PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063841

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063841

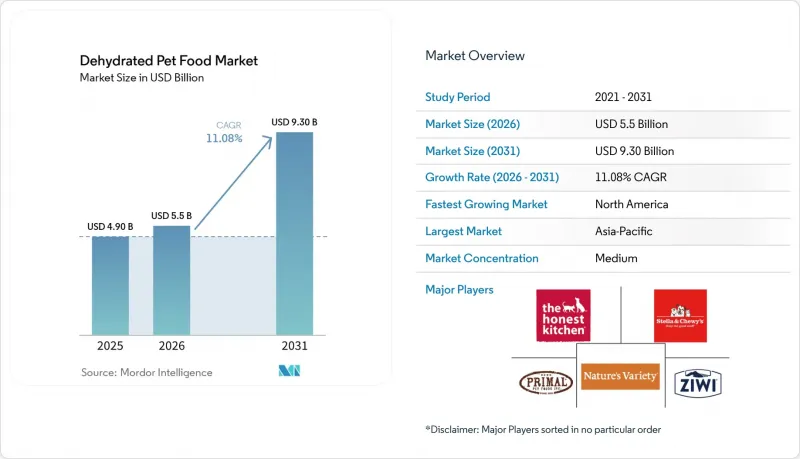

Dehydrated Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the dehydrated pet food market size is projected to grow from USD 4.90 billion in 2025 to USD 5.50 billion in 2026 and is projected to reach USD 9.30 billion by 2031, registering a CAGR of 11.08% during 2026-2031.

This report is Segmented by Product Type (Freeze-Dried Dehydrated Food, Air-Dried Dehydrated Food, and More), by Pet Type (Dog, Cat, and More), by Ingredient Source (Animal-Based, Plant-Based, and More), by Distribution Channel (Supermarkets and Hypermarkets, and More), and by Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Dehydrated Pet Food Market Trends and Insights

Premiumization of Pet Diets

Pet owners are increasingly treating their pets as family members, driving demand for premium, human-grade, minimally processed pet nutrition. According to the American Pet Products Association (APPA), premium pet food purchases rebounded in 2024, with 41% of dog owners and 38% of cat owners opting for higher-quality diets. This reflects a significant shift toward wellness-focused feeding . Dehydrated pet food aligns with this trend by providing clean-label, nutrient-dense formulations that emphasize health and ingredient transparency. Positioned between kibble and raw diets, these products appeal to consumers seeking convenient yet premium nutrition options, solidifying their role as a key beneficiary of the ongoing premiumization trend.

Humanization of Pets in Mature Economies

The growing trend of humanizing companion animals continues to drive the demand for premium, health-oriented pet nutrition. According to the American Pet Products Association (APPA) 2024-2025 National Pet Owners Survey, 94 million United States households owned a pet in 2024, highlighting the strong emotional bond and integration of pets into family life . This trend is prompting pet owners to prioritize high-quality, minimally processed, and human-grade diets. Dehydrated pet food meets these preferences by offering clean-label, nutrient-rich formulations, enabling brands to position their products as convenient, wholesome, and premium options that align with evolving consumer expectations and drive market growth.

High Price Differential Versus Conventional Kibble

Dehydrated pet food faces adoption challenges primarily because of its higher price compared to traditional kibble. The reliance on energy-intensive processes such as freeze-drying, extended production cycles, and the use of premium-quality protein ingredients substantially increases production costs. This leads to higher retail prices, making these products less affordable for cost-conscious consumers, especially in emerging, price-sensitive markets. During times of economic uncertainty or inflation, pet owners often opt for more economical feeding alternatives, which reduces demand for premium formats. As a result, the cost barrier remains a significant obstacle to wider market penetration, hindering overall growth.

Other drivers and restraints analyzed in the detailed report include:

- Growth of E-Commerce Pet-Food Retail

- Insect-Protein Dehydration Breakthroughs

- Limited Shelf Life After Opening

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Freeze-dried dehydrated food accounted for the largest 48% of market share in 2025, reflecting strong consumer trust, extended shelf stability, and premium positioning supported by nutrient retention and established retail presence. These products benefit from early market entry and wide availability across specialty channels, reinforcing their dominance among pet owners seeking minimally processed nutrition. Their convenience and perceived health benefits continue to drive adoption, particularly in developed markets where premium pet food consumption is well established and supported by higher disposable income and awareness of ingredient quality.

Air-dried dehydrated food is projected to grow at the fastest 18.8% CAGR from 2026 to 2031, supported by cost efficiency improvements and comparable nutritional value to freeze-dried alternatives. These products offer a balance between affordability and quality, making them attractive to consumers seeking premium options at relatively lower prices. Advances in drying technologies are improving production efficiency and product consistency, while maintaining high protein content and shelf stability. Increasing availability across online and specialty retail channels is further supporting adoption, particularly among new consumers transitioning from conventional pet food formats.

Dogs segment accounted for the largest 63% of the market share in 2025, driven by higher consumption levels and the growing trend of premiumization among dog owners. Larger portion sizes and established feeding habits have contributed to increased product demand, while owners are placing greater emphasis on high-protein, minimally processed diets. The availability of a wide range of products tailored to breed size, age, and health conditions further strengthens this segment's dominance. Additionally, higher spending on dog nutrition compared to other companion animals continues to reinforce its market leadership.

Cats segment is projected to grow at the fastest 13.4% CAGR from 2026 to 2031, driven by increasing urban pet ownership and greater awareness of feline-specific dietary requirements. Cats require high-protein, low-carbohydrate diets, which has boosted demand for nutrient-dense formulations. The rise in apartment living and smaller household sizes has contributed to increased cat adoption, particularly in the Asia-Pacific and Europe. Manufacturers are expanding feline-focused product lines with functional ingredients and tailored formulations, supporting sustained growth and diversification within this segment.

Geography Analysis

North America accounted for the largest 42% of the dehydrated pet food market share, driven by high pet ownership, robust consumer spending, and the widespread adoption of premium nutrition products. The region benefits from established retail networks and advanced supply chains that ensure consistent product availability. Additionally, growing consumer awareness of ingredient quality and minimally processed diets supports demand. The presence of major manufacturers and a strong distribution infrastructure further solidifies North America's leading position in the global market.

The Asia-Pacific region is projected to grow at the fastest 15% CAGR from 2026 to 2031, driven by rising pet ownership, urbanization, and higher disposable incomes. The expanding middle-class population and evolving lifestyles are driving higher spending on pet care and nutrition. Growth in e-commerce platforms is enhancing accessibility and product awareness, particularly in emerging markets. Furthermore, regulatory initiatives to improve food safety and quality standards are contributing to market growth. These factors collectively establish Asia-Pacific as a significant growth driver in the global market.

South America is experiencing changing adoption patterns influenced by growing pet ownership and increasing demand for commercial pet food, although affordability continues to be a challenge in several markets. According to the United States Department of Agriculture (USDA) Foreign Agricultural Service, South America imported USD 162.0 million worth of dog and cat food in 2024, an 11% increase compared to the previous year . This growth highlights the strengthening demand for packaged and premium pet nutrition products. It reflects improving economic conditions and a shift in consumer preferences toward higher-quality pet food, driving the gradual adoption of minimally processed and premium formats across the region.

- The Honest Kitchen, Inc.

- Stella & Chewy's, LLC

- Primal Pet Foods, Inc. (Pure Treats Inc.)

- Nature's Variety, Inc.

- Ziwi Limited

- K9 Natural Limited (Natural Pet Food Group)

- Grandma Lucy's, LLC

- Open Farm Inc.

- Carnivore Meat Company, LLC

- Steve's Real Food, LLC

- Sundays for Dogs, Inc.

- Kiwi Kitchens Limited

- Real Dog Box, Inc.

- The New Zealand Natural Pet Food Co. Limited

- Sojos (BrightPet Nutrition Group, LLC)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Premiumization of pet diets

- 4.2.2 Humanization of pets in mature economies

- 4.2.3 Growth of e-commerce pet-food retail

- 4.2.4 Veterinary endorsement of minimally processed nutrition

- 4.2.5 Insect-protein dehydration breakthroughs

- 4.2.6 Government disaster-relief stockpiling of light-weight pet rations

- 4.3 Market Restraints

- 4.3.1 High price differential versus conventional kibble

- 4.3.2 Limited shelf life after opening

- 4.3.3 Supply volatility of single-species novel proteins

- 4.3.4 Regulatory ambiguity on dehydrated raw pathogen standards

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Freeze-Dried Dehydrated Food

- 5.1.2 Air-Dried Dehydrated Food

- 5.1.3 Other Dehydrated Formats

- 5.2 By Pet Type

- 5.2.1 Dog

- 5.2.2 Cat

- 5.2.3 Other Companion Animals

- 5.3 By Ingredient Source

- 5.3.1 Animal-Based

- 5.3.2 Plant-Based

- 5.3.3 Insect-Based

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets and Hypermarkets

- 5.4.2 Pet Specialty Stores

- 5.4.3 Veterinary Clinics

- 5.4.4 Online Retailers

- 5.4.5 Other Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 New Zealand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 Nigeria

- 5.5.6.2 South Africa

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 The Honest Kitchen, Inc.

- 6.4.2 Stella & Chewy's, LLC

- 6.4.3 Primal Pet Foods, Inc. (Pure Treats Inc.)

- 6.4.4 Nature's Variety, Inc.

- 6.4.5 Ziwi Limited

- 6.4.6 K9 Natural Limited (Natural Pet Food Group)

- 6.4.7 Grandma Lucy's, LLC

- 6.4.8 Open Farm Inc.

- 6.4.9 Carnivore Meat Company, LLC

- 6.4.10 Steve's Real Food, LLC

- 6.4.11 Sundays for Dogs, Inc.

- 6.4.12 Kiwi Kitchens Limited

- 6.4.13 Real Dog Box, Inc.

- 6.4.14 The New Zealand Natural Pet Food Co. Limited

- 6.4.15 Sojos (BrightPet Nutrition Group, LLC)

7 Market Opportunities and Future Outlook