PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063838

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063838

Payroll And HR Compliance Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

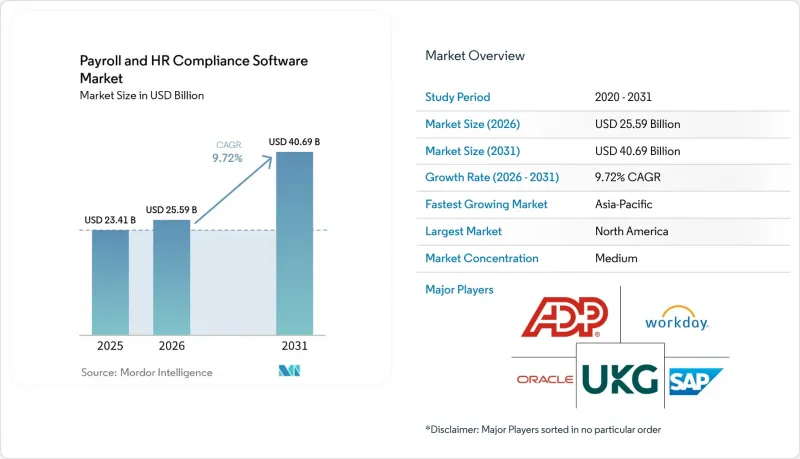

According to Mordor Intelligence, the payroll and HR compliance software market size is projected to expand from USD 23.4 billion in 2025 and USD 25.6 billion in 2026 to USD 40.7 billion by 2031, registering a CAGR of 9.72% between 2026 and 2031.

This report is Segmented by Deployment Model (Cloud, On-Premise, and Hybrid), End User Size (Large Enterprises, and Small and Medium Enterprises), Application (Payroll Processing, HR Compliance, Time and Attendance, and Core HR), Vertical (BFSI, Healthcare, IT and Telecom, Manufacturing, Retail, Government, and More), and Geography. The Market Forecast are Provided in Terms of Value (USD).

Global Payroll And HR Compliance Software Market Trends and Insights

Cloud Adoption by SMEs Accelerating SaaS Payroll Uptake

The payroll and HR compliance software market is seeing one of its clearest demand shifts in the SME segment, where buyers are moving from manual processes and narrow payroll tools to cloud systems that combine payroll, records, and compliance tasks in a single environment. This change matters because smaller firms usually need lower setup effort, faster product updates, and fewer vendor handoffs than large enterprise buyers. In France, 86% of companies used payroll software in 2025, and 62% of employees received digital payslips, indicating how commonplace digital payroll administration has become in a mature SME setting. As more SMEs adopt broader HR platforms, standalone accounting-linked payroll modules become less relevant, as buyers prefer a single workflow for pay, employee records, and compliance actions. The payroll and HR compliance software market, therefore, benefits from a structural shift in buying behavior, not just from short-term software replacement cycles.

Stringent Multi-Country Tax and Labor Compliance Mandates

The payroll and HR compliance software market continues to gain support from compliance mandates that now span pay transparency, payroll documentation, cyber controls, and country-specific labor administration rules. The commercial case becomes stronger when employers manage payroll across several jurisdictions, because rule changes, reporting demands, and local filing practices no longer sit neatly inside one payroll team or one local system. CloudPay reported in late 2025 that more than 36% of organizations now manage payroll across 6 or more countries, underscoring the need for centralized rules and local compliance enforcement within a single platform. This multi-country burden does not act as a one-time trigger, because new country rules and compliance updates continue to arrive after the initial implementation. The payroll and HR compliance software market is therefore being pulled forward by recurring compliance work that employers increasingly want software to manage inside the payroll process itself.

Complexities in Global Data Privacy Regulations

The payroll and HR compliance software market still faces a major restraint from data privacy rules that do not align neatly across countries. Payroll systems handle sensitive employee records, pay details, tax identifiers, and banking data so that each cross-border workflow can trigger extra controls, local review, or product redesign. This becomes harder when one employer runs payroll across multiple countries and expects one system to support both centralized oversight and local legal requirements. Multi-country payroll findings show how common these cross-border operating models have become, indicating that privacy friction now affects a wider share of buyers than in earlier deployment cycles. The payroll and HR compliance software market, therefore, faces slower standardization because vendors often need local hosting choices, regional process logic, and more careful data access design to win multinational clients.

Other drivers and restraints analyzed in the detailed report include:

- AI-Driven Payroll Error Detection and Fraud Prevention

- Integration of Payroll APIs Into Fintech Ecosystems

- High Switching Costs From Legacy ERP Modules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud accounted for 68.4% of revenue in 2025 and is projected to expand at a 10.8% CAGR through 2031, keeping it clearly ahead of on-premises and hybrid options. Cloud, therefore, represented 68.4% of the payroll and HR compliance software market share in 2025, and that lead reflects more than hosting preference alone. Buyers are choosing the cloud because payroll rules change frequently, local requirements vary, and software updates need to move faster than traditional release cycles. In the payroll and HR compliance software market, this model also supports easier rollout across new business units and new country payrolls. On-premises and hybrid deployments still matter for enterprises with heavy ERP customization, strict control requirements, or gradual migration plans.

The remaining deployment mix continues to serve buyers that cannot move all payroll workloads at once, particularly in regulated verticals and multinational groups with uneven country readiness. Hybrid deployments remain useful where firms want cloud speed for new-country payrolls but still want tighter local control for selected data sets or legacy integrations. Third-party certifications, secure hosting, and documented control frameworks have become a basic entry requirement for cloud vendors in Europe and other sensitive regions. That dynamic is narrowing the field of credible providers in the payroll and HR compliance software industry, because smaller vendors need a stronger compliance posture just to stay on the shortlist. The payroll and HR compliance software market is thus becoming more cloud-led, but the migration path still depends on risk tolerance, localization needs, and installed-base complexity.

Large enterprises accounted for 61.7% of revenue in 2025, while SMEs are expected to record the faster 10.4% CAGR through 2031. The large enterprise base still anchors the payroll and HR compliance software market because multi-entity structures, global tax filings, audit demands, and ERP links create higher software intensity per customer. These employers often need deeper workflow control, stronger reporting layers, and closer coordination between payroll and finance systems. SMEs, however, are shifting from the margin of the category to the center of future demand because they now see payroll software as an operating necessity rather than an optional back-office tool. That demand is especially evident among small firms that want a single platform for payroll, employee records, benefits, and compliance.

Growth in the SME segment also reflects a shift in product design, as newer vendors emphasize speed of deployment and lower operational burden rather than heavy configuration. In France, 86% of companies were already using payroll software in 2025, suggesting that adoption can move quickly once the value case becomes clear among SMEs. Challenger vendors are also turning payroll into a platform entry point, then expanding into adjacent services that raise retention and wallet share over time. That cross-sell pattern matters for the payroll and HR compliance software industry because it shifts competition away from simple payroll processing and toward broader workforce administration. The payroll and HR compliance software market should therefore see the SME segment remain the most commercially active buyer group during the forecast period.

Geography Analysis

North America accounted for 38.6% of global revenue in 2025, making it the largest regional market for payroll and HR compliance software. North America, therefore, accounted for 38.6% of the payroll and HR compliance software market share in 2025, led by the United States, which has a dense base of payroll platforms, integrations, and compliance-oriented product demand. The region also benefits from active development in earned wage access, which has become a major adjacent use case for payroll connectivity. In December 2025, it was clarified that covered earned wage access products are not considered credit under Regulation Z, which reduced one important regulatory concern for employer-integrated models. The payroll and HR compliance software market in North America also remains attractive because enterprise clients continue to invest in systems that connect payroll, workforce administration, and employee financial services.

Europe remained the second-largest regional market, with the United Kingdom, Germany, France, and Spain forming the main demand centers. The payroll and HR compliance software market in Europe is shaped by country-specific payroll formats, reporting requirements, and data-handling expectations that require both localization and scale. In France, 86% of companies used payroll software in 2025, and 62% of employees received digital payslips, indicating a mature digital payroll environment with room for validation and upgrade demand. These local requirements make Europe a strong region for vendors that combine multi-country coverage with deep in-country workflow support.

Asia-Pacific is projected to grow at a 12.7% CAGR through 2031, making it the fastest-growing region in the payroll and HR compliance software market. Demand is rising as labor markets formalize, SME digitization spreads, and multinational employers expand deeper into India, Southeast Asia, and Australia. In October 2025, one vendor announced plans to target native payroll coverage in 100+ countries by 2029, which shows how seriously vendors now view in-country capability as a growth lever across fast-moving regions. South America, the Middle East, and Africa are still earlier-stage markets, but adoption is rising as labor law modernization, employer-of-record services, and global HR platform expansion push payroll administration away from manual processes.

- Automatic Data Processing, Inc.

- Paychex, Inc.

- Workday, Inc.

- UKG Inc.

- Ceridian HCM Holding Inc.

- Paylocity Holding Corporation

- Oracle Corporation

- SAP SE

- Intuit Inc.

- Paycom Software, Inc.

- Rippling People Center Inc.

- Gusto, Inc.

- HiBob Inc.

- Deel Inc.

- Papaya Global Ltd.

- BambooHR LLC

- Sage Group plc

- Paycor HCM, Inc.

- Personio

- Ramco Systems Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud Adoption by SMEs Accelerating SaaS Payroll Uptake

- 4.2.2 Stringent Multi-country Tax and Labor Compliance Mandates

- 4.2.3 Integration of Payroll APIs into Fintech Ecosystems

- 4.2.4 Shift Toward On-demand Pay and Earned Wage Access

- 4.2.5 AI-driven Payroll Error Detection and Fraud Prevention

- 4.2.6 Growing Freelancer and Gig Workforce Requiring Agile Payroll

- 4.3 Market Restraints

- 4.3.1 Complexities in Global Data Privacy Regulations

- 4.3.2 High Switching Costs from Legacy ERP Modules

- 4.3.3 Skill Shortage in Payroll Compliance Specialists

- 4.3.4 Resistance to Payroll Process Outsourcing in Regulated Verticals

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-premise

- 5.1.3 Hybrid

- 5.2 By End User Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By Application

- 5.3.1 Payroll Processing

- 5.3.2 Time and Attendance Management

- 5.3.3 HR Compliance and Regulatory Management

- 5.3.4 Benefits and Compensation Administration

- 5.3.5 Core HR and Employee Records Management

- 5.4 By End User Industry Vertical

- 5.4.1 Information Technology (IT) and Telecom

- 5.4.2 Banking, Financial Services and Insurance (BFSI)

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Industrial Manufacturing

- 5.4.5 Retail and eCommerce

- 5.4.6 Government and Public Sector

- 5.4.7 Other End User Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Automatic Data Processing, Inc.

- 6.4.2 Paychex, Inc.

- 6.4.3 Workday, Inc.

- 6.4.4 UKG Inc.

- 6.4.5 Ceridian HCM Holding Inc.

- 6.4.6 Paylocity Holding Corporation

- 6.4.7 Oracle Corporation

- 6.4.8 SAP SE

- 6.4.9 Intuit Inc.

- 6.4.10 Paycom Software, Inc.

- 6.4.11 Rippling People Center Inc.

- 6.4.12 Gusto, Inc.

- 6.4.13 HiBob Inc.

- 6.4.14 Deel Inc.

- 6.4.15 Papaya Global Ltd.

- 6.4.16 BambooHR LLC

- 6.4.17 Sage Group plc

- 6.4.18 Paycor HCM, Inc.

- 6.4.19 Personio

- 6.4.20 Ramco Systems Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment