PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063997

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063997

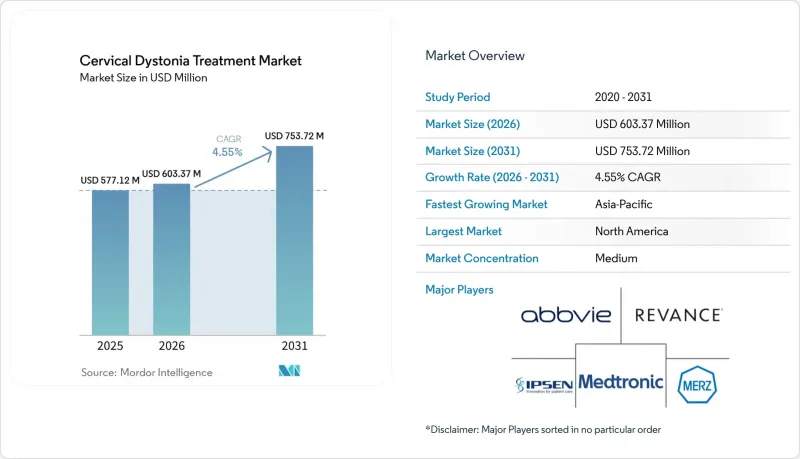

Cervical Dystonia Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the cervical dystonia treatment market size is expected to grow from USD 577.12 million in 2025 to USD 603.37 million in 2026 and is forecast to reach USD 753.72 million by 2031 at 4.55% CAGR over 2026-2031.

This report is Segmented by Treatment Type (Botulinum Toxin Injections [Type A Neurotoxins {OnabotulinumtoxinA, and More}, and More], Oral Medications, and More), Care Setting (Hospitals, Neurology Clinics, and More), Distribution Channel (Hospital, Retail, Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Cervical Dystonia Treatment Market Trends and Insights

Rising Diagnosis Rates in Mid-Life Neurology Cohorts

The cervical dystonia treatment market still leaves revenue on the table when patients spend years moving through general neurology visits before reaching a movement disorder specialist. Earlier diagnosis in mid-life cohorts matters because this is the stage when persistent abnormal posture, tremor, and pain are more likely to be recognized as a treatable dystonia pattern rather than a musculoskeletal complaint. Patients who enter treatment earlier often do so with less accumulated cervical degeneration and a lower baseline pain burden, which supports steadier follow-up and better continuity across injection cycles. That change has a direct commercial effect because recurring therapies depend on retention, not only on first diagnosis. The cervical dystonia treatment market therefore benefits when referral pathways shorten the lag between first symptoms and specialist confirmation. This effect is likely to emerge first in health systems that already have dense neurology networks and established referral routes.

Longer-Acting Toxin Innovation and Label Expansion

Longer-duration toxin development is the clearest formulation shift now shaping the cervical dystonia treatment market. DAXXIFY received U.S. approval for cervical dystonia in August 2023, and its commercial roll-out through 2024 introduced the first major therapeutic formulation advance in this class in more than 30 years. In the ASPEN-1 Phase 3 trial, the 125-unit dose showed a median duration of effect of 24 weeks, and dysphagia was reported at 1.6%, compared with the much shorter 10 to 12 week effect window often associated with older clinical practice patterns. Crown Laboratories completed its acquisition of Revance Therapeutics in February 2025 for USD 924 million, which showed that commercial infrastructure is now being built around extended-duration toxin use. Revance also reported that therapeutic revenue for DAXXIFY rose 318% in 2024 to USD 31.4 million, which was modest in absolute terms but meaningful for an asset that had only just entered commercial use. Ipsen added to the long-duration pipeline by initiating a Phase II study of corabotase in cervical dystonia in September 2025, which broadened the cervical dystonia treatment market beyond a single new entrant.

High Recurring Therapy Cost and Reimbursement Friction

Recurring cost remains one of the most important constraints on the cervical dystonia treatment market because branded toxin use requires repeat administration over long periods. In the United States, prior authorization under commercial and Medicare Advantage plans often requires diagnosis confirmation, muscle-level injection records, and proof of prior treatment response before another cycle is approved. When administrative delays push patients past planned retreatment timing, symptom control can fall sharply and disability can return, which raises the risk of discontinuation. CMS policy generally limits injections to every 12 weeks and was built around older toxin patterns, which creates a poor fit for products such as DAXXIFY that showed a 24-week median duration of effect in trial data. Physicians are then left to justify retreatment timing or manage expectations around a policy-driven care gap that does not always match clinical reality. Even when manufacturers provide support services, the cervical dystonia treatment market remains exposed to payer timing rules that can limit both utilization and satisfaction.

Other drivers and restraints analyzed in the detailed report include:

- Chronic First-Line Positioning of Botulinum Neurotoxins

- Ultrasound and EMG-Guided Injection Precision Gains

- Misdiagnosis and Limited Specialist Injector Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Botulinum toxin injections accounted for 68.2% of revenue in 2025, which kept them firmly in the lead across treatment categories in the cervical dystonia treatment market. Their position reflects long-standing specialist familiarity, durable reimbursement pathways, and the fact that they remain the most established first-line option for symptom control. OnabotulinumtoxinA continues to hold brand leadership within this group because injector habit and formulary preference still matter heavily in routine practice. IncobotulinumtoxinA keeps a distinct role through its protein-free formulation, and that profile gained added commercial relevance when Merz Therapeutics enrolled the first patients in its Phase III MINT-E and MINT-C migraine prevention trials in August 2025. RimabotulinumtoxinB also keeps a structurally important place in the cervical dystonia treatment industry because it serves Type A secondary non-responders, and MYOBLOC net product sales reached USD 101.1 million in 2024, up 10% year over year.

Oral medications are projected to expand at 7.0% through 2031, making them the fastest-growing treatment class in the cervical dystonia treatment market. That growth reflects adjunct use rather than replacement, since valbenazine improved TWSTRS scores and reduced end-of-cycle wearing-off when added to botulinum neurotoxin treatment in a 2025 pilot study. Generic penetration in anticholinergics and benzodiazepines also supports uptake where access to toxin treatment is limited or delayed. Device-based and surgical options remain smaller because they are reserved for refractory patients, yet the December 2025 FDA labeling change for Medtronic DBS should broaden payer willingness to cover this part of the cervical dystonia treatment industry.

Geography Analysis

North America held 41.2% of revenue in 2025, which gave the region the largest share in the cervical dystonia treatment market. The United States remained the largest country base, and AbbVie reported USD 3.151 billion in U.S. therapeutic neurotoxin revenue in 2025 across its full therapeutic portfolio. Regional growth still faces a reimbursement ceiling because CMS timing rules do not fully align with the longer duration shown for DAXXIFY in clinical data. At the same time, North America benefits from dense specialist access, established prior authorization pathways, and early commercial adoption of new toxin formats. These factors keep the cervical dystonia treatment market strong in the region even when payer friction slows full use of extended-duration products.

Europe remained the second-largest regional block in the cervical dystonia treatment market, supported mainly by Germany, France, and the United Kingdom. Ipsen reported EUR 158.4 million in European Dysport Therapeutics revenue in 2025, equal to USD 168.1 million, with 6.8% constant-exchange-rate growth. The region benefits from broad specialist expertise and favorable reimbursement in core countries, though centralized referral structures can still limit throughput at the provider level. Merz also enrolled the first patients in 2 global Phase III migraine trials for Xeomin in August 2025, which reinforced its broader neurology positioning from a European base.

Asia-Pacific is projected to expand at 6.3% through 2031, which makes it the fastest-growing regional part of the cervical dystonia treatment market. Growth is being supported by broader specialist infrastructure, competitive activity from regional neurotoxin manufacturers, and a wider set of commercialization pathways than the region had a few years ago. Hugel has cervical dystonia in Phase I development for its botulinum toxin program, which shows that the regional pipeline is moving beyond cosmetic use into therapeutic positioning. South America and the Middle East and Africa remain early-stage, though Daewoong's February 2025 launch of Nabota in Saudi Arabia shows that geographic expansion is continuing outside the largest established markets.

- Abbvie

- AEON Biopharma, Inc.

- Daewoong Pharmaceutical Co., Ltd.

- Fosun Pharma

- Ipsen

- Medtronic

- Medytox, Inc.

- Merz Pharma

- Mitra Bio, Inc.

- Revance Therapeutics, Inc.

- Sloan Pharma S.a.r.l.

- Solstice Neurosciences, LLC

- Supernus Pharmaceuticals

- Teijin Pharma Limited

- Vima Therapeutics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Diagnosis Rates in Mid-Life Neurology Cohorts

- 4.2.2 Longer-Acting Toxin Innovation and Label Expansion

- 4.2.3 Chronic First-Line Positioning of Botulinum Neurotoxins

- 4.2.4 Ultrasound and EMG-Guided Injection Precision Gains

- 4.2.5 Patient Affordability and Reimbursement-Support Programs

- 4.3 Market Restraints

- 4.3.1 High Recurring Therapy Cost and Reimbursement Friction

- 4.3.2 Misdiagnosis and Limited Specialist Injector Capacity

- 4.3.3 Secondary Non-Response and End-Of-Cycle Symptom Rebound

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Treatment Type

- 5.1.1 Botulinum Toxin Injections

- 5.1.1.1 Type A Neurotoxins

- 5.1.1.1.1 OnabotulinumtoxinA

- 5.1.1.1.2 AbobotulinumtoxinA

- 5.1.1.1.3 IncobotulinumtoxinA

- 5.1.1.1.4 Other Type A Neurotoxins

- 5.1.1.2 Type B Neurotoxins

- 5.1.1.2.1 RimabotulinumtoxinB

- 5.1.1.1 Type A Neurotoxins

- 5.1.2 Oral Medications

- 5.1.2.1 Anticholinergics

- 5.1.2.2 Benzodiazepines and GABAergic agents

- 5.1.2.3 Muscle relaxants

- 5.1.2.4 Dopaminergic and VMAT-modulating agents

- 5.1.3 Device-based and Surgical Interventions

- 5.1.3.1 Deep Brain Stimulation

- 5.1.3.2 Selective Peripheral Denervation

- 5.1.4 Supportive and Adjunctive Therapies

- 5.1.1 Botulinum Toxin Injections

- 5.2 By Care Setting

- 5.2.1 Hospitals

- 5.2.2 Specialty Neurology Clinics

- 5.2.3 Ambulatory Surgical Centers

- 5.2.4 Home Care and Rehabilitation Centers

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 Online Pharmacies

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 AbbVie Inc.

- 6.3.2 AEON Biopharma, Inc.

- 6.3.3 Daewoong Pharmaceutical Co., Ltd.

- 6.3.4 Fosun Pharma

- 6.3.5 Ipsen S.A.

- 6.3.6 Medtronic plc

- 6.3.7 Medytox, Inc.

- 6.3.8 Merz Pharma GmbH & Co. KGaA

- 6.3.9 Mitra Bio, Inc.

- 6.3.10 Revance Therapeutics, Inc.

- 6.3.11 Sloan Pharma S.a.r.l.

- 6.3.12 Solstice Neurosciences, LLC

- 6.3.13 Supernus Pharmaceuticals, Inc.

- 6.3.14 Teijin Pharma Limited

- 6.3.15 Vima Therapeutics

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment