PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063969

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063969

360-Degree Feedback Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

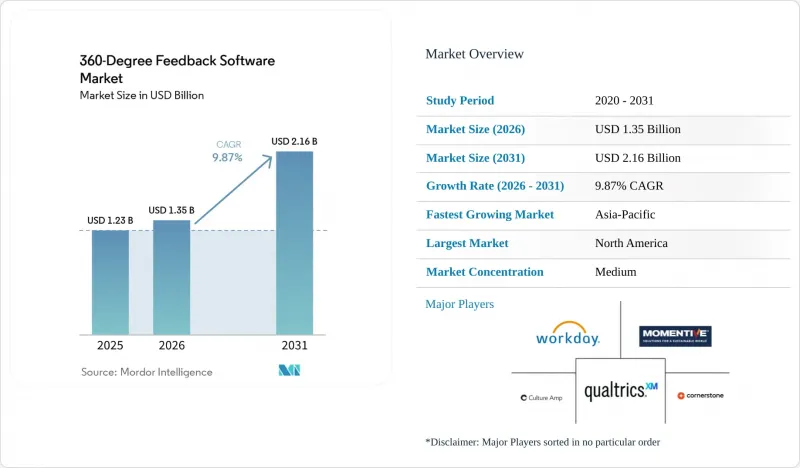

According to Mordor Intelligence, the 360-degree feedback software market size is expected to grow from USD 1.23 billion in 2025 to USD 1.35 billion in 2026 and is forecast to reach USD 2.16 billion by 2031 at 9.87% CAGR over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment (Cloud, On-Premises, and Hybrid), Organization Size (Small and Medium-Sized Enterprises, and Large Enterprises), Industry Vertical (IT and Telecom, BFSI, Healthcare and Lifesciences, and More), Pricing Model (Subscription-Based, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global 360-Degree Feedback Software Market Trends and Insights

AI-Driven Personalized Feedback Workflows

Generative AI now tailors question sets to individual competency gaps and rapidly converts raw multi-rater data into coaching prompts, slashing insight lead time from weeks to hours. Microsoft Viva Glint, SAP SuccessFactors, and Oracle HCM Cloud have all released agentic AI features that surface sentiment patterns and flag rating discrepancies, prompting 48% of European HR teams to pilot specialized AI performance tools in 2025. Vendors unable to embed real-time personalization or bias screening risk price erosion as buyers increasingly view those capabilities as table stakes.

Integration of 360-Degree Feedback into Continuous Performance Management Suites

Quarterly reviews are replacing annual appraisals, pushing organizations to converge feedback, goal tracking, and peer recognition into unified workflows. Workday's 2025 acquisition of Sana for USD 1.1 billion was framed as a move to weave AI-driven talent intelligence across its HCM suite, underscoring how tightly integrated analytics now shape succession planning and skill development. Stand-alone vendors, therefore, face a build-or-partner decision as cross-suite integration has become a primary buying criterion in the 360-degree feedback software market.

Concerns Over Data Privacy and Psychometric Bias

Strict statutes like GDPR and California ADMT now require transparency on algorithmic decision-making, elevating vendor compliance costs and amplifying litigation risk. A 2025 Journal of Applied Psychology article revealed that 30% of responses in large firms were skewed by rater bias, prompting buyers to demand encryption, audit logs, and statistical bias checks. Vendors lagging on these safeguards face procurement delays and potential reputational damage.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Hybrid and Remote Work Operating Models

- Rising Demand for Data-Driven Leadership Development Programs

- Change-Management Challenges in Traditional Hierarchical Cultures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software captured 78.92% of market revenue of the 360-degree feedback software market in 2025, reflecting the dominance of license and subscription fees, yet services are projected to expand at 10.96% CAGR through 2031, outpacing the overall market rate. SurveyConnect observed that 40% of HR teams in firms above 5,000 employees failed to create actionable dashboards within a month, catalyzing demand for advisory projects. As a result, vendors now bundle quarterly calibration workshops into premium tiers, blending software and services in one subscription.

The 360-degree feedback software market benefits as service partners monetize rater-training, psychometric validation, and culture-change roadmaps, especially in regulated verticals where GDPR or healthcare accreditation demands third-party attestation. Paychex's January 2025 announcement of its USD 4.1 billion acquisition of Paycor highlighted expected run-rate cost synergies exceeding USD 80 million, with substantial revenue synergy opportunities tied to cross-selling implementation and advisory services across a combined customer base of approximately 745,000 clients.

Cloud deployment commanded 69.14% of the 360-degree feedback software market share in 2025, driven by scalability, automatic updates, and lower upfront capital expenditure, yet hybrid configurations are growing at 11.42% CAGR through 2031, the fastest rate among deployment models. UAE regulations that require federal employee records to stay on national soil have spurred interest in private cloud nodes hosted in domestic data centers. SAP's 2026 SuccessFactors release leverages cloud infrastructure for real-time AI while supporting customer-controlled storage for compensation files, illustrating how large vendors balance sovereignty and agility.

Hybrid architectures appeal to financial services, healthcare, and government entities that must balance data sovereignty mandates with the agility and AI capabilities of cloud-native platforms. On-premises deployments persist in legacy manufacturing firms and defense contractors where air-gapped networks and stringent cybersecurity protocols prohibit cloud connectivity, though this segment is contracting as vendors phase out on-premises support in favor of private cloud instances hosted in customer-controlled data centers.

Geography Analysis

North America generated 39.28% of 2025 revenue, sustained by Fortune 500 cross-suite expansions and a compliance environment that rewards transparent talent processes. Federal contractors moving to hybrid deployments have lengthened deal cycles but lifted average contract value as buyers layer advisory and security modules. The region also benefits from early adoption of AI-enabled HR tools, which enhances analytics-driven decision-making and accelerates platform upgrades. Additionally, strong vendor ecosystems and high HR tech spending capacity continue to reinforce North America's leadership position.

Europe posts slower topline growth yet enjoys sticky renewal rates because GDPR heightens vendor switching costs. Lattice data show 51% of European firms run quarterly reviews, cementing demand for continuous feedback loops. High legal scrutiny means buyers favor platforms that provide clear audit trails and automated deletion workflows, adding complexity that protects incumbent penetration. This regulatory environment encourages long-term vendor relationships and increases demand for compliant, enterprise-grade solutions. Moreover, multilingual workforce requirements further drive the need for customizable and localized platforms.

Asia-Pacific is the clear volume driver with a 12.36% CAGR. Indian vendors such as Darwinbox localize labor codes and offer vernacular interfaces while Chinese state-owned enterprises modernize talent oversight under national digitalization programs. Cultural hesitancy toward upward feedback persists in Japan and South Korea, so vendors invest in anonymity guarantees and group discourse formats that sustain user confidence without violating face-saving norms. Rapid SME digitization and cost-sensitive SaaS adoption are also expanding the addressable market across the region. In addition, increasing government-led digital transformation initiatives are accelerating enterprise adoption of structured feedback systems.

- Culture Amp Pty Ltd

- Qualtrics LLC

- Momentive Global Inc.

- Cornerstone OnDemand Inc.

- Workday Inc.

- Inspire Software Inc.

- Leapsome GmbH

- EchoSpan Inc.

- Spidergap Ltd

- Trakstar Inc.

- Reflektive Inc.

- SurveySparrow Inc.

- EngageRocket Pte. Ltd.

- Betterworks Systems Inc.

- PeopleGoal Ltd.

- 15Five Inc.

- AssessTEAM LLC

- ClearCompany Inc.

- Synergita Software Pvt. Ltd.

- Reviewsnap, LLC

- OrangeHRM Inc.

- PeopleFluent Holdings Corp.

- Lattice HR Inc.

- Saba Software Inc.

- BambooHR LLC

- Zoho Corporation Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Driven Personalised Feedback Workflows

- 4.2.2 Integration of 360-Degree Feedback into Continuous Performance Management Suites

- 4.2.3 Expansion of Hybrid and Remote-Work Operating Models

- 4.2.4 Rising Demand for Data-Driven Leadership Development Programs

- 4.2.5 Growing Adoption Across Emerging-Market SMBs Via Freemium GTM Strategies

- 4.2.6 Increasing Regulatory Emphasis on Objective Employee Evaluations

- 4.3 Market Restraints

- 4.3.1 Concerns Over Data Privacy and Psychometric Bias

- 4.3.2 Change-Management Challenges in Traditional Hierarchical Cultures

- 4.3.3 Limited HR Tech Budgets in Micro-enterprises

- 4.3.4 Interoperability Gaps with Legacy HCM/ERP Stacks

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Small and Medium-sized Enterprises

- 5.3.2 Large Enterprises

- 5.4 By Industry Vertical

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Lifesciences

- 5.4.4 Retail and E-commerce

- 5.4.5 Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Other Industry Verticals

- 5.5 By Pricing Model

- 5.5.1 Subscription-Based

- 5.5.2 Perpetual / One-Time License

- 5.5.3 Usage-Based / Pay-Per-Use

- 5.5.4 Freemium

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Egypt

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Culture Amp Pty Ltd

- 6.4.2 Qualtrics LLC

- 6.4.3 Momentive Global Inc.

- 6.4.4 Cornerstone OnDemand Inc.

- 6.4.5 Workday Inc.

- 6.4.6 Inspire Software Inc.

- 6.4.7 Leapsome GmbH

- 6.4.8 EchoSpan Inc.

- 6.4.9 Spidergap Ltd

- 6.4.10 Trakstar Inc.

- 6.4.11 Reflektive Inc.

- 6.4.12 SurveySparrow Inc.

- 6.4.13 EngageRocket Pte. Ltd.

- 6.4.14 Betterworks Systems Inc.

- 6.4.15 PeopleGoal Ltd.

- 6.4.16 15Five Inc.

- 6.4.17 AssessTEAM LLC

- 6.4.18 ClearCompany Inc.

- 6.4.19 Synergita Software Pvt. Ltd.

- 6.4.20 Reviewsnap, LLC

- 6.4.21 OrangeHRM Inc.

- 6.4.22 PeopleFluent Holdings Corp.

- 6.4.23 Lattice HR Inc.

- 6.4.24 Saba Software Inc.

- 6.4.25 BambooHR LLC

- 6.4.26 Zoho Corporation Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment