PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063868

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063868

AI-Based Care Coordination - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

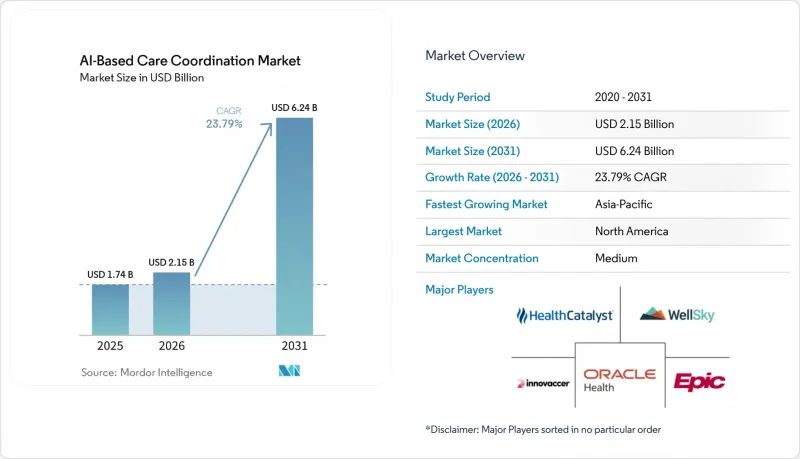

According to Mordor Intelligence, the aI-Based care coordination market size is projected to expand from USD 1.74 billion in 2025 and USD 2.15 billion in 2026 to USD 6.24 billion by 2031, registering a CAGR of 23.79% between 2026 to 2031.

This report is Segmented by Solution Type (EHR-Embedded, Care Management Suites, and More), Care Setting (Hospitals, Ambulatory, and More), Deployment Model (Cloud/SaaS, On-Premises, Hybrid), Application (Chronic Disease Care Pathways, and More) AI Technique (Predictive Analytics & Risk Stratification, and More), Integration Approach (EHR-Integrated, and More), and Geography. Value Forecasts in USD.

Global AI-Based Care Coordination Market Trends and Insights

Shift To Value-Based Care And ACO Models Elevates Analytics-Driven Workflows

The move from fee-for-service reimbursement toward value-based contracting continues to create a direct operating need for the AI-based care coordination market, because success under shared-risk models depends on earlier outreach, tighter follow-up, and fewer avoidable gaps in care. The State and Science of Value-based Care 2025 study found that 50% of surveyed organizations were actively investing in data analytics and AI, while 65% expressed optimism about AI's predictive value in value-based arrangements.

Evidence cited in the user draft also showed that Medicare Shared Savings Program ACOs using AI-enhanced analytics reported 40% higher shared savings distributions, which supports the case that better coordination performance can fund additional technology spending. That pattern matters because the AI-based care coordination market is no longer being bought only as software, it is being evaluated as an operating lever that can improve medical cost control and quality performance under risk contracts. As more ACOs and related provider groups seek repeatable gains in utilization management, discharge planning, and chronic disease follow-up, the commercial pull for automation becomes stronger. The result is a self-reinforcing cycle in which organizations with better coordination tools can post better contract performance, defend their economics, and widen the gap with providers still dependent on manual care management models.

CMS-0057-F Interoperability Mandate Catalyzes API-First Coordination Architectures

The CMS Interoperability and Prior Authorization final rule has accelerated the move toward API-first workflow design in the AI-based care coordination market, because it turns interoperability from a planning goal into a dated compliance requirement. CMS finalized the rule on January 17, 2024, with a January 1, 2026 deadline for certain prior authorization response timelines and a January 1, 2027 deadline for the related FHIR API requirements covering provider access, payer-to-payer exchange, and prior authorization. ONC also tied related interoperability work to lower administrative burden, noting projected savings of USD 19.2 billion over the coming decade from electronic prior authorization standards.

Once provider systems can retrieve more complete payer-side history through standardized interfaces, AI coordination tools can compress work that previously required separate payer portals, manual history checks, and repeated staff follow-up. That change makes the AI-based care coordination market more attractive to health systems and payers that need administrative simplification at scale, especially in referral, authorization, and pre-visit preparation workflows. It also favors vendors that were built for structured data exchange and flexible orchestration rather than those relying on closed interfaces and local custom integrations.

Data Privacy, Security, And Integration Complexity Slow AI Deployment

The AI-based care coordination market still faces a basic deployment challenge, because the same broad data access that improves coordination also widens the operational burden around privacy, consent, identity resolution, and interface reliability. These platforms need to ingest and normalize information from EHRs, payer systems, HIEs, remote monitoring streams, and community resource networks, and each source often carries a different data model and governance expectation. The State and Science of Value-based Care 2025 study found that 69% of surveyed respondents cited regulatory complexities as a primary reason for slower adoption, which shows that the issue extends well beyond technical interface work alone.

Federal TEFCA rulemaking and related interoperability activity continue to expand exchange pathways, but they also make trust, routing, and data-handling practices more visible to buyers that are assessing enterprise AI coordination deployments. Large health systems can usually absorb more of this integration effort through internal digital teams, but smaller providers often struggle to support the same level of data engineering, consent management, and workflow redesign. That imbalance slows broader adoption of the AI-based care coordination market, especially in mid-sized networks, community settings, and rural organizations that need the benefit but have fewer deployment resources.

Other drivers and restraints analyzed in the detailed report include:

- TEFCA QHIN-To-QHIN FHIR Exchange Accelerates Cross-Network Coordination

- AI-Driven Patient Flow And Discharge Orchestration Unlocks System Capacity

- High Implementation And Change-Management Costs Challenge ROI Realization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

EHR-embedded care coordination platforms led the solution landscape in 2025 with a 35.16% share, which reflected the advantage of staying inside the core workflow already used by clinicians and care managers. In the AI-based care coordination market, that installed-base position matters because switching between systems still slows documentation, follow-up, and exception handling. Care management suites for population health continued to hold an important secondary position, especially where organizations wanted a broader longitudinal view across attributed populations. Referral and network management tools also remained relevant, because post-acute and external handoffs still sit among the least digitized parts of the care journey. Standalone and other solution types continued to attract investment where providers wanted focused functionality without a full suite replacement.

The fastest-growing solution segment is SDoH closed-loop coordination platforms, which are projected to grow at 24.88% CAGR through 2031 as social needs closure becomes more visible in quality and population health workflows. This part of the AI-based care coordination industry is gaining traction because buyers now want evidence that referrals to community-based organizations were completed, tracked, and tied back to patient follow-up. Innovaccer announced in November 2025 a statewide partnership with the PopHealth Learning Center to support care coordination for 2 million Medi-Cal patients across 200 clinics, which illustrates how publicly sponsored programs are pushing broader SDoH-linked deployment. That policy and program pressure is changing the mix of demand inside the AI-based care coordination market, because buyers are no longer treating social screening as sufficient on its own. They are instead looking for auditable closed-loop processes that connect clinical teams, social services, and reporting requirements in one operating chain.

Hospitals and health systems held 46.17% share in 2025, which gave them the leading position across care settings because they control large technology budgets and manage the most complex patients. That scale gives hospital buyers an early advantage in the AI-based care coordination market, since they can spread deployment costs across care management, utilization review, discharge planning, and population health programs. Ambulatory and physician group settings still matter, but their buying patterns are more fragmented and often depend on narrower use cases or shared infrastructure. Post-acute and long-term care settings remained smaller in current share terms, yet they carry some of the highest coordination pain points in day-to-day operations. Other care settings also remained part of the demand mix where local network coordination gaps were large.

Home health and hospital-at-home is projected to record the fastest CAGR at 24.12% through 2031, which shows how quickly coordination demand is moving beyond the traditional inpatient campus. The hospital-at-home waiver extension through 2030 and the spread of approved programs across 139 health systems support that shift by making distributed acute care a more durable operating model rather than a temporary experiment. WellSky stated in February 2026 that its SkySense AI expansion into long-term care and skilled nursing could reduce documentation time by up to 50% in home health workflows, which signals stronger automation demand in post-acute settings. In practical terms, the AI-based care coordination market is moving toward the places where follow-up failures are common and staffing pressure is persistent. That makes home-based and post-acute care a natural growth area, even while hospitals continue to hold the largest current spending base.

Geography Analysis

North America held 43.18% share in 2025, which kept it as the largest regional block in the AI-based care coordination market. That lead is tied to a stronger regulatory and operating framework, because CMS interoperability deadlines, TEFCA network development, and value-based care adoption are moving in the same direction. The United States also has the densest concentration of scaled vendors, which helps convert product development into live contracts across payer and provider organizations. Within North America, the AI-based care coordination market benefits from a buyer base that is already familiar with risk-based care, utilization controls, and interoperability spending. Canada and Mexico remain at earlier stages, with some digital health foundation in place but less direct policy pressure than in the United States.

Europe presents a different operating profile for the AI-based care coordination market because compliance design plays a larger role in how systems are brought to market and scaled. Official European guidance on the interaction between the AI Act and MDR or IVDR shows why many care coordination tools tied to clinical decision or regulated workflows face heavier oversight requirements. France published a national strategy for AI and health data in July 2025, and CNSA also released its 2025-2026 roadmap for AI in autonomy and care coordination, which points to active public-sector support in targeted areas. Germany's applied activity is also visible through Fraunhofer ITWM's ViKI pro work in AI-based care planning for long-term care settings, which shows that the regional opportunity extends beyond hospitals and into broader care delivery models. The region therefore offers real demand, but that demand is filtered through stronger governance, more formal conformity expectations, and closer attention to how tools are classified and supervised.

Asia-Pacific is the fastest-growing region and is projected to expand at 27.36% CAGR through 2031, which gives it the strongest forward growth profile in the AI-based care coordination market. Growth in this region is being supported by aging populations, more active public digital health programs, and a willingness in several countries to use AI as part of system modernization. India published its Strategy for Artificial Intelligence in Healthcare in February 2026 and identified care coordination among the priority use cases, which supports longer-term deployment potential where digital public infrastructure is expanding. Japan is also moving forward, and Fujitsu Japan announced in March 2026 a joint proof of concept with Teikyo University Hospital focused on referred-patient management and data analysis, which shows concrete interest in AI-assisted coordination workflows. Outside the 3 leading regions, the Middle East and Africa and South America remain earlier-stage demand pockets, with activity concentrated in selective smart hospital and digital health programs rather than broad-based adoption.

- Arcadia

- athenahealth

- Bamboo Health

- eClinicalWorks

- Epic Systems

- Health Catalyst (Lumeon & Twistle)

- HealthEdge (GuidingCare)

- Innovaccer

- Lightbeam Health Solutions

- Medecision

- Netsmart

- Oracle Health (Cerner)

- PointClickCare

- Qventus

- Salesforce (Health Cloud)

- Signify Health (CVS)

- Unite Us

- Veradigm

- WellSky (CarePort)

- ZeOmega

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift To Value-Based Care and ACO Models Elevates Coordinated, Analytics-Driven Workflows

- 4.2.2 Interoperability Mandates (CMS 0057-F) Catalyze API-First, Automated Coordination

- 4.2.3 Cloud-First Architectures Scale AI Pipelines Across Settings and Stakeholders

- 4.2.4 TEFCA QHIN-To-QHIN FHIR Exchange Enables Cross-Network, Near Real-Time Data Flows

- 4.2.5 AI-Driven Patient Flow/Discharge Orchestration to Unlock Capacity And Reduce LOS

- 4.3 Market Restraints

- 4.3.1 Data Privacy/Security and Integration Complexity Slow AI Deployment

- 4.3.2 High Implementation and Change-Management Costs Challenge ROI

- 4.3.3 EU AI Act High-Risk Obligations Raise Compliance Burden in Europe

- 4.3.4 Uneven Real-Time Cross-Network Eventing Until TEFCA FHIR Matures

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Solution Type

- 5.1.1 EHR-embedded care coordination platforms

- 5.1.2 Care management suites (population health / care management)

- 5.1.3 Patient flow & discharge orchestration

- 5.1.4 Referral & network management (including post-acute transitions)

- 5.1.5 SDoH closed-loop coordination platforms

- 5.1.6 Others

- 5.2 By Care Setting

- 5.2.1 Hospitals & health systems

- 5.2.2 Ambulatory/physician groups & clinics

- 5.2.3 Post-acute & long-term care (SNF, rehab, home health)

- 5.2.4 Home health & hospital-at-home

- 5.2.5 Others

- 5.3 By Deployment Model

- 5.3.1 Cloud / SaaS

- 5.3.2 On-premises

- 5.3.3 Hybrid

- 5.4 By Application

- 5.4.1 Chronic disease care pathways

- 5.4.2 Transitions of care / discharge & post-acute coordination

- 5.4.3 High-risk identification & outreach

- 5.4.4 Prior authorization & utilization management coordination

- 5.4.5 SDoH referrals & closed-loop coordination

- 5.4.6 Others

- 5.5 By AI Technique

- 5.5.1 Predictive analytics & risk stratification

- 5.5.2 NLP & information extraction/summarization

- 5.5.3 Workflow automation, RPA & agentic AI

- 5.5.4 Recommender systems / next best action

- 5.5.5 Computer vision & remote monitoring

- 5.6 By Integration Approach

- 5.6.1 EHR-integrated

- 5.6.2 HIE/QHIN-integrated

- 5.6.3 Standalone with open APIs

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Arcadia

- 6.3.2 athenahealth

- 6.3.3 Bamboo Health

- 6.3.4 eClinicalWorks

- 6.3.5 Epic Systems

- 6.3.6 Health Catalyst (Lumeon & Twistle)

- 6.3.7 HealthEdge (GuidingCare)

- 6.3.8 Innovaccer

- 6.3.9 Lightbeam Health Solutions

- 6.3.10 Medecision

- 6.3.11 Netsmart

- 6.3.12 Oracle Health (Cerner)

- 6.3.13 PointClickCare

- 6.3.14 Qventus

- 6.3.15 Salesforce (Health Cloud)

- 6.3.16 Signify Health (CVS)

- 6.3.17 Unite Us

- 6.3.18 Veradigm

- 6.3.19 WellSky (CarePort)

- 6.3.20 ZeOmega

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment