PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063916

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063916

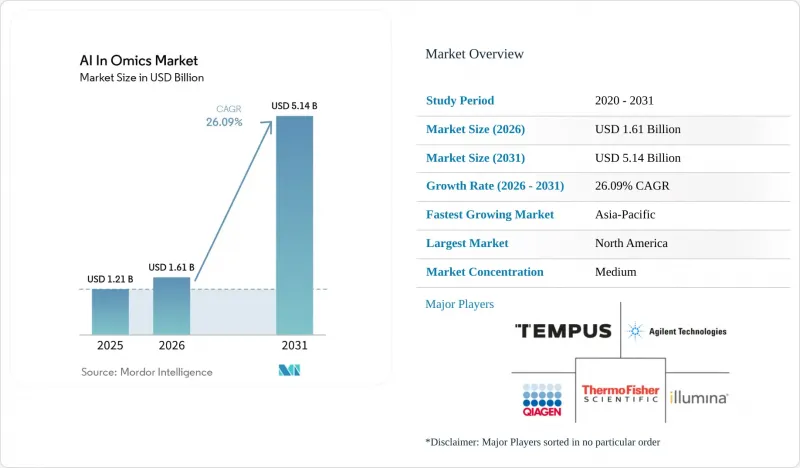

AI In Omics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the aI in omics market size was valued at USD 1.21 billion in 2025 and is estimated to grow from USD 1.61 billion in 2026 to reach USD 5.14 billion by 2031, at a CAGR of 26.09% during the forecast period (2026-2031).

This report is Segmented by Component (Software, Hardware, Services), Omics Type (Genomics, Transcriptomics, Proteomics, and More), AI Technology (ML, Deep Learning, NLP, CV, Data Mining), Application (Clinical Diagnostics, and More), End User (Pharmaceutical Companies, and More), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global AI In Omics Market Trends and Insights

Precision Medicine Adoption Reshaping Drug Development Economics

Precision oncology and rare disease workflows are moving molecular profiling closer to the center of therapeutic selection, which is changing how clinical teams decide where to place time, capital, and trial resources in the AI in omics market. That shift matters because multi-omics models can help narrow patient groups earlier, which supports better alignment between biological signal, trial design, and downstream treatment response. Tempus AI's Lens platform shows that this model is scaling commercially, with Data and Applications revenue reaching USD 316.4 million in 2025, up 30.9% year over year. Tempus also reported total 2025 revenue of USD 1.3 billion, which indicates that AI-linked clinical and data services are moving beyond isolated pilot work and into repeatable operating models. As these workflows move earlier in development, disease-specific pathway findings can be reused across related programs, which improves the commercial return on each curated dataset. That is helping the AI in omics market attract spending from drug discovery groups, translational researchers, and clinically focused software vendors at the same time.

Rising Omics Data Volumes Straining Legacy Analytical Infrastructure

Rising data volumes remain a basic growth engine for the AI in omics market because multi-layer biological datasets are becoming too large and too complex for many legacy analytical stacks. Modern projects rarely work with one modality in isolation, so sequence, expression, protein, phenotype, and clinical context often need to be processed together inside the same computational environment. That creates pressure not just on storage, but also on preprocessing, harmonization, inference speed, validation tracking, and retraining capacity as new records continue to arrive. NVIDIA states that Parabricks can deliver more than 100 times faster whole-genome analysis at 50% lower compute cost than CPU workflows, which shows why accelerated and cloud-ready pipelines are gaining favor. Once an institution commits to that stack, migration becomes harder because data models, validation routines, and user habits become tied to the platform architecture. This is why the AI in omics market is moving away from stand-alone tools and toward integrated environments that combine compute, analytics, and workflow management in a single layer.

Data Privacy and Consent Constraints Fragmenting Training Datasets

Data privacy and consent rules keep the AI in omics market from using all of the data it generates, even when the scientific value of those records is high. Whole-genome sequences cannot be de-identified as easily as many other clinical records, so institutions still face strict governance expectations around access, storage, linkage, and secondary use. The European Commission states that the EHDS Regulation entered into force in March 2026 and covers secondary use of genomic, proteomic, transcriptomic, metabolomic, and epigenomic data, but national Health Data Access Bodies will only become operational over time. That means near-term access remains uneven, with local consent rules, legal reviews, and security requirements still slowing multi-site dataset assembly. The hardest-to-access material often includes underrepresented ancestry groups, which can deepen bias when models are trained on narrower and less representative cohorts. Federated learning can help the AI in omics market reduce central data transfer, but it still depends on shared governance, compatible workflows, and reliable coordination across institutions.

Other drivers and restraints analyzed in the detailed report include:

- AI Compressing the Biomarker-to-Clinical-Trial Pipeline

- Companion Diagnostics Embedding AI Omics Into Regulatory Workflows

- Multiomics Data Standardization Constraining Cross-Platform Interoperability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 55.2% of 2025 revenue, which kept it as the largest component in the AI in omics market and reflected the strength of platform-led commercialization. That lead came from cloud-based environments that combine prebuilt pipelines, curated knowledge layers, compute access, and visualization tools into one operating system for omics analysis. For many users, this reduces the need to build internal infrastructure before beginning multi-omics work, which makes adoption easier for teams that have data but limited engineering capacity. It also shortens time to use because analysts can move from raw files to interpretation inside a single workflow instead of stitching together multiple tools. Hardware remained the smallest component because more analytical workloads are now being separated from local instrumentation and shifted into scalable remote environments.

Services are projected to grow at 34.9% CAGR through 2031, which makes them the fastest-expanding component of the AI in omics market size and shows where incremental value creation is moving. Demand is shifting toward custom model development, bioinformatics consulting, workflow management, and long-cycle data integration support as projects become harder to standardize across institutions and use cases. QIAGEN said its Digital Insights business delivered double-digit constant-exchange-rate growth in FY2025 and that the company plans at least 14 AI-enabled applications by 2028. That matters because the AI in omics industry is creating recurring service demand around software cores, especially where users need validation, retraining, regulatory documentation, and workflow tuning after initial deployment. As AI tools move deeper into regulated and clinically linked settings, external support becomes less optional and more embedded in the day-to-day operating model.

Genomics held 35.2% of revenue in 2025 and is forecast to expand at 40.1% CAGR through 2031, which means it leads both scale and growth in the AI in omics market. That position reflects its role as the base layer for most multi-omics workflows, since genomic sequence often serves as the starting frame for linking downstream expression, protein, and phenotype signals. Population-scale sequencing and the wider use of biobank-linked research continue to enlarge the training base available for model development, which reinforces genomics as the most commercially central omics layer. Transcriptomics and proteomics are gaining ground as complementary layers because they add functional context that sequence data alone cannot provide in clinical and drug development settings. Metabolomics and epigenomics remain smaller in revenue, but research interest keeps rising because both layers help explain phenotypic variability that sequence changes do not fully capture on their own.

The AI in omics market still centers on genomics because new multimodal models usually begin with sequence data and then attach other biological layers as the context widens. NVIDIA said Evo 2 is a 40-billion parameter genomic foundation model trained on 8.85 trillion nucleotides from more than 128,000 genomes. That scale supports the view that genomic sequence is becoming the primary substrate for larger biological foundation models that can later absorb transcriptomic, proteomic, and clinical context. Within the AI in omics industry, this keeps genomics at the center of product design, long-horizon model training, and data licensing priorities across the value chain. It also means suppliers that already control high-quality genomic workflows hold an important starting advantage as broader multi-omics platforms continue to evolve.

Geography Analysis

North America held 38.2% of the AI in omics market share in 2025, which made it the largest regional revenue pool and reflected the concentration of sequencing infrastructure, AI talent, and pharmaceutical research spending in one ecosystem. The United States drives that lead because clinical genomics networks, data-oriented software firms, academic medical centers, and large drug developers are already deeply connected. Tempus reported USD 1.3 billion in 2025 revenue, up 83.4% year over year, which illustrates the commercialization scale that the U.S. environment can support when clinical data, analytics, and payer familiarity line up. The U.S. Food and Drug Administration's 2025 companion diagnostic decisions also showed that AI-linked molecular tests can move through recognizable regulatory paths when evidence packages are strong. That combination of infrastructure depth, reimbursement familiarity, and regulatory experience keeps North America ahead in deployment speed across the AI in omics market.

Europe remains a major region in the AI in omics market, even as its policy structure both enables longer-term data use and raises near-term compliance costs for many participants. The European Commission states that the EHDS Regulation entered into force in March 2026 and covers secondary use of genomic, proteomic, transcriptomic, metabolomic, and epigenomic data. Germany's genomDE model project had integrated more than 5,000 patients by autumn 2024 and targets 100,000 whole-genome sequences over 5 years. These programs should expand the region's usable data base over time, but the operational burden of the EU AI Act and related governance steps still favors better-established vendors.

Asia-Pacific is projected to grow at 37.4% CAGR, which gives it the fastest regional expansion in the AI in omics market size through 2031 and points to rising momentum in government-backed genomics and digital health programs. That pace reflects efforts across major Asian economies to build local sequencing capacity, strengthen clinical data systems, and reduce dependence on Western ancestry-biased training sets. Japan also shows active translation of language models into genomics, with DBCLS reporting in 2026 that ChatTogoVar outperformed GPT-4o in genomic variant interpretation. South America and the Middle East and Africa remain smaller today, but better healthcare infrastructure and growing startup activity should gradually widen future adoption opportunities.

- 10x Genomics

- Agilent Technologies

- Amazon Web Services

- BGI

- Bruker

- Deep Genomics

- DNAnexus

- DNAstack

- Elucidata

- Roche

- Fabric Genomics

- Illumina

- Lifebit

- NVIDIA

- Oxford Nanopore Technologies

- PacBio

- QIAGEN

- SOPHiA GENETICS

- Tempus AI

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Precision Medicine Adoption in Oncology and Rare Disease Workflows

- 4.2.2 Rising Omics Data Volumes and Complexity

- 4.2.3 AI-Enabled Target and Biomarker Discovery Acceleration

- 4.2.4 Expansion of Clinical Multiomic Assays and Companion Diagnostics

- 4.2.5 Billion-Cell Atlas Programs Expanding Training Corpora

- 4.2.6 Federated Clinico-Omics Environments Enabling Model Development

- 4.3 Market Restraints

- 4.3.1 Data Privacy, Consent, and Cybersecurity Constraints

- 4.3.2 Multiomics Data Standardization and Interoperability Gaps

- 4.3.3 EU AI Act and EHDS Compliance Burden

- 4.3.4 Atlas-Scale Annotation and Label Quality Bottlenecks

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Hardware

- 5.1.3 Services

- 5.2 By Omics Type

- 5.2.1 Genomics

- 5.2.2 Transcriptomics

- 5.2.3 Proteomics

- 5.2.4 Metabolomics

- 5.2.5 Epigenomics

- 5.3 By AI Technology

- 5.3.1 Machine Learning

- 5.3.2 Deep Learning

- 5.3.3 Natural Language Processing

- 5.3.4 Computer Vision

- 5.3.5 Data Mining

- 5.4 By Application

- 5.4.1 Drug Discovery & Development

- 5.4.2 Clinical Diagnostics

- 5.4.3 Precision Medicine

- 5.4.4 Biomarker Discovery

- 5.4.5 Target Identification & Validation

- 5.5 By End User

- 5.5.1 Pharmaceutical & Biotechnology Companies

- 5.5.2 Academic & Research Institutes

- 5.5.3 Hospitals & Clinical Laboratories

- 5.5.4 Contract Research Organizations

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 10x Genomics

- 6.3.2 Agilent Technologies

- 6.3.3 Amazon Web Services

- 6.3.4 BGI Genomics

- 6.3.5 Bruker Corporation

- 6.3.6 Deep Genomics

- 6.3.7 DNAnexus

- 6.3.8 DNAstack

- 6.3.9 Elucidata

- 6.3.10 F. Hoffmann-La Roche AG

- 6.3.11 Fabric Genomics

- 6.3.12 Illumina, Inc.

- 6.3.13 Lifebit

- 6.3.14 NVIDIA

- 6.3.15 Oxford Nanopore Technologies

- 6.3.16 PacBio

- 6.3.17 QIAGEN

- 6.3.18 SOPHiA GENETICS

- 6.3.19 Tempus AI

- 6.3.20 Thermo Fisher Scientific

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment