PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063872

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063872

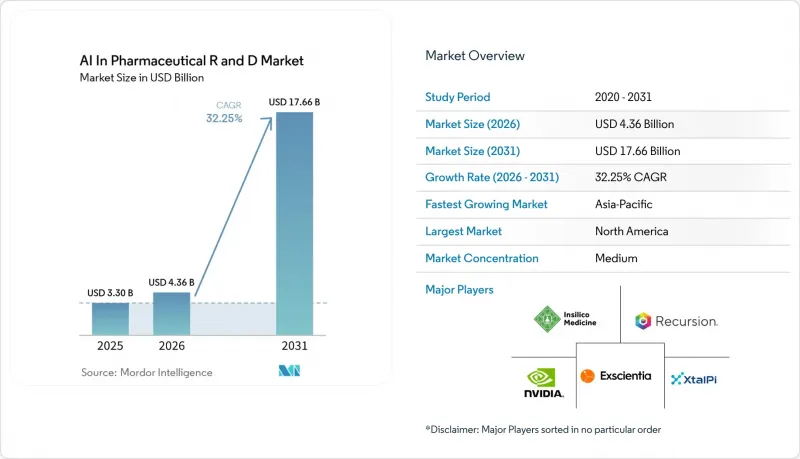

AI In Pharmaceutical R & D - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the aI in pharmaceutical r & d market size was valued at USD 3.30 billion in 2025 and is estimated to grow from USD 4.36 billion in 2026 to reach USD 17.66 billion by 2031, at a CAGR of 32.25% during the forecast period (2026-2031).

This report is Segmented by Component (Software, Services, Hardware), Technology (Machine Learning, NLP, Deep / Generative Learning), Application (Target ID, Hit-To-Lead, Preclinical / Clinical, Drug Optimisation), End User (Pharma & Biotech, Cros, Academic Institutes, Others) and Geography (North America, Europe, APAC, MEA, South America). Forecasts in Value (USD).

Global AI In Pharmaceutical R & D Market Trends and Insights

Soaring Costs in Biopharma R&D

JAMA estimates that the average cost of bringing a drug to market is USD 1.31 billion, accounting for capital costs and program attrition. Smaller biopharma firms face a 37.6% cost premium compared to the top 20 companies, highlighting the critical need to reduce drug development timelines. AI platforms are addressing this challenge by improving phase-transition success rates and shortening patient trial durations. For instance, Insilico Medicine identified a preclinical candidate in just eight months, significantly faster than the traditional 2.5 to 4-year timeframe. These advancements are increasing confidence in AI's ability to reduce costs in pharmaceutical R&D, with deal structures now frequently incorporating milestones tied to accelerated timelines.

Surge in Biomedical Data Volumes

Foundation models depend on diverse data sets, including genomics, proteomics, imaging, and electronic health records (EHRs). Recursion, for example, has gained exclusive access to 20 petabytes of oncology data, increasing its total data holdings to approximately 50 petabytes. Similarly, IBM Research trains its models on over a billion small molecules and protein sequences, while Xaira's X-Cell leverages 4.9 billion parameters derived from 25.6 million single-cell transcriptomes. The expansion and diversity of these data sets enhance model generalization, enabling predictions for previously untested targets or pathways. This trend is driving continuous investments in cloud computing, further expanding opportunities for specialized infrastructure providers in the AI-driven pharmaceutical R&D market.

Data Quality & Standardization Gaps

Inconsistent annotations, missing metadata, and non-standard identifiers weaken the generalizability of models. Regulatory bodies now require traceable documentation for every data-processing step and explicit acknowledgment of limitations. Collaborative initiatives, such as federated projects, are addressing these gaps by standardizing ontologies across partners. Additionally, national strategies, like China's digital-intelligent transformation plan for 2025, aim to establish unified data standards and regional data hubs to improve data quality. However, challenges such as outdated assays and underrepresented populations remain significant obstacles that could limit the growth of the AI in pharmaceutical R&D market until adequately addressed.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Pharma-AI Collaborations & Funding

- Regulatory Embrace of AI in R&D

- Shortage of AI-Skilled Life-Science Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, software captured a dominant 57.34% share of the AI in pharmaceutical R&D market. Integrated platforms like RecursionOS manage processes ranging from target discovery to clinical-trial simulations, processing millions of phenomics images weekly and storing 36 petabytes of proprietary data. Exscientia's platform integrates primary human-tissue assays into design loops, which management asserts enhances clinical relevance compared to traditional animal models. This strong platform loyalty drives recurring license revenue and supports the growth trajectory of the AI in pharmaceutical R&D market.

While services currently hold a smaller market share, they are projected to grow at a robust 32.55% CAGR through 2031. Contract Research Organizations (CROs) are differentiating their offerings by incorporating AI-driven patient-recruitment modules and adaptive-trial designs. As sponsors increasingly prefer variable costs over fixed ones, the adoption of outsourced AI capabilities is expected to expand, deepening their penetration in the AI in pharmaceutical R&D market.

In 2025, machine learning accounted for 45.45% of technology revenue, driving key processes such as ADME-Tox prediction, biomarker discovery, and patient stratification. Supervised algorithms continue to be dependable, particularly when labeled data is abundant.

Generative learning is emerging as the fastest-growing segment, with a remarkable 32.79% CAGR projected through 2031. AlphaFold 3's innovative diffusion method has significantly enhanced protein-ligand predictions, improving accuracy by 50%. Exscientia's sixth AI-generated molecule entered clinical trials in 2023, marking a pivotal moment for the technology. With advancements like transformer and diffusion networks now crafting antibodies, RNA therapeutics, and PROTACs, generative frameworks are set to redefine the AI in pharmaceutical R&D market landscape.

Geography Analysis

In 2025, North America accounted for 48.45% of the revenue, driven by biotech clusters spanning Boston to San Diego and early FDA guidance on AI credibility. In 2024, venture investors directed nearly USD 10 billion into AI drug-discovery deals, with five transactions exceeding USD 1 billion. Demonstrating the region's computational capabilities, Recursion's BioHive-2 supercomputer features 504 NVIDIA H100 GPUs. These factors collectively establish North America as the benchmark market for AI-driven innovation in pharmaceutical R&D.

Europe, while following North America, demonstrates strong regulatory involvement. Federated learning initiatives, such as MELLODDY, emphasize compliance with GDPR requirements. The EMA's reflection paper provides detailed guidance across the product life cycle. Additionally, public-private partnerships and Horizon Europe funding foster early-stage ventures, maintaining Europe's relevance in the AI pharmaceutical R&D market.

Asia-Pacific is the fastest-growing region, with a projected CAGR of 34.00% through 2031. China's digital-intelligent transformation plan aims for full implementation by 2030, including 100 pilot digital drug factories and 10 large-model innovation hubs. India offers cost-efficient data-science talent for Contract Research Organizations (CROs), while Japan utilizes precision-medicine grants to modernize its clinical infrastructure. Although Latin America and the Middle East & Africa (MEA) lag in computational resources and regulatory frameworks, pilot projects in Brazil and the UAE indicate gradual progress, expanding the global footprint of AI in pharmaceutical R&D.

- Absci Corporation

- Alphabet Inc. (DeepMind / Isomorphic Labs)

- Atomwise

- BenevolentAI S.A.

- Berg Health (BPGbio)

- BioSymetrics

- Cloud Pharmaceuticals

- Deep Genomics Inc.

- Exscientia plc

- GNS Healthcare (Aitia)

- Healx

- Iktos

- Insilico Medicine IP Limited

- insitro

- IBM

- NVIDIA

- Owkin

- Recursion Pharmaceuticals

- Relay Therapeutics

- Schrodinger

- Standigm

- Valo Health

- Verge Genomics

- XtalPi

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Biopharma R&D Costs

- 4.2.2 Expanding Biomedical Data Volumes

- 4.2.3 Pharma-AI Partnerships & Funding Surge

- 4.2.4 Regulatory Openness to AI in R&D

- 4.2.5 Emergence of Foundation Bio-Models

- 4.2.6 Growth of Federated?Learning Data Corridors

- 4.3 Market Restraints

- 4.3.1 Data Quality & Standardization Gaps

- 4.3.2 Shortage of AI-Skilled Life-Science Talent

- 4.3.3 IP Ambiguity for AI-Generated Molecules

- 4.3.4 Rising GPU / Cloud Compute Costs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.3 Hardware

- 5.2 By Technology

- 5.2.1 Machine Learning

- 5.2.2 Natural Language Processing

- 5.2.3 Deep / Generative Learning

- 5.3 By Application

- 5.3.1 Target Identification & Validation

- 5.3.2 Hit Generation & Lead Optimisation

- 5.3.3 Preclinical / Clinical Testing

- 5.3.4 Drug Optimisation & Repurposing

- 5.4 By End User

- 5.4.1 Pharmaceutical & Biotechnology Companies

- 5.4.2 Contract Research Organisations

- 5.4.3 Academic & Research Institutes

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Absci Corporation

- 6.3.2 Alphabet Inc. (DeepMind / Isomorphic Labs)

- 6.3.3 Atomwise

- 6.3.4 BenevolentAI S.A.

- 6.3.5 Berg Health (BPGbio)

- 6.3.6 BioSymetrics

- 6.3.7 Cloud Pharmaceuticals, Inc.

- 6.3.8 Deep Genomics Inc.

- 6.3.9 Exscientia plc

- 6.3.10 GNS Healthcare (Aitia)

- 6.3.11 Healx

- 6.3.12 Iktos

- 6.3.13 Insilico Medicine IP Limited

- 6.3.14 insitro

- 6.3.15 International Business Machines Corporation

- 6.3.16 NVIDIA

- 6.3.17 Owkin

- 6.3.18 Recursion Pharmaceuticals

- 6.3.19 Relay Therapeutics

- 6.3.20 Schrodinger

- 6.3.21 Standigm

- 6.3.22 Valo Health

- 6.3.23 Verge Genomics

- 6.3.24 XtalPi

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment