PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063960

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063960

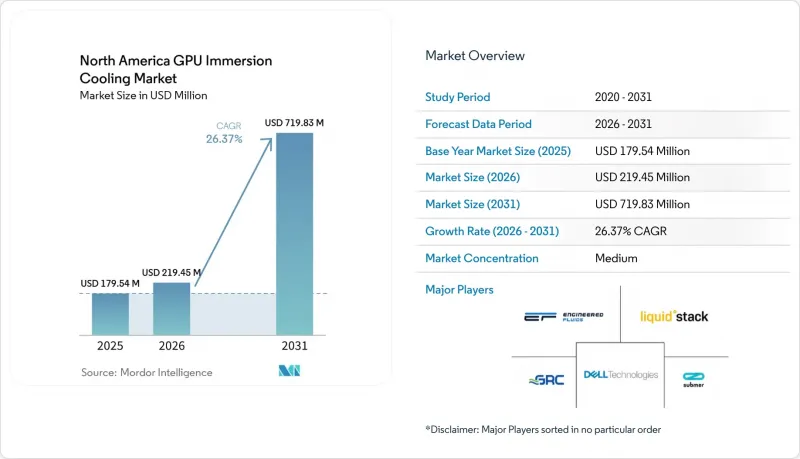

North America GPU Immersion Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the gPU immersion cooling market size is expected to increase from USD 179.54 million in 2025 and USD 219.45 million in 2026 to USD 719.83 million by 2031, growing at a CAGR of 26.37% over 2026-2031.

This report is Segmented by Immersion Type (Single-Phase Immersion Cooling, and Two-Phase Immersion Cooling), Solution Type (Immersion Cooling Tank/Systems, Immersion-Optimized GPU Server Systems, and More), Deployment (Hyperscale/Cloud, Enterprise, and More), GPU Power Density (Below 300W, 300W-700W, and Above 700W), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America GPU Immersion Cooling Market Trends and Insights

Growing Demand for High-Density GPU Compute for Generative AI Workloads

Training and inference clusters are already fielding NVIDIA H100 GPUs rated at 700 watts, and the leap to 1,000-watt Blackwell B200 silicon pushes rack power toward 120 kilowatts. Immersion cooling allows operators to crest these density thresholds without chiller upgrades, keeping PUE near 1.1. xAI's Memphis supercomputer reached 100,000 liquid-cooled H100S and logged a PUE of 1.09, setting a performance baseline other hyperscalers now chase. With trillion-parameter language models standardizing, even enterprise labs accept that air cooling throttles utilization, cementing immersion as the pragmatic path to GPU (Graphics Processing Unit) saturation.

Expanding Deployment of Liquid-Cooled Hyperscale Data Centers by U.S. Cloud Providers

Amazon, Microsoft, Google, and Oracle have each publicized liquid-cooling roadmaps that convert every new availability zone after 2025 into either direct-to-chip or immersion builds. CoreWeave's 300-megawatt Quebec campus illustrates the economic upside of combining immersion tanks with district heating loops, offsetting cooling costs through municipal energy sales. These high-profile commitments reassure CFOs that immersion is not an experiment but an industry baseline, strengthening the upgrade narrative inside Fortune 500 IT departments.

Limited Availability of Synthetic Dielectric Fluids with UL and EPA Approvals

In 2025, 3M announced its decision to exit the Novec product line, a move that significantly reduced the number of approved chemistries available in the market from seven to four. This reduction in options triggered a 40% increase in secondary-market pricing, creating additional cost pressures for operators. As a result, operators are now required to undergo a re-qualification process with alternative fluids supplied by Solvay, Chemours, or Shell. This process, which typically spans six to nine months, presents operational challenges and carries the potential risk of voiding GPU warranties unless vendors explicitly provide immersion riders to address compatibility concerns. Adding to these complexities, the Environmental Protection Agency (EPA) has implemented stricter thresholds for volatile organic compounds (VOCs), further limiting the range of candidate fluids available. These regulatory changes coincide with a surge in demand, intensifying supply constraints and creating a challenging environment for market participants.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Regulations by U.S. Department of Energy Targeting PUE Reductions

- Vendor-Led Open Hardware Standards Accelerating Adoption

- Capital-Intensive Retrofit Requirements for Legacy Enterprise Data Halls

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-phase designs captured 79.87% of 2025 North America GPU immersion cooling market revenue by leveraging simpler plumbing and broader fluid options. Enterprises favor atmospheric-pressure operation, while hyperscalers pilot two-phase tanks to chase sub-1.05 PUE targets and sub-ambient silicon temperatures. The NA Graphics Processing Unit immersion cooling market size for two-phase architectures is projected to climb steadily as warranty coverage matures and condenser automation trims maintenance overhead. Yet single-phase vendors retain an edge on ease of use, exemplified by GRC's plug-and-play ICEraQ Series 3, which ships with recirculation and monitoring baked in.

Hyperscale buyers are willing to train technicians on boiling-fluid dynamics, expecting latency cuts that shave cost-per-inference. Submer's SmartPodX Gen 2 already bundles vapor recovery and closed-loop condensers, positioning it for AI inference farms that prize every extra degree of cooling headroom. Meanwhile, Intel's oil-based warranty rider signals OEM readiness to normalize single-phase deployments, but GPU manufacturers have yet to extend similar guarantees for two-phase chemistries, limiting some operators to pilot-scale deployments until broader warranty frameworks emerge.

In 2025, tanks and ancillary infrastructure commanded 55.23% of revenue of the North America GPU immersion cooling market, but immersion-optimized servers are outrunning at a 26.56% CAGR through 2031. ODMs now pre-install thermal interface pads, fluid manifolds, and out-of-band sensors, avoiding costly field retrofits. For example, Supermicro's DLC-3 platform supports 150-kilowatt racks and ships immersion-ready for H200, MI325X, and Gaudi 3 accelerators. As a result, the GPU immersion cooling market size tied to integrated server platforms will narrow the gap with tank revenue by the decade's close.

Tanks continue to benefit from modular 50-kilowatt blocks that colocation landlords deploy incrementally, but fluid revenue is flattening as operators install on-site reclamation skid packages that extend service life by two years. Dielectric suppliers thus pivot to bundled analytics, embedding inline spectroscopy to upsell predictive-maintenance subscriptions, a move that keeps them tethered to the GPU immersion cooling market even as raw-fluid volumes plateau.

List of Companies Covered in this Report:

- GRC (Green Revolution Cooling)

- Submer Technologies SL

- LiquidStack Holding Pte. Ltd.

- Engineered Fluids Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Super Micro Computer Inc.

- Nvidia Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- 3M Company

- Shell plc

- Fluoramics Inc.

- Asperitas BV

- Wiwynn Corporation

- Midas Immersion Cooling

- CoolIT Systems Inc.

- Asetek A/S

- Schneider Electric SE

- Vertiv Holdings Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for High-Density GPU Compute for Generative AI Workloads

- 4.2.2 Expanding Deployment of Liquid-Cooled Hyperscale Data Centers by U.S. Cloud Providers

- 4.2.3 Energy-Efficiency Regulations by the U.S. Department of Energy Targeting PUE Reductions

- 4.2.4 Vendor-Led Open Hardware Standards (e.g., OCP Advanced Cooling Solutions) Accelerating Adoption

- 4.2.5 Rising Electricity Tariffs in Northern Virginia and Silicon Valley

- 4.2.6 Heat-Reuse Incentives Supporting Data-Center Waste-Heat Recovery

- 4.3 Market Restraints

- 4.3.1 Limited Availability of Synthetic Dielectric Fluids with UL and EPA Approvals

- 4.3.2 Capital-Intensive Retrofit Requirements for Legacy Enterprise Data Halls

- 4.3.3 Uncertain Long-Term GPU Warranty Policies for Two-Phase Immersion Fluids

- 4.3.4 Supply-Chain Concentration of Immersion Tank Manufacturing in East Asia

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Immersion Type

- 5.1.1 Single-Phase Immersion Cooling

- 5.1.2 Two-Phase Immersion Cooling

- 5.2 By Solution Type

- 5.2.1 Immersion Cooling Tanks / Systems

- 5.2.2 Dielectric Fluids

- 5.2.3 Immersion-Optimized GPU Server Systems

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W-700W

- 5.4.3 Above 700W

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 GRC (Green Revolution Cooling)

- 6.4.2 Submer Technologies SL

- 6.4.3 LiquidStack Holding Pte. Ltd.

- 6.4.4 Engineered Fluids Inc.

- 6.4.5 Dell Technologies Inc.

- 6.4.6 Hewlett Packard Enterprise Company

- 6.4.7 Super Micro Computer Inc.

- 6.4.8 Nvidia Corporation

- 6.4.9 Advanced Micro Devices Inc.

- 6.4.10 Intel Corporation

- 6.4.11 3M Company

- 6.4.12 Shell plc

- 6.4.13 Fluoramics Inc.

- 6.4.14 Asperitas BV

- 6.4.15 Wiwynn Corporation

- 6.4.16 Midas Immersion Cooling

- 6.4.17 CoolIT Systems Inc.

- 6.4.18 Asetek A/S

- 6.4.19 Schneider Electric SE

- 6.4.20 Vertiv Holdings Co.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment