PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063924

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063924

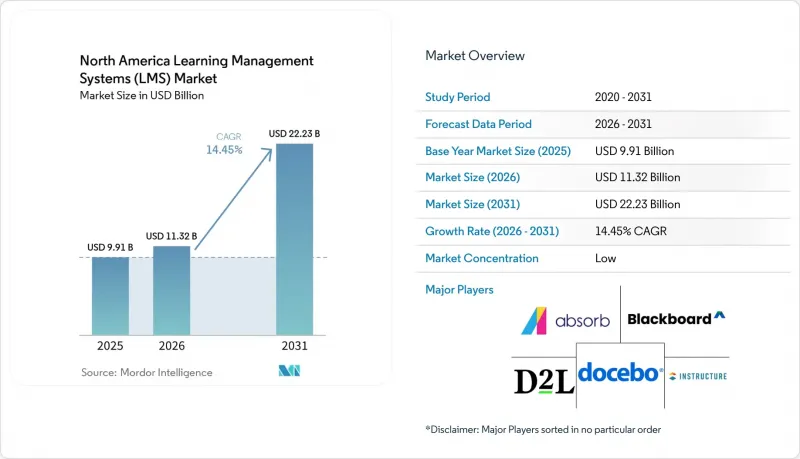

North America Learning Management Systems (LMS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america learning management systems (LMS) market size is projected to expand from USD 9.91 billion in 2025 and USD 11.32 billion in 2026 to USD 22.23 billion by 2031, registering a CAGR of 14.45% between 2026 and 2031.

This report is Segmented by Component (Solution, and Services), Deployment (Cloud, On-Premises, and Hybrid), Learning Type (Academic Learning, and More), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Industry Vertical (Information Technology and Telecommunications, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America Learning Management Systems (LMS) Market Trends and Insights

Enterprise Upskilling and Compliance Digitization

The North America learning management systems market is receiving steady support from employers that now treat reskilling as an operating requirement rather than an occasional talent initiative. Instructure announced the broad availability of Canvas Career in January 2026 to support skills-first workforce learning for adult learners and workforce-aligned education programs, underscoring how closely platform demand is now tied to employability and internal mobility needs. Regulated buyers are also keeping spending consistent because training completion, certification status, and learner records must be documented and retrievable across large user populations. TotaraGov states that its platform serves more than 50 U.S. government agencies, including USDA's AgLearn environment, which has 140,000 users across 30 agencies, demonstrating how deeply auditable digital learning is embedded in public-sector operations. Docebo also disclosed customer wins with a major U.S. financial services regulator, reinforcing the importance of learning systems in highly supervised environments. This blend of skills, pressure, and recurring compliance needs gives the North America learning management systems market a durable demand floor even when general software budgets face scrutiny.

AI-Powered Personalization and Learning Analytics Adoption

The North America learning management systems market is moving from basic content delivery toward platforms that guide learning decisions in real time. Docebo launched AgentHub in April 2026 to combine learning delivery, enterprise knowledge, skills intelligence, and agentic AI in a single environment, demonstrating how vendors are repositioning the LMS as a more active system layer. Litmos is promoting AI and machine learning video assessments that evaluate learner tone, clarity, and keyword use without manual grading, which expands scalable skills validation for distributed teams. Instructure also introduced AI Nutrition Facts within its April 2026 Canvas tier update, giving buyers clearer visibility into how AI-enabled features work and what they process. Those releases matter because many education, public-sector, and regulated enterprise buyers want automation that improves learner outcomes without weakening governance or explainability. As a result, vendors that can show transparent AI workflows are gaining a stronger position in the North America learning management systems market.

Data Privacy and Cybersecurity Concerns

The North America learning management systems market still faces slower procurement where student or employee data governance is highly sensitive. CoSN's 2025 National Student Data Privacy Report found that 88% of district ed-tech leaders ranked student data privacy as a top-two priority, underscoring how central this issue has become in education purchasing decisions. The same report showed that only 43% conducted regular audits of their privacy practices, indicating that many institutions are still working through governance gaps as they expand digital learning use. CoSN also found that 55% of respondents were concerned about managing the influx of unvetted classroom technologies, which raises the bar for LMS vendors adding AI and third-party capabilities. Buyers are therefore asking harder questions on data access, retention, oversight, and institutional control before approving deployments. The result is not a collapse in demand, but a longer path to conversion across privacy-sensitive segments of the North America learning management systems market.

Other drivers and restraints analyzed in the detailed report include:

- Hybrid and Asynchronous Learning Normalization

- Cloud-Native LMS Modernization for Distributed Training

- Legacy HRIS, SIS, and Content-System Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for 71.44% of the North America learning management systems market share by component in 2025, indicating that software subscriptions and platform licenses remained the core spending areas. Services are projected to grow at a 16.27% CAGR, marking the fastest expansion in the North America learning management systems market size by component from 2026 to 2031. That gap between current scale and future growth shows that buyers increasingly value the work around the platform rather than the platform itself. Migration from legacy systems, integration with enterprise applications, AI configuration, learner support, and ongoing optimization are now part of the buying decision in many larger accounts. Instructure's exclusive access to K16 Solutions directly monetizes migration demand and shows that vendors now treat services as a strategic revenue line rather than a peripheral attachment.

The North America learning management systems market is therefore placing more value on services that extend well beyond initial setup. Mid-market buyers also need support, as many lack in-house teams to manage learning integrations, AI policy tuning, and content restructuring. This is widening the addressable opportunity into managed learning support, operational administration, and continuous improvement work. Absorb's 2025 roadmap emphasized AI-driven personalized learning, strategic learning playbooks, and peer learning communities, which indicates that even customer-facing innovations can create new implementation and enablement needs after go-live. As the North America learning management systems industry becomes more dependent on analytics, automation, and migration work, services are likely to remain the faster-moving component, even as solutions maintain the larger revenue base.

Cloud deployment captured 65.32% of the North America learning management systems market by deployment mode in 2025, confirming that the long migration away from older infrastructure is well advanced. Hybrid deployment is projected to expand at a 15.34% CAGR from 2026 to 2031, which makes it the fastest-growing mode in this segmentation. That pattern shows that many buyers are not choosing between cloud and on-premises in absolute terms. They are instead building staged architectures that preserve sensitive repositories or local controls while moving user-facing learning functions into more flexible environments. TotaraGov's public-sector presence across more than 50 U.S. agencies demonstrates that modern learning deployments can meet strict governance requirements without forcing every buyer onto the same architectural path.

In higher education and government, migration timing often matters as much as the final target architecture, because institutions need continuity of access, preservation of legacy content, and dependable audit trails during transition periods. Instructure's K16 partnership reflects this reality by focusing directly on course migration, assessment transfer, and preservation of structure for institutions leaving older platforms. Cloud delivery is also becoming more strategic, as major vendors are placing new AI capabilities within existing product tiers rather than reserving them for custom environments. Instructure embedded IgniteAI Agent capabilities in Canvas Next during April 2026, and Docebo's 2026 release cycle highlighted continued delivery of AI-enabled features through its cloud platform. For the North America learning management systems market, hybrid deployment is serving as the bridge between current operational constraints and a longer-term move toward cloud-led learning environments.

List of Companies Covered in this Report:

- Blackboard LLC

- Instructure, Inc.

- D2L Corporation

- Docebo Inc.

- Absorb Software Inc.

- Litmos US, L.P.

- Moodle Pty Ltd.

- Totara Learning Solutions

- LearnUpon

- 360LEARNING SA

- Epignosis LLC

- SkyPrep Inc.

- Axonify Inc.

- Meridian Knowledge Solutions

- Thinkific Labs Inc.

- Thought Industries

- Learning Pool

- Schoox

- Skilljar

- LearnWorlds (CY) Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Enterprise Upskilling and Compliance Digitization

- 4.2.2 AI-Powered Personalization and Learning Analytics Adoption

- 4.2.3 Hybrid and Asynchronous Learning Normalization

- 4.2.4 Cloud-Native LMS Modernization for Distributed Training

- 4.2.5 Verifiable Digital Credentials and Skills-Based Hiring Integration

- 4.2.6 Learner Record Interoperability and Short-Form Credential Accountability

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cybersecurity Concerns

- 4.3.2 Legacy HRIS, SIS, and Content-System Integration Complexity

- 4.3.3 Fragmented State AI and Student-Data Regulation

- 4.3.4 Rising Cyber-Insurance and Security-Control Costs for School Districts

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-premises

- 5.2.3 Hybrid

- 5.3 By Learning Type

- 5.3.1 Academic Learning

- 5.3.2 Corporate Training

- 5.3.3 Government / Public Training

- 5.3.4 Skill Development / Certification

- 5.4 By End User Vertical

- 5.4.1 Information Technology (IT) and Telecommunications

- 5.4.2 Banking, Financial Services, and Insurance (BFSI)

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Manufacturing and Industrial Operations

- 5.4.5 Retail and E-commerce

- 5.4.6 Education

- 5.4.7 Government and Public Sector

- 5.4.8 Energy and Utilities

- 5.4.9 Media and Entertainment

- 5.5 By End User Enterprise Size

- 5.5.1 Large Enterprises

- 5.5.2 Small and Medium-sized Enterprises

- 5.6 By Geography

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Blackboard LLC

- 6.4.2 Instructure, Inc.

- 6.4.3 D2L Corporation

- 6.4.4 Docebo Inc.

- 6.4.5 Absorb Software Inc.

- 6.4.6 Litmos US, L.P.

- 6.4.7 Moodle Pty Ltd.

- 6.4.8 Totara Learning Solutions

- 6.4.9 LearnUpon

- 6.4.10 360LEARNING SA

- 6.4.11 Epignosis LLC

- 6.4.12 SkyPrep Inc.

- 6.4.13 Axonify Inc.

- 6.4.14 Meridian Knowledge Solutions

- 6.4.15 Thinkific Labs Inc.

- 6.4.16 Thought Industries

- 6.4.17 Learning Pool

- 6.4.18 Schoox

- 6.4.19 Skilljar

- 6.4.20 LearnWorlds (CY) Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment