PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063845

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063845

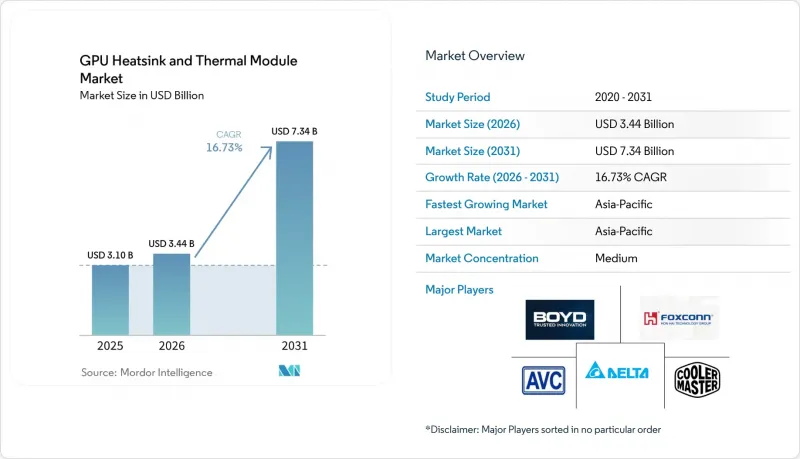

GPU Heatsink And Thermal Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the gPU heatsink and thermal module market size is expected to increase from USD 3.1 billion in 2025 to USD 3.44 billion in 2026 and reach USD 7.34 billion by 2031, growing at a CAGR of 16.37% over 2026-2031.

This report is Segmented by Product Type (Heat Sinks, Vapor Chambers, Heat Pipe-Based Modules, and Active Thermal Modules), Material (Aluminum-Based, Copper-Based, and Hybrid), GPU Type (Data Center/AI GPUs, Workstation GPUs, and Consumer/Gaming GPUs), and Geography (North America, Europe, Asia Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global GPU Heatsink And Thermal Module Market Trends and Insights

Surging AI Workloads Driving Data-Center GPU Shipments

Hyperscale operators spent more than USD 300 billion on AI infrastructure in 2026, a figure that includes liquid-cooling distribution units needed to prevent throttling in racks exceeding 100 kilowatts. NVIDIA's H200 dissipates 700 watts, and AMD's MI300X reaches 750 watts, pushing air-cooled designs beyond their economic limits. Intel's Gaudi 3 delivers 1200 watts only under liquid cooling, a 33% power-density premium that translates into faster model-training cycles. Delta Electronics reports liquid-cooling penetration climbing from 14% in 2024 to 40% in 2026, illustrating a decisive industry pivot. The bifurcated market now sees traditional finned heat sinks limited to edge-inference boxes below 300 watts, whereas vapor chambers and cold plates dominate the 500-watt-plus tier.

Escalating Thermal Design Power of Advanced Nodes

GPU power envelopes rise with each process generation. NVIDIA's RTX 5090 approaches 600 watts under sustained ray tracing, and memory junctions climb to 92 °C despite triple-slot coolers. RTX 4090's 450-watt spec already forced board partners to adopt vapor chambers that spread heat across larger fin surfaces. Data-center accelerators follow the same arc, with 700 watts becoming the entry point. Thermal-interface materials now exceed 15 W m-K but demand metal backplates to maintain contact pressure. IEC 62368-1 touch-temperature limits further constrain fin density, forcing creative airflow management.

OEM Shift Toward Integrated Liquid Cooling Loops

Server builders now ship closed-loop liquid systems pre-installed, bypassing the aftermarket for discrete modules. Lenovo's Neptune achieves a 1.1 power-usage effectiveness and recycles waste heat for facility heating, cutting cooling energy by 40%. Dell's PowerCool eRDHx enables 80-kilowatt racks that air systems cannot meet without prohibitive noise. Asetek's USD 35 million, two-year supply contract underscores the pivot toward OEM-centric revenue streams. While liquid loops enlarge the total market, they erode unit sales of standalone heat sinks, especially in data-center GPUs where liquid is the default.

Other drivers and restraints analyzed in the detailed report include:

- Emergence of Chiplet-Based GPU Architectures

- Growth of Ray-Tracing Gaming Titles

- Volatility in Copper Commodity Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vapor chambers accounted for the fastest expansion, posting a 17.17% CAGR outlook as GPU envelopes breach 600 watts. Heat sinks still secured 37.48% of 2025 revenue, covering sub-300-watt consumer GPUs, yet their share will contract as board partners migrate high-end designs to vapor chambers. Heat-pipe modules serve RTX 4080-class cards around 320 watts, but they face capillary-limit ceilings. Solder-attached vapor chambers lower GPU junction temperatures by 10-15%, making them indispensable in professional rendering stations. Active thermal modules integrate pumps and radiators, unlocking rack densities above 100 kilowatts. TaiSol's 3D vapor chamber layers evaporators to match chiplet footprints, while Cooler Master's FreeForm 2.0 allows dual-GPU loops on one radiator.

The GPU heatsink and thermal module market share of vapor chambers is rising because they deliver sub-0.1 °C-W thermal resistance in a thin profile, critical for multi-slot cards. Meanwhile, the GPU heatsink and thermal module market share of traditional heatsinks will shrink as air-cooling meets diminishing returns beyond 400 watts. Active modules remain niche in volume but command high average selling prices in AI servers. Together, these product-type dynamics keep innovation centered on vapor-chamber geometry and cold-plate microchannels rather than on fin-stack height.

Geography Analysis

Asia-Pacific generated 67.81% of 2025 revenue and is forecast to grow at a compound annual growth rate (CAGR) of 17.29% through 2031, driven by Taiwan's expertise in vapor-chamber manufacturing and China's large-scale assembly capabilities. Delta Electronics has committed NTD 12.1 billion (USD 380 million) to expand its Taoyuan production capacity, further solidifying the region's dominance in the market. Japan's Furukawa Electric plays a key role by supplying sintered pipes specifically designed for 1U chassis, while Vietnam and Thailand are emerging as alternative hubs for assembly, offering cost advantages and reducing reliance on traditional manufacturing centers.

North America ranks as the second-largest market, supported by hyperscale data center campuses located in states such as Virginia, Oregon, and Iowa. These facilities are increasingly adopting liquid-cooled racks with power capacities exceeding 100 kilowatts. Favorable tax incentives and access to renewable energy sources continue to drive the construction of new data centers in the region. In Europe, demand is concentrated in Germany's automotive simulation clusters and the United Kingdom's fintech data centers. Both regions operate under stringent carbon-pricing regulations, which are pushing buyers to adopt energy-efficient solutions such as advanced cold plates to meet sustainability goals.

South America, the Middle East, and Africa are still in the early stages of market development. In South America, Brazil's data center facilities are transitioning to 30-kilowatt racks that require advanced vapor-chamber designs to effectively manage heat dissipation. Meanwhile, Gulf nations in the Middle East are deploying liquid-cooled workstations to support AI-driven oil exploration activities, reflecting the region's growing interest in high-performance computing. Geographic diversification remains a key trend, as suppliers are increasingly establishing production lines in countries such as Vietnam, Thailand, and Mexico to mitigate risks associated with Taiwan-centric manufacturing and to meet the growing global demand for thermal management solutions.

- Boyd Corporation

- Cooler Master Technology Inc.

- Noctua GmbH

- Arctic GmbH

- Hon Hai Precision Industry Co., Ltd.

- Delta Electronics, Inc.

- Sunonwealth Electric Machine Industry Co., Ltd.

- Furukawa Electric Co., Ltd.

- Asia Vital Components Co., Ltd.

- Taisol Electronics Co., Ltd.

- Asetek A/S

- EKWB d.o.o.

- Thermalright Inc.

- Listan GmbH

- Corsair Gaming, Inc.

- ASUSTeK Computer Inc.

- Gigabyte Technology Co., Ltd.

- Micro-Star International Co., Ltd.

- Zotac Technology Limited

- Palit Microsystems Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging AI Workloads Driving Data-Center GPU Shipments

- 4.2.2 Escalating Thermal Design Power of Advanced Nodes

- 4.2.3 Growth of Ray-Tracing Gaming Titles

- 4.2.4 Expansion of Cloud Gaming Infrastructure Globally

- 4.2.5 Emergence of Chiplet-Based GPU Architectures

- 4.2.6 Increasing Use of Solder-Attached Vapor Chambers in Workstations

- 4.3 Market Restraints

- 4.3.1 Volatility in Copper Commodity Prices

- 4.3.2 OEM Shift Toward Integrated Liquid Cooling Loops

- 4.3.3 Supply Chain Concentration in East Asia

- 4.3.4 Environmental Regulations on Mining of Thermal Interface Metals

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Heat Sinks

- 5.1.2 Vapor Chambers

- 5.1.3 Heat Pipe-Based Modules

- 5.1.4 Active Thermal Modules

- 5.2 By Material

- 5.2.1 Aluminum-Based

- 5.2.2 Copper-Based

- 5.2.3 Hybrid (Aluminum + Copper)

- 5.3 By GPU Type

- 5.3.1 Data Center / AI GPUs

- 5.3.2 Workstation GPUs

- 5.3.3 Consumer / Gaming GPUs

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Southeast Asia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Boyd Corporation

- 6.4.2 Cooler Master Technology Inc.

- 6.4.3 Noctua GmbH

- 6.4.4 Arctic GmbH

- 6.4.5 Hon Hai Precision Industry Co., Ltd.

- 6.4.6 Delta Electronics, Inc.

- 6.4.7 Sunonwealth Electric Machine Industry Co., Ltd.

- 6.4.8 Furukawa Electric Co., Ltd.

- 6.4.9 Asia Vital Components Co., Ltd.

- 6.4.10 Taisol Electronics Co., Ltd.

- 6.4.11 Asetek A/S

- 6.4.12 EKWB d.o.o.

- 6.4.13 Thermalright Inc.

- 6.4.14 Listan GmbH

- 6.4.15 Corsair Gaming, Inc.

- 6.4.16 ASUSTeK Computer Inc.

- 6.4.17 Gigabyte Technology Co., Ltd.

- 6.4.18 Micro-Star International Co., Ltd.

- 6.4.19 Zotac Technology Limited

- 6.4.20 Palit Microsystems Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment