites unable to enroll any patients. To address these inefficiencies, sponsors are increasingly implementing predictive enrollment engines. These advanced systems significantly reduce activation time from 39 days to 14 days and eliminate approximately USD 180,000 in unnecessary overhead costs per site, streamlining the enrollment process and improving overall trial efficiency.

Pandemic-Led Rise of Decentralized and Hybrid Trials Accelerates Infrastructure Investment

Decentralized clinical trials have experienced substantial growth, with spending reaching USD 8.66 billion in 2025 and continuing to rise. AI-driven patient-matching technologies have become integral to these trials, enhancing the efficiency of participant selection. The adoption of telemedicine consent and direct-to-patient drug shipping has expanded the geographic reach of trials, removing the previous 50-mile radius limitation tied to academic centers. Hybrid trials, which combine home-based monitoring with periodic in-person visits, address regulatory safety requirements while simultaneously providing continuous data streams to AI-powered dashboards. This approach ensures compliance with safety standards while leveraging technology to optimize trial operations.

Bias and Cybersecurity Threats Constrain Adoption

Oncology prescreening models exhibit significant accuracy disparities, with up to a 12-percentage-point gap observed across racial subgroups. This has prompted regulatory bodies to emphasize the need for proactive bias assessments to address these discrepancies. Additionally, nearly a quarter of AI platforms lack comprehensive end-to-end encryption, leaving sensitive genomic data vulnerable to breaches. Such vulnerabilities not only compromise data security but also expose organizations to potential regulatory penalties under frameworks like HIPAA or GDPR.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Real-World Data and AI Validation Pathways Creates New Enrollment Opportunities

- Growing EHR Interoperability Enables Scalable Prescreening

- Under-Representation of Minority Cohorts Limits Generalizability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, machine learning captured 45.10% of the AI market share in clinical trial patient recruitment, showcasing its capability to accurately rank site feasibility. Natural-language processing, driven by algorithms proficient in mining free-text notes containing up to 80% of eligibility data, is projected to grow at a robust 26.25% CAGR. The industry is also adopting predictive analytics, a method validated in real-time pilots with oncology sponsors. This approach enables mid-study patient reassignments based on Bayesian analyses.

Second-generation systems utilize synthetic data to strengthen rare-disease cohorts, enhancing model robustness while protecting identifiers. Compliance with AI/ML software guidance adds an estimated USD 800,000 per lifecycle, extending the time to market but significantly increasing trust among cautious pharmaceutical sponsors.

In 2025, cloud platforms accounted for 61.00% of the AI market in clinical trial patient recruitment, as sponsors avoided on-premise GPU expenditures. However, hybrid models are expanding at a 26.86% CAGR, driven by regulations that impose restrictions on cross-border data transfers. The market is witnessing hybrid workflows that retain identifiers on-site while transmitting anonymized eligibility summaries to global dashboards, balancing a 15% latency trade-off for compliance across multiple jurisdictions.

Geography Analysis

North America contributes nearly half of global revenue, driven by 50,000 active investigator sites and extensive FHIR interoperability, which enables vendors to seamlessly integrate into health-system data lakes. The region also benefits from FDA pilots that demonstrate real-time oversight, providing assurance to risk-averse sponsors and accelerating procurement decisions. Additionally, state Medicaid claims engines enhance recruitment efforts by identifying disease events within 72 hours.

Asia-Pacific is the fastest-growing territory. Japan's effective use of generative-AI prescreeners and China's regulation requiring anonymized data to undergo security reviews before crossing borders encourage hybrid deployments. Australia, Singapore, and South Korea are adopting similar frameworks, supported by government grants focused on rare-disease diagnostics, which expand the AI in clinical trial patient recruitment market.

Europe follows, supported by GDPR-compliant architectures. EMA guidance on algorithmic transparency and the upcoming EU AI Act simplify filings across 27 states, reducing compliance costs and enabling mid-sized biotech firms to scale multi-country studies with confidence. Eastern European hospitals are increasingly implementing EHR systems compatible with HL7 FHIR standards, unlocking new patient pools for oncology and cardiology trials.

- AiCure

- Antidote Technologies

- BEKHealth

- Citeline Connect

- Clarify Health

- DataCubed Health

- Deep Lens (Guardant Health)

- Deep6 AI

- Evidation Health

- ICON

- Innoplexus

- IQVIA

- Medidata Solutions

- ObvioHealth

- Oracle Health Sciences

- Parexel International

- Reify Health

- Syneos Health

- TrialSpark

- TrialX

- Unlearn.AI

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Complexity & Cost of Patient Enrolment

- 4.2.2 Pandemic-Led Rise of Decentralized & Hybrid Trials

- 4.2.3 Regulatory Push for Real-World Data & AI Validation Pathways

- 4.2.4 Growing EHR Interoperability Enabling Scalable Pre-Screening

- 4.2.5 Multimodal Genomic-Phenotypic Matching Boosting Accuracy

- 4.3 Market Restraints

- 4.3.1 Data-Privacy & Cybersecurity Concerns Around Patient Data

- 4.3.2 Under-Representation of Minority Cohorts in Training Sets

- 4.3.3 Explainability & Validation Hurdles for AI Algorithms

- 4.3.4 Site-Level Workflow Inertia & Change-Management Friction

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By AI Technology

- 5.1.1 Machine Learning

- 5.1.2 Natural Language Processing

- 5.1.3 Predictive Analytics

- 5.1.4 Computer Vision

- 5.2 By Deployment Model

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Clinical Trial Phase

- 5.3.1 Phase I

- 5.3.2 Phase II

- 5.3.3 Phase III

- 5.3.4 Phase IV (Post-Marketing)

- 5.4 By Therapeutic Area

- 5.4.1 Oncology

- 5.4.2 Cardiovascular

- 5.4.3 Neurology

- 5.4.4 Metabolic Disorders

- 5.4.5 Infectious Diseases

- 5.4.6 Rare Diseases

- 5.4.7 Others

- 5.5 By End User

- 5.5.1 Pharmaceutical & Biotech Sponsors

- 5.5.2 Contract Research Organizations (CROs)

- 5.5.3 Academic Medical Centers

- 5.5.4 Hospital Sites & Investigator Groups

- 5.5.5 Patient Recruitment Agencies

- 5.6 By Data Source

- 5.6.1 Electronic Health Records (EHR)

- 5.6.2 Genomic & Omics Datasets

- 5.6.3 Patient Registries

- 5.6.4 Insurance Claims

- 5.6.5 Wearables & Digital Biomarkers

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East & Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AiCure

- 6.3.2 Antidote Technologies

- 6.3.3 BEKHealth

- 6.3.4 Citeline Connect

- 6.3.5 Clarify Health

- 6.3.6 DataCubed Health

- 6.3.7 Deep Lens (Guardant Health)

- 6.3.8 Deep6 AI

- 6.3.9 Evidation Health

- 6.3.10 ICON plc

- 6.3.11 Innoplexus

- 6.3.12 IQVIA

- 6.3.13 Medidata Solutions

- 6.3.14 ObvioHealth

- 6.3.15 Oracle Health Sciences

- 6.3.16 Parexel

- 6.3.17 Reify Health

- 6.3.18 Syneos Health

- 6.3.19 TrialSpark

- 6.3.20 TrialX

- 6.3.21 Unlearn.AI

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment