PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063918

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063918

AI In CRO Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

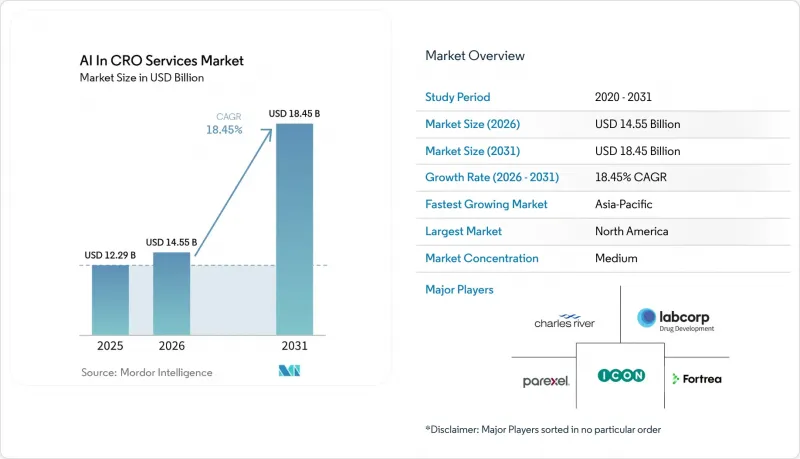

According to Mordor Intelligence, the aI in cRO services market size is projected to expand from USD 12.29 billion in 2025 and USD 14.55 billion in 2026 to USD 18.45 billion by 2031, registering a CAGR of 18.45% between 2026 to 2031.

This report is Segmented by Service Type (Clinical Trial Management, Biometrics & Analytics, and More), AI Technology (ML, NLP, Generative AI, and More), Therapeutic Area (Oncology, Rare Diseases, and More), Trial Phase (I, II, III, IV/RWE), End User (Pharma, Biotech, Medical Device, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global AI In CRO Services Market Trends and Insights

Rising Late-Stage Trial Complexity and Data Intensity

Traditional CRO operating models are increasingly inadequate in managing the growing data volumes from late-stage programs. This issue is particularly significant in Phase III studies within the AI in CRO services market, where adaptive endpoints, wearable signals, biomarker data, and real-world inputs are integrated into a single program. Centralized data flow approaches have demonstrated the ability to automate data ingestion, reduce programming cycle times, and enhance efficiency in data issue management. These advancements highlight why sponsors now consider AI capabilities a core criterion when awarding major programs. As a result, CTMS and data platforms in the AI in CRO services market have transitioned from supporting tools to essential commercial assets.

Biotech Outsourcing Demand for Flexible Clinical Capacity

Biotech companies, often operating with lean internal teams, increasingly rely on external partners for execution and planning support. In the AI in CRO services market, this reliance is shifting from basic outsourcing to engaging CROs capable of modeling trial scenarios, identifying potential bottlenecks, and accelerating feasibility decisions. This shift is redefining vendor competition, as staffing depth alone no longer meets sponsor needs when development plans change rapidly. Additionally, hybrid engagement models are gaining traction, allowing sponsors to access platforms and specialized support without committing to a single service structure. Consequently, AI readiness is becoming a critical factor in early-stage sponsor relationships.

AI Validation and GxP Compliance Uncertainty

Validation remains a significant barrier to the broader adoption of AI in regulated clinical workflows. The FDA's draft guidance in January 2025 introduced a seven-step credibility framework for AI models in regulatory submissions. However, final guidance has yet to be issued. This situation places sponsors and CROs in an interim phase where expectations are somewhat clearer but not fully defined. In the AI in CRO services market, this challenge primarily impacts areas such as dose selection, safety monitoring, and submission-related applications, while lower-risk tasks like document or workflow management are less affected. As a result, the market continues to grow rapidly, but adoption rates vary across different service categories.

Other drivers and restraints analyzed in the detailed report include:

- Decentralized and Hybrid Trial Expansion

- Precision Medicine and Biomarker-Driven Recruitment

- Fragmented Sponsor-CRO-Site Data Interoperability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Clinical Trial Management Services, holding 57.34% of the market share in 2025, dominated the AI in CRO services market. This leadership reflects its critical role in global multi-site coordination, risk-based monitoring, site performance tracking, and regulatory document management. Efficiency gains from AI-driven orchestration functions have solidified their position as key revenue drivers. Additionally, steady investments in biometrics, data management, analytics, and regulatory support services further highlight their importance in trial execution.

Early Development & Translational Services is expected to grow at a 19.20% CAGR from 2026 to 2031, making it the fastest-growing segment. Sponsors are increasingly using AI for feasibility simulations and early decision-making to reduce delays in trial initiation. AI platforms have demonstrated the ability to identify trial sites efficiently, accelerating Phase III programs across multiple countries. Adjacent services, such as AI-enabled writing and pathology workflows, are also evolving, showcasing the industry's focus on early-stage AI capabilities.

Machine Learning, with a 42.45% share in 2025, led the AI in CRO services market as the primary technology layer. Its widespread application in site selection, risk prediction, data cleaning, anomaly detection, and workflow optimization underscores its commercial durability. The technology remains integral to improving recurring operational tasks, while emerging approaches like knowledge graphs are gaining traction in oncology and rare disease workflows.

Natural Language Processing (NLP) is projected to grow at a 20.35% CAGR through 2031, making it the fastest-growing AI technology segment. This growth is driven by the need to process large volumes of unstructured data, such as EHR notes and clinical narratives. AI systems have demonstrated strong performance in trial matching and structured data extraction, signaling a shift toward deeper applications of language models in recruitment, documentation, and data normalization.

Geography Analysis

In 2025, North America accounted for 44.05% of the AI in CRO services market, maintaining its leadership position. This dominance stems from a strong biopharma sponsor base, a mature CRO ecosystem, and early regulatory advancements for AI in drug development. The region also benefits from being a hub for AI-specialist vendors and significant investments in full-service CRO platforms, strengthening its commercial foundation in the U.S. and Canada.

Europe is the second-largest regional market, driven by Germany, the U.K., and France. Its growth is supported by strong academic research networks, a large sponsor base, and investments in digital health and drug research. Europe also serves as a key base for multi-country studies, creating demand for vendors skilled in managing compliance and data workflows across jurisdictions.

Asia-Pacific is projected to grow at a 23.00% CAGR from 2026 to 2031, making it the fastest-growing region in the AI in CRO services market. The region's growth is fueled by large patient pools, cost-effective trials, and increasing digital health investments. China plays a significant role in this expansion, with AI integration deepening across the development process, positioning Asia-Pacific as a key area for market growth.

- Agilisium

- Ardigen

- Aurora Analytica

- Charles River

- Emmes Group

- Fortrea

- IQVIA

- ICON

- Inductive Quotient

- InnovoCommerce

- LabCorp

- LyfeSci

- MedPace

- Novotech

- Parexel International

- PhaseV

- PSI CRO

- Thermo Fisher Scientific Inc. (PPD)

- Verisian

- Voiant Clinical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Late-Stage Trial Complexity and Data Intensity

- 4.2.2 Biotech Outsourcing Demand for Flexible Clinical Capacity

- 4.2.3 Decentralized and Hybrid Trial Expansion

- 4.2.4 Precision Medicine and Biomarker-Driven Recruitment

- 4.2.5 Genai Compression of Study Start-Up and Medical Writing Cycles

- 4.2.6 RWE-Linked Synthetic Control and Feasibility Models

- 4.3 Market Restraints

- 4.3.1 AI Validation and GxP Compliance Uncertainty

- 4.3.2 Fragmented Sponsor-CRO-Site Data Interoperability

- 4.3.3 Liability Ambiguity for AI-Assisted Regulated Outputs

- 4.3.4 Training-Data Bias in Site and Patient Models

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD Billion)

- 5.1 By Service Type

- 5.1.1 Clinical Trial Management Services

- 5.1.2 Biometrics, Data Management & Analytics Services

- 5.1.3 Laboratory, Imaging & Sample Intelligence Services

- 5.1.4 Regulatory, Safety & Medical Writing Services

- 5.1.5 Early Development & Translational Services

- 5.2 By AI Technology

- 5.2.1 Machine Learning

- 5.2.2 Natural Language Processing

- 5.2.3 Generative AI / Large Language Models

- 5.2.4 Computer Vision

- 5.2.5 Knowledge Graphs & Causal AI

- 5.2.6 Predictive Analytics / Digital Twins

- 5.3 By Therapeutic Area

- 5.3.1 Oncology

- 5.3.2 Rare Diseases

- 5.3.3 Infectious Diseases & Vaccines

- 5.3.4 Neurology

- 5.3.5 Cardiovascular & Metabolic Disorders

- 5.3.6 Immunology & Inflammation

- 5.4 By Trial Phase

- 5.4.1 Phase I

- 5.4.2 Phase II

- 5.4.3 Phase III

- 5.4.4 Phase IV and Real-World Evidence

- 5.5 By End User

- 5.5.1 Pharmaceutical Companies

- 5.5.2 Biotechnology Companies

- 5.5.3 Medical Device Companies

- 5.5.4 Academic & Research Institutes

- 5.5.5 Government and Nonprofit Sponsors

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Agilisium

- 6.3.2 Ardigen

- 6.3.3 Aurora Analytica

- 6.3.4 Charles River Laboratories

- 6.3.5 Emmes Group

- 6.3.6 Fortrea

- 6.3.7 IQVIA

- 6.3.8 ICON plc

- 6.3.9 Inductive Quotient

- 6.3.10 InnovoCommerce

- 6.3.11 Labcorp Drug Development

- 6.3.12 LyfeSci

- 6.3.13 Medpace

- 6.3.14 Novotech

- 6.3.15 Parexel

- 6.3.16 PhaseV

- 6.3.17 PSI CRO

- 6.3.18 Thermo Fisher Scientific Inc. (PPD)

- 6.3.19 Verisian

- 6.3.20 Voiant Clinical

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment